Key Takeaways

- The Sp. z o.o. is Poland's most widely registered entity, favored for its limited liability structure and manageable capital requirements relative to the S.A. and P.S.A.

- Company registration in Poland is administered through the Krajowy Rejestr Sądowy (KRS), operated under the authority of the Polish Ministry of Justice, with regulated activities subject to additional licensing from bodies such as the KNF.

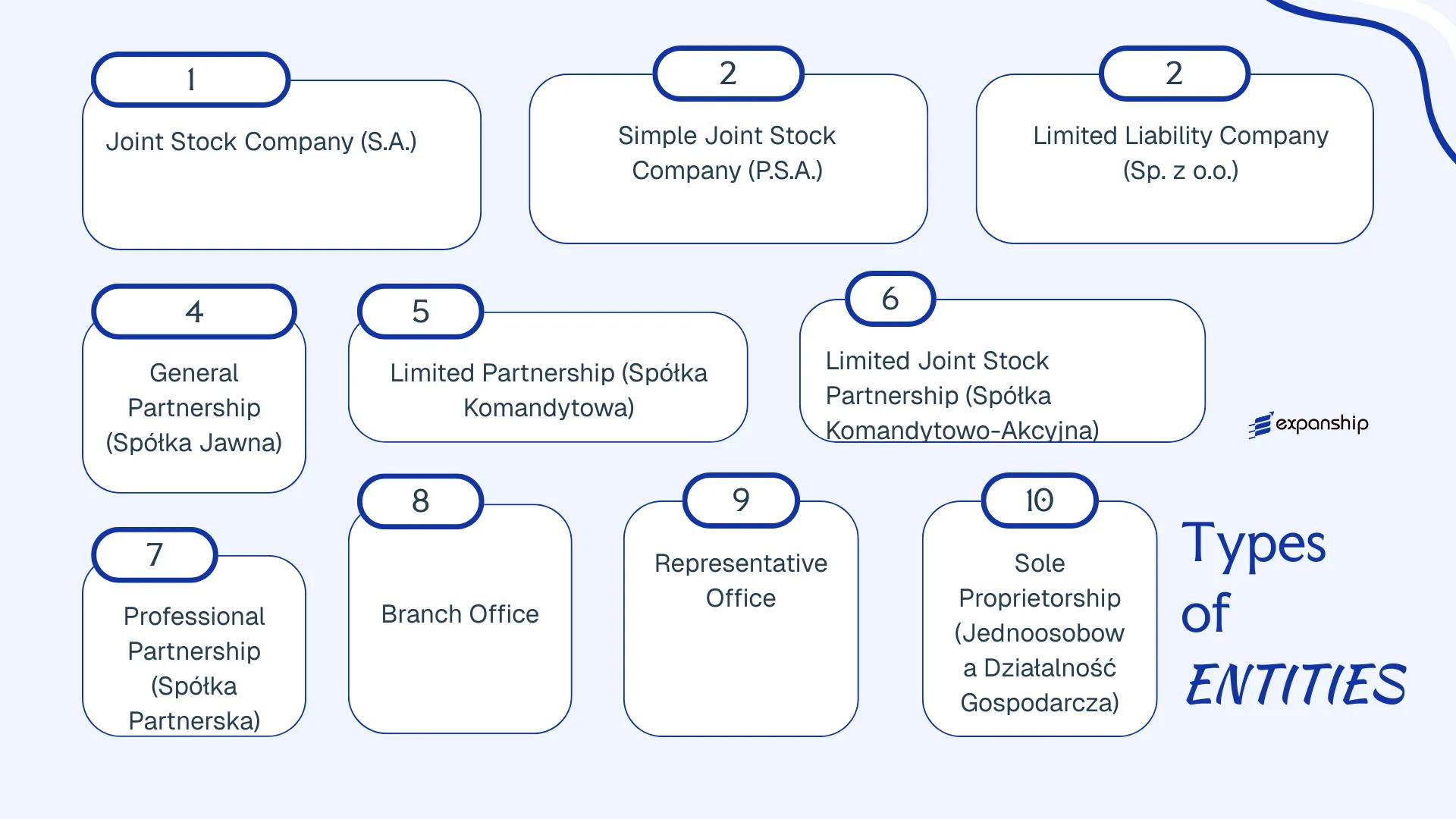

- Poland recognizes at least ten distinct legal forms for business operation, ranging from sole proprietorships (Jednoosobowa Działalność Gospodarcza) to joint stock companies (S.A.), each carrying different liability rules, governance requirements, and tax treatment.

- Foreign businesses entering Poland without establishing a local legal entity typically do so through a branch office or representative office, two structures that differ in their permitted scope of commercial activity.

Introduction to Entity Types in Poland

Poland sits in Central Europe, bordered by Germany to the west, the Czech Republic and Slovakia to the south, Ukraine and Belarus to the east, and Lithuania and the Russian exclave of Kaliningrad to the north. It is an independent EU member state, which means that types of business entities in Poland are subject to both domestic legislation and applicable European Union directives.

Company registration is administered through the Krajowy Rejestr Sądowy (KRS — National Court Register), operated under the authority of the Polish Ministry of Justice. Certain regulated activities require additional licensing from sector-specific bodies such as the Polish Financial Supervision Authority (KNF). Poland operates a standard corporate tