Key Takeaways

- The Puerto Rico Department of State administers all business entity formations on the island under a dual legal framework that applies both federal law and local statutes simultaneously.

- Among the available structures, the LLC (Compañía de Responsabilidad Limitada) is the most widely registered entity type in Puerto Rico, favored for its operating flexibility and pass-through tax treatment.

- Corporations formed under the Puerto Rico General Corporations Act are best suited for businesses that anticipate outside investment or public offerings.

- Act 60 of 2019 and ongoing federal oversight through PROMESA distinguish Puerto Rico's regulatory environment from that of standard U.S. state jurisdictions, making the entity selection process here more complex than a typical domestic incorporation.

Introduction to Entity Types in Puerto Rico

Puerto Rico is a Caribbean island territory located approximately 1,000 miles southeast of Miami, situated between the Dominican Republic to the west and the U.S. Virgin Islands to the east. As an unincorporated territory of the United States, it operates under a dual legal framework — subject to federal law while maintaining its own local statutes and regulatory institutions.

Company registration falls under the jurisdiction of the Puerto Rico Department of State, which administers the formation and maintenance of business entities on the island. Federal tax obligations apply alongside local ones, though Puerto Rico's tax regime includes significant incentive programs that can substantially reduce the effective rate for qualifying businesses.

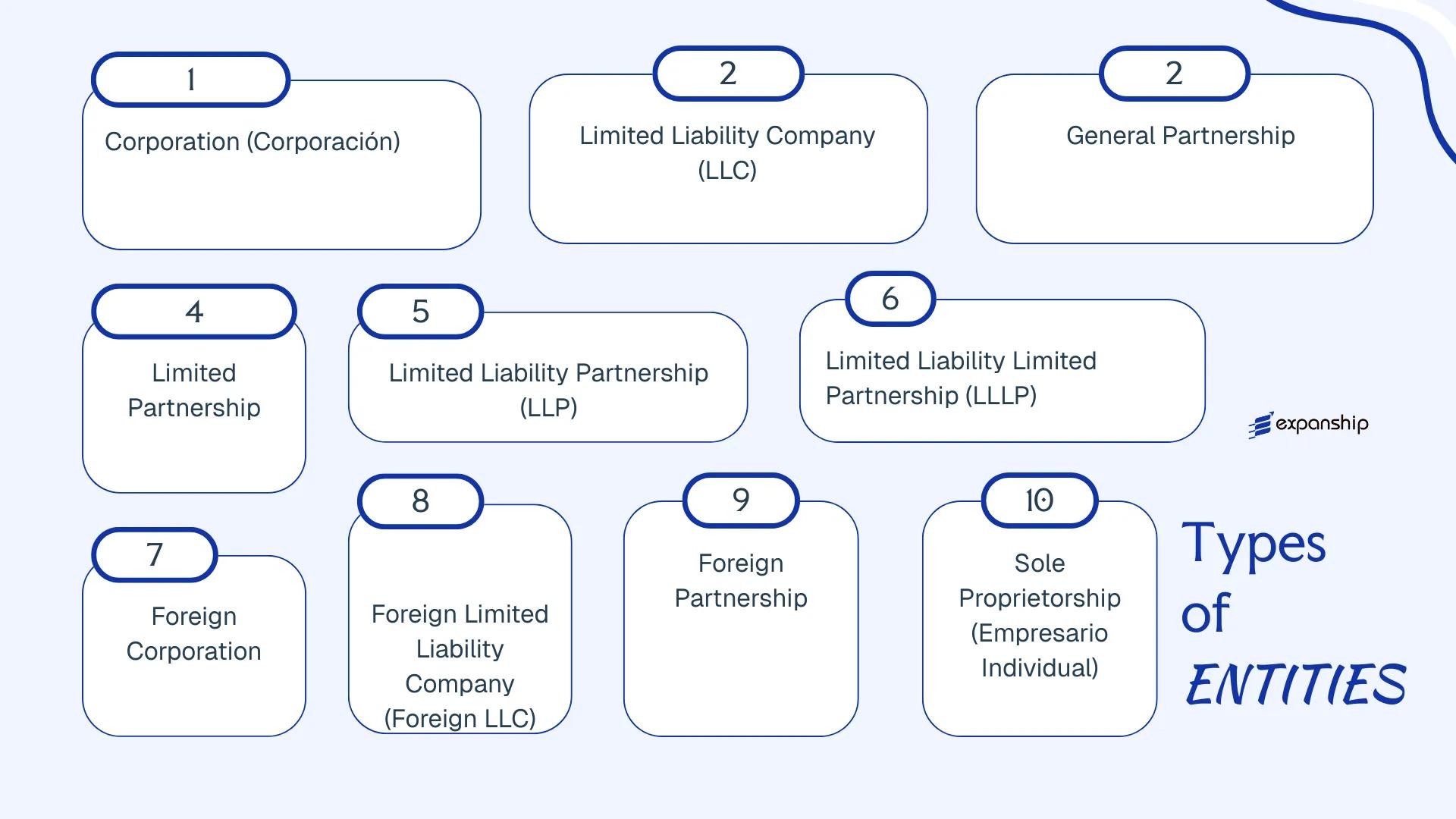

The business entity types available under local law include:

- Corporation (Corporación)

- Limited Liability Company (Compañía de Responsabilidad Limitada)

- General Partnership

- Limited Partnership

- Limited Liability Partnership

- Limited Liability Limited Partnership

- Foreign Corporation

- Foreign LLC

- Foreign Partnership

- Sole Proprietorship (Empresario Individual)

Each structure carries distinct implications for liability, taxation, governance, and compliance. This article examines each form in detail so your business can make an informed decision about the most appropriate structure for its operations.

An Overview of Business Structures in Puerto Rico

Puerto Rico's company law framework accommodates several distinct entity types, each governed primarily by the Puerto Rico General Corporations Act of 2009 (Act 164-2009) and related statutes such as the Special Act for the Creation of the Compañía de Responsabilidad Limitada. Each structure carries a different combination of liability exposure, tax treatment, and administrative obligation.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Corporation (Corporación) | Separate legal entity | Limited to share capital | Corporate-level tax applies | Permitted | 1 shareholder | DACO / State Dept. | Act 164-2009 |

| LLC (CRL) | Separate legal entity | Members limited | Pass-through or corporate | Permitted | 1 member | Dept. of State | CRL Act |

| General Partnership | Contractual entity | Unlimited, joint | Pass-through | Permitted | 2 partners | Dept. of State | Civil Code / Commerce Code |

| Limited Partnership | Hybrid entity | GP unlimited; LP limited | Pass-through | Permitted | 1 GP + 1 LP | Dept. of State | Act 164-2009 |

| LLP | Contractual entity | Partners limited | Pass-through | Permitted | 2 partners | Dept. of State | Act 164-2009 |

| LLLP | Hybrid entity | All partners limited | Pass-through | Permitted | 1 GP + 1 LP | Dept. of State | Act 164-2009 |

| Foreign Corporation | Registered branch | Limited to capital | Corporate-level tax applies | Permitted post-registration | N/A | Dept. of State | Act 164-2009 |

| Foreign LLC | Registered foreign entity | Members limited | Pass-through or corporate | Permitted post-registration | N/A | Dept. of State | CRL Act |

| Foreign Partnership | Registered foreign entity | Varies by home structure | Pass-through | Permitted post-registration | N/A | Dept. of State | Commerce Code |

| Sole Proprietorship | Unincorporated | Unlimited personal | Individual income tax | Permitted | 1 owner | Municipal / Treasury | Civil Code |

Each of these structures is examined in full in the sections below.

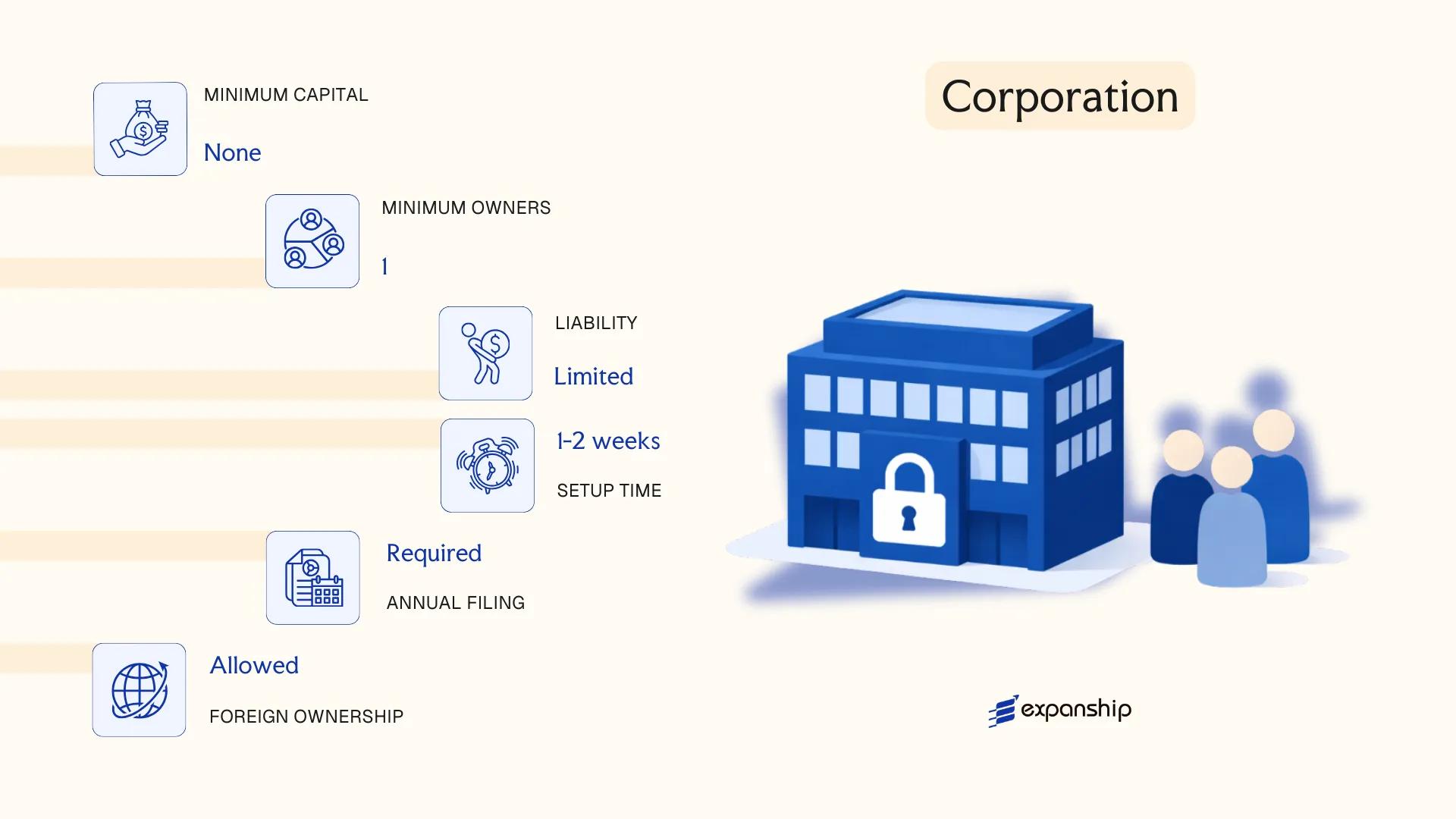

Corporation (Corporación) Under the Puerto Rico General Corporations Act

Governed by the Puerto Rico General Corporations Act (Act No. 164 of 2009, as amended), a corporation is a separate legal entity distinct from its shareholders. This structure confers limited liability on investors, meaning personal assets remain shielded from corporate obligations.

Formation requires filing a Certificate of Incorporation with the Puerto Rico Department of State. The GCA follows a framework closely modeled on Delaware corporate law, making it familiar to U.S. and international counsel alike.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Corporación (Corporation) | Separate legal personality under Act No. 164 of 2009 |

| Members | Shareholders (owners); Directors (management); Officers (operations) | Minimum 1 shareholder, 1 director, 1 officer; no maximum; same person may hold all roles |

| Local Presence | Registered Agent required; registered office in Puerto Rico | Agent must maintain a physical Puerto Rico address |

| Capital | USD; no statutory minimum paid-up capital | Authorized share capital stated in the Certificate of Incorporation |

| Privacy | Shareholder names not required in public filings | Directors may appear in certain filings; beneficial ownership rules apply |

Focus Points

- Taxation: Subject to Puerto Rico corporate income tax at graduated rates up to 18.5%; municipal license tax (patente municipal) applies; Act 60 (formerly Acts 20/22) incentives may reduce rates significantly; no U.S. federal corporate tax on Puerto Rico-sourced income for bona fide residents and qualifying entities; dividend withholding tax applies to distributions.

- Annual Compliance: Annual report and franchise tax due to the Department of State; corporate books must be maintained.

- Economic Substance: No formal OECD-style substance test, but Act 60 incentive holders must meet employment and investment thresholds to retain decree benefits.

- Conversion: A corporation may convert to an LLC or other entity type under the GCA by filing the appropriate certificate with the Department of State.

- Restrictions: Certain regulated industries (banking, insurance) require additional licensing beyond standard GCA registration.

Sub-Types

Close Corporation

A close corporation restricts share transferability and limits the shareholder count, allowing simplified governance without a formal board structure. Suitable for small, closely held businesses where shareholders prefer direct operational control.

Non-Profit Corporation

Organized for charitable, religious, educational, or civic purposes, this variant foregoes profit distribution to members. It may qualify for Puerto Rico tax-exempt status and, separately, U.S. federal 501(c) recognition.

A Puerto Rico corporation suits holding structures, active trading operations, and IP ownership, particularly when combined with Act 60 tax decrees. The primary limitation is ongoing compliance burden: annual filings, franchise taxes, and, for incentive holders, substance requirements add administrative cost.

Mid-size to large businesses, U.S. and foreign investors seeking Act 60 incentives, and entities that benefit from a well-developed corporate law framework with predictable governance rules.

Company Incorporation in Puerto Rico

Incorporate a corporation or other entity in Puerto Rico with full compliance support across all Department of State requirements.

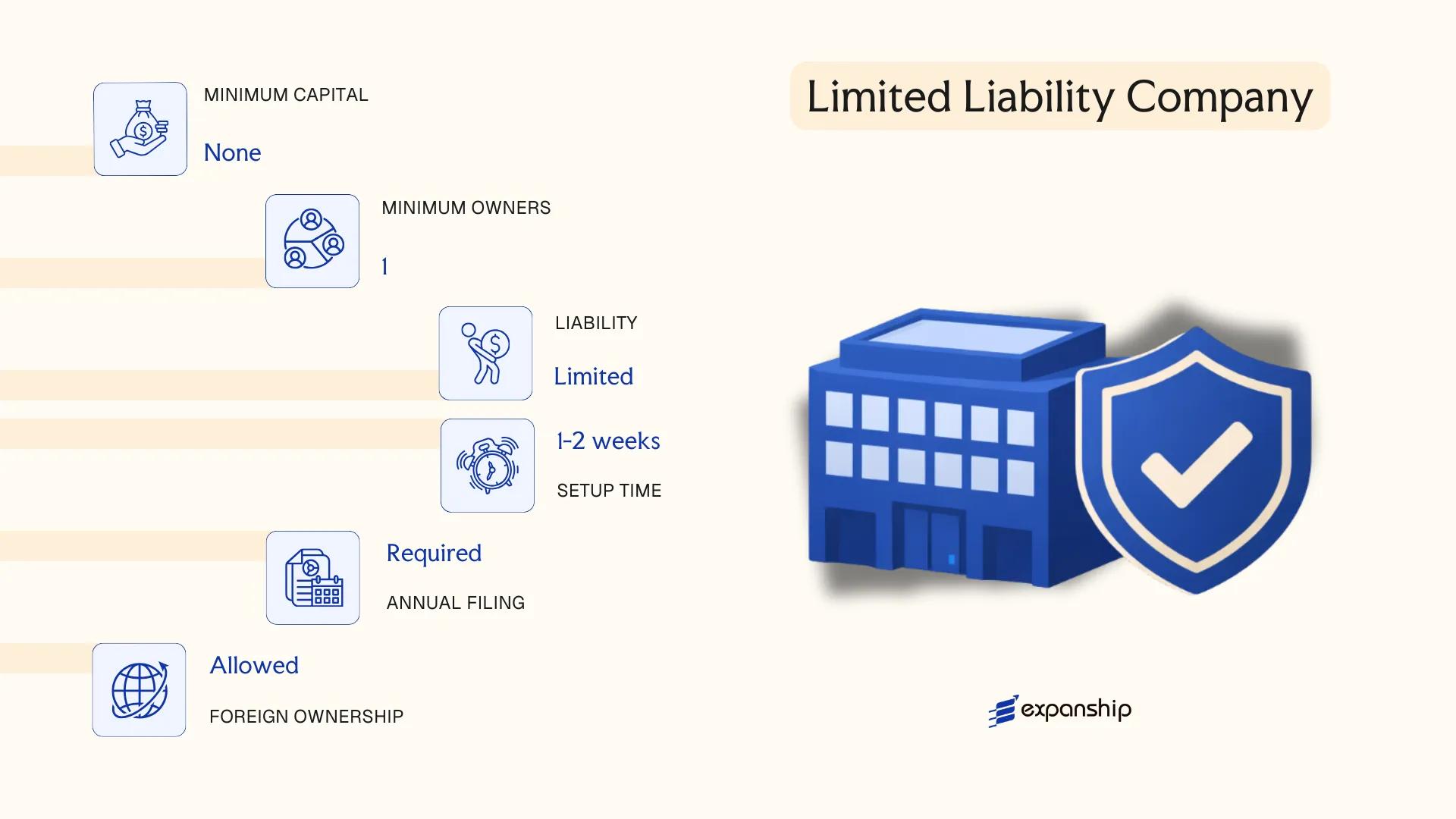

Limited Liability Company (LLC / Compañía de Responsabilidad Limitada)

Governed by the Puerto Rico Limited Liability Company Act of 1995 (Act No. 487 of 1995), the Puerto Rico LLC compañía de responsabilidad limitada is a distinct legal entity separate from its members. It combines the liability protection of a corporation with the structural flexibility of a partnership.

Members are not personally liable for the debts or obligations of the business. The operating agreement — known as the acuerdo operacional — governs internal affairs and may be structured with considerable freedom, though its existence is a legal requirement under Act 487.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Compañía de Responsabilidad Limitada (CRL) | Registered with the Puerto Rico Department of State |

| Member Terminology | Members (Miembros); may appoint Managers (Gerentes) | Member-managed or manager-managed structure permitted |

| Members | Minimum 1; no maximum; domestic or foreign nationals permitted | Single-member LLCs are recognised |

| Local Presence | Registered Agent with a Puerto Rico address required | No mandatory local office beyond registered agent |

| Capital | USD; no statutory minimum capital requirement | Contributions may be cash, property, or services |

| Privacy | Member names not publicly disclosed on formation documents | Operating agreement is a private document |

Focus Points

- Taxation: Treated as a pass-through entity by default for U.S. federal tax purposes; subject to Puerto Rico income tax rules, with potential benefits under Act 60 (formerly Acts 20/22) for qualifying businesses; no separate Puerto Rico sales and use tax (IVU) exemption solely by entity type.

- Annual Compliance: Annual report (informe anual) filed with the Department of State; failure to file can result in administrative dissolution.

- Economic Substance: No specific economic substance legislation comparable to certain offshore jurisdictions, but Act 60 incentive holders must meet local employment and investment thresholds.

- Conversion: Act 487 permits conversion from other entity types into a CRL, subject to filing requirements with the Department of State.

- Restrictions: Certain regulated industries, including banking and insurance, may not use the LLC structure without specific authorisation.

A Puerto Rico LLC suits holding structures, service businesses, and Act 60-incentivised operations where pass-through taxation and operational flexibility are priorities. The absence of a minimum capital requirement lowers the formation threshold, though the mandatory operating agreement adds a layer of upfront structuring work.

Best suited for U.S.-connected businesses and individual entrepreneurs seeking pass-through tax treatment combined with limited liability, particularly those exploring Act 60 incentive eligibility.

Partnerships [General Partnership, Limited Partnership, Limited Liability Partnership, Limited Liability Limited Partnership]

Puerto Rico partnership structures are governed by the Puerto Rico General Corporations Act of 2009 (Act 164-2009), which modernized and consolidated the rules applicable to these entities. Puerto Rico limited liability partnership registration follows a filing-based process with the Puerto Rico Department of State, and each partnership variant carries distinct liability and governance characteristics.

Unlike a simple contractual arrangement, registered partnerships in Puerto Rico are recognized as separate legal entities capable of holding property, entering contracts, and incurring liabilities in their own name.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (Sociedad) | Separate legal personality upon registration with the PR Department of State |

| Members Referred To As | Partners (Socios) | General Partners and/or Limited Partners depending on structure |

| Membership | Minimum 2 partners; no statutory maximum | At least one General Partner required in LP and LLLP structures |

| Local Presence | Registered Agent with a Puerto Rico address required | Physical office not mandated, but a local registered agent is compulsory |

| Capital | No minimum capital requirement; contributions in cash, property, or services | USD denomination standard |

| Privacy | Partner names appear in formation documents filed publicly with the Department of State | No beneficial ownership registry specific to partnerships currently |

Focus Points

- Taxation: Partnerships are treated as pass-through entities for Puerto Rico income tax purposes under Act 1-2011 (Internal Revenue Code of Puerto Rico); partners report distributive shares on individual returns. Federal U.S. tax rules also apply given Puerto Rico's territory status. No separate VAT applies to partnership income distributions, though the general SUT (Sales and Use Tax) applies to applicable transactions.

- Annual Compliance: Annual reports must be filed with the Puerto Rico Department of State; failure to file can result in administrative dissolution.

- Economic Substance: No formal economic substance regime equivalent to certain offshore jurisdictions applies, but actual business activity is relevant for tax treatment.

- Conversion: Act 164-2009 permits conversion between partnership types and to other entity forms through a formal filing process.

- Restrictions: General partners in an LP or LLLP bear unlimited personal liability unless the LLLP shield is properly established and maintained.

Sub-Types

General Partnership (Sociedad General)

All partners share management authority and bear joint and unlimited personal liability for partnership obligations. Typically used for small professional or family business arrangements where liability exposure is accepted.

Limited Partnership (Sociedad en Comandita)

At least one general partner retains unlimited liability while limited partners contribute capital and enjoy liability protection capped at their investment, provided they do not participate in management. Commonly used for investment vehicles and family wealth structures.

Limited Liability Partnership (Sociedad de Responsabilidad Limitada de Socios)

Each partner receives a liability shield against obligations arising from the acts or omissions of other partners, while remaining liable for their own conduct. Frequently adopted by professional service firms.

Limited Liability Limited Partnership (LLLP)

The LLLP extends liability protection to general partners as well, combining the structural flexibility of a limited partnership with broader personal liability shielding. This is the least commonly used variant but suits complex multi-tier investment arrangements.

Closing

Partnerships suit professional services, joint ventures, and investment holding arrangements where pass-through taxation is a priority. The principal limitation is that general partnerships and improperly maintained LP structures expose at least one partner to unlimited personal liability.

Puerto Rico partnership structures are most appropriate for professional firms and investment co-ownership arrangements where two or more parties require pass-through tax treatment and can accept the liability trade-offs of their chosen variant.

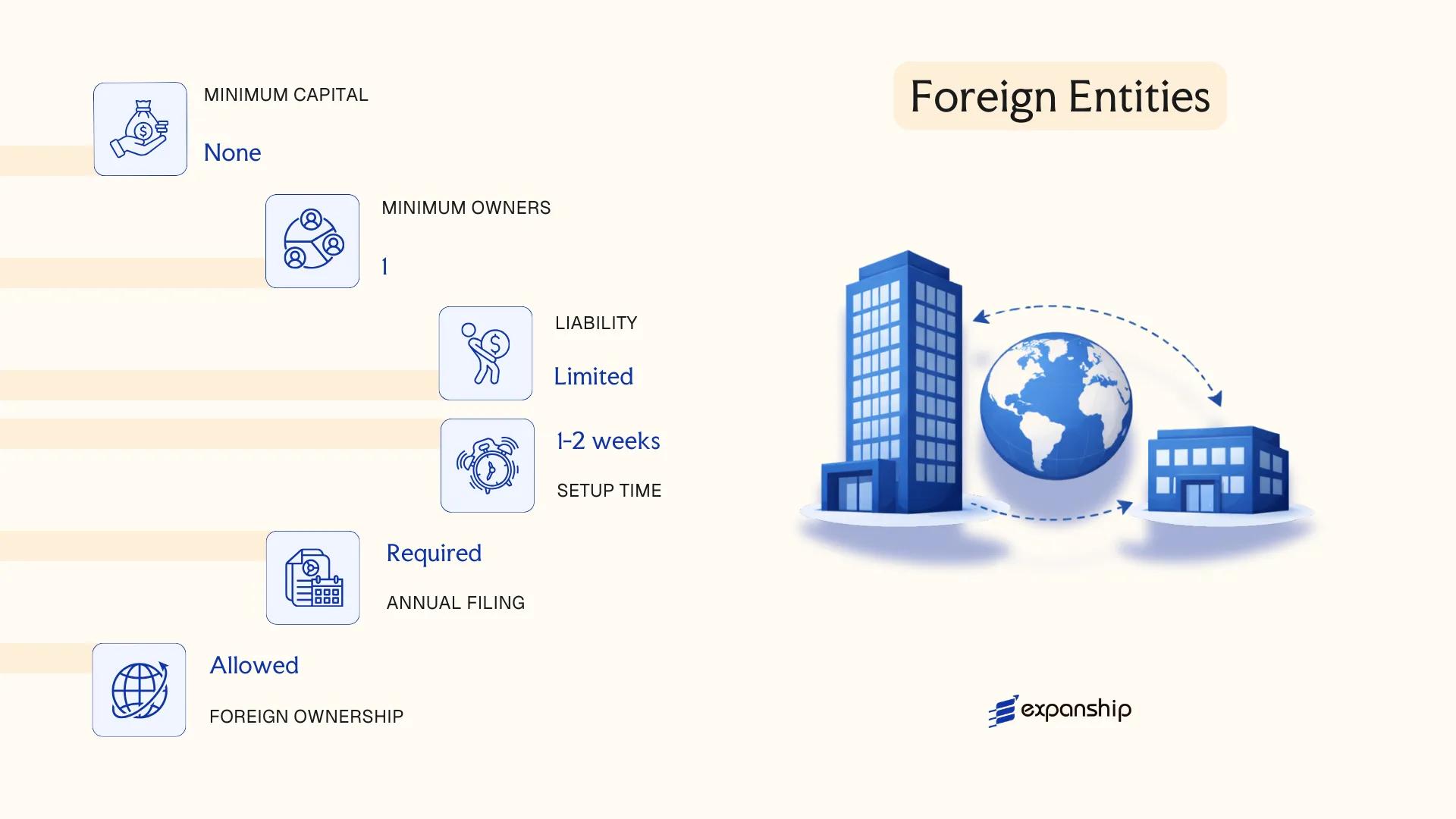

Foreign Entities in Puerto Rico [Foreign Corporation, Foreign LLC, Foreign Partnership]

Businesses incorporated outside of Puerto Rico that wish to conduct business within the territory must register with the Puerto Rico Department of State. Foreign corporation registration in Puerto Rico is governed by the Puerto Rico General Corporations Act of 2009 (Act 164-2009), while foreign LLCs and partnerships follow parallel registration requirements under their respective statutes. Registration does not create a new legal entity — the foreign firm retains its original legal personality and structure from its home jurisdiction.

Qualification grants the entity the legal authority to transact business locally. Without it, a foreign business may be denied access to local courts and face civil penalties, though the threshold for what constitutes "doing business" is determined by statute.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Foreign Corporation, Foreign LLC, or Foreign Partnership | Retains legal form of home jurisdiction |

| Governing Authority | Puerto Rico Department of State | Administers the Puerto Rico foreign entity certificate of authority |

| Registered Agent | Required — must be resident in Puerto Rico | Mandatory for service of process |

| Certificate of Good Standing | Required from home jurisdiction | Must accompany registration application |

| Filing Fee | Varies by entity type | Confirm current schedule with Department of State |

| Privacy | Officers/members disclosed in filings | Public record upon registration |

Focus Points

- Taxation: Foreign entities operating in Puerto Rico are subject to local corporate income tax and municipal license taxes on Puerto Rico-sourced income; Act 60-2019 may offer incentive-based rate reductions depending on activity type.

- Annual Compliance: Annual reports must be filed with the Department of State to maintain good standing and certificate of authority.

- Restrictions: Certain regulated industries require additional licensing beyond the standard qualification process.

- Treaty Access: Puerto Rico is a U.S. territory; U.S. federal tax treaties do not automatically apply, and the territory has no separate bilateral tax treaty network.

Closing

Foreign qualification suits businesses already established elsewhere that need an operational presence in the territory without restructuring their existing corporate form. The primary advantage is continuity of legal identity; the main limitation is dual compliance — the entity must meet both home-jurisdiction and local requirements simultaneously.

Foreign qualification is best suited for established U.S. or international companies seeking to extend operations into Puerto Rico without forming a separate local entity.

Sole Proprietorship (Empresario Individual)

A sole proprietorship Puerto Rico empresario individual is the simplest form of business operation available on the island. Unlike corporations or LLCs, it carries no separate legal personality — the business and the owner are legally the same entity, meaning personal assets are fully exposed to business liabilities.

Registration does not create a distinct legal person. Instead, you are conducting trade under your own name or a trade name (DBA), and obligations arise directly against you as the individual.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated; no separate legal personality | Owner and business are one and the same |

| Owner Title | Sole Proprietor (Empresario Individual) | Single natural person only |

| Ownership | 1 individual; no maximum or minimum beyond that | Cannot be held by a legal entity |

| Local Presence | Trade name registration with the Puerto Rico Department of State if operating under a DBA | No registered agent requirement |

| Capital | No statutory minimum; denominated in USD | Fully at owner's discretion |

| Liability | Unlimited personal liability | No liability shield exists |

Focus Points

- Taxation: Subject to Puerto Rico individual income tax rates on net business income; also required to file and remit sales and use tax (IVU) if selling taxable goods or services; self-employment contributions apply under the Puerto Rico Social Security equivalents.

- Registration: A trade name (DBA) must be registered with the Departamento de Estado de Puerto Rico; a municipal patent (patente municipal) is required in the municipality of operation.

- Annual Compliance: Must file an annual volume of business declaration with the municipality and maintain IVU filings with the Departamento de Hacienda.

- Federal Obligations: As a U.S. territory, self-employed individuals may have federal self-employment tax exposure depending on residency and income sourcing rules under IRC Section 933.

- Conversion: Can be converted into a formal entity such as an LLC or corporation, but this requires a new registration process rather than a statutory conversion procedure.

Closing

This structure suits freelancers, independent contractors, and small local service providers who operate with low liability exposure and minimal administrative overhead. The primary advantage is simplicity of setup; the clear drawback is unlimited personal liability, which makes it unsuitable for any business carrying financial, legal, or operational risk.

Best suited for individual professionals or self-employed operators in Puerto Rico who have no partners, require no investor capital, and face minimal liability risk in their day-to-day activities.

How to Choose the Right Entity Type in Puerto Rico

Selecting the wrong legal structure has consequences that are difficult and costly to reverse. The decision on how to choose a business entity type in Puerto Rico should be based on your specific operational profile, tax position, and compliance capacity — not on what is most common or convenient.

Why Your Entity Choice Matters

The structure you register today shapes your legal obligations for years. Concrete outcomes of a mismatched choice include:

- Choosing an entity eligible for Act 60 tax incentives without meeting the required substance and residency conditions results in disqualification from the decree and potential clawback of tax benefits.

- Selecting a structure incompatible with your intended banking or regulated activity may require a full re-incorporation, triggering new fees and registration delays with the Puerto Rico Department of State.

- Forming a corporation when a single-member LLC would suffice obligates you to maintain board formalities, hold annual meetings, and file separate corporate records — adding administrative burden without corresponding benefit.

- Choosing a general partnership for a multi-party venture without liability separation exposes each partner personally to the full debts and obligations of the business.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as insurance or investment funds each require distinct structures under Puerto Rico law.

- Tax Objectives: Your eligibility for incentives under the Puerto Rico Incentives Code (Act 60-2019) depends on the entity type you select and whether you can satisfy residency and substance requirements.

- Ownership and Management: A single-owner operation may find the LLC's default pass-through treatment and flexible management structure more proportionate than a multi-director corporate setup.

- Privacy Requirements: Director and officer information for corporations is publicly accessible through the Puerto Rico Department of State's registry; LLCs offer comparatively more flexibility in member disclosure.

- Substance Capacity: If you cannot maintain a genuine operational presence on the island, certain tax incentive regimes will not apply, and the entity type you choose must reflect that constraint.

- Exit Strategy: Not all entities permit redomiciliation or conversion under the Puerto Rico General Corporations Act — verify whether your preferred structure supports those options before incorporating.

Compliance Services for Companies in Puerto Rico

Maintain good standing with the Puerto Rico Department of State and meet your annual filing, reporting, and regulatory obligations.

Conclusion

This Puerto Rico business incorporation conclusion guide brings together the key distinctions across the entity types available under local law. Corporations formed under the Puerto Rico General Corporations Act suit businesses that anticipate outside investment or public offerings. The LLC remains the most widely registered structure, favored for its operating flexibility and pass-through tax treatment. General partnerships carry unlimited personal liability, making them less suitable for ventures with meaningful financial exposure. Limited partnerships serve investment and real estate structures where management and capital roles are separated. Foreign entities registered through the Department of State extend an existing legal structure into the territory without forming a new domestic entity.

Act 60 of 2019 continues to shape formation trends, and ongoing federal oversight through PROMESA means the regulatory environment here evolves differently from U.S. state jurisdictions. Professional guidance aligned with both local and federal frameworks remains relevant when selecting a structure.

How Expanship Can Assist You

Expanship company formation services Puerto Rico cover the full process of establishing your business under the Puerto Rico General Corporations Act or as an LLC registered with the Puerto Rico Department of State. From selecting the right entity structure to meeting Departamento de Estado filing requirements, the work is handled with direct knowledge of local rules — not generalized offshore guidance.

Across both incorporation and ongoing maintenance, the services available to you include:

- Preparation and legalization of formation documents

- Registered agent and registered office provision in Puerto Rico

- Government filing and liaison with the Departamento de Estado

- Post-incorporation compliance management, including annual reports

- Banking introduction assistance for newly formed entities

Reach out through Expanship Puerto Rico to discuss your specific situation with someone who works in this jurisdiction.

Frequently Asked Questions (FAQ)

The Limited Liability Company is the most frequently formed structure, largely because it combines pass-through taxation under Subchapter K of the U.S. Internal Revenue Code with flexible governance arrangements. Single-member and multi-member configurations are both permitted under the LLC Act.

A corporation formed under the General Corporations Act is subject to Puerto Rico corporate income tax as a separate taxable entity, while an LLC is treated as a pass-through by default. Corporations carry heavier ongoing obligations, including annual reports, board requirements, and formal meeting minutes. Both structures may trade locally without restriction.

An LLC generally affords more privacy than a corporation, as member identities are not required in the articles of organization filed with the Department of State. The operating agreement, which governs membership, is a private document. Nominee arrangements are legally permissible but must reflect actual ownership for tax and compliance purposes.

A sole proprietorship and a single-member LLC each require only one individual. Corporations under the General Corporations Act may be formed by a single incorporator. General partnerships and limited partnerships, by definition, require at least two parties, since the partnership relationship is contractual in nature.

Yes. Foreigners may form corporations, LLCs, and partnerships without residency requirements. A registered agent with a physical address in the jurisdiction is mandatory for all entity types. Foreign nationals should also assess whether their activities qualify under Act 60-2019 incentive programs, which carry specific eligibility conditions.

The General Corporations Act permits statutory conversion, allowing a corporation to convert into an LLC and vice versa, provided members or shareholders approve the plan. The converted entity assumes all prior obligations. Not all conversion paths are symmetrical, so legal review of the specific transaction is advisable before filing.

Corporations and LLCs hold separate legal personality, meaning they can contract, own assets, and be sued independently of their owners. General partnerships do not have separate legal personality under Puerto Rico law. Limited partnerships occupy an intermediate position, with the partnership itself recognized as a distinct entity for certain purposes.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.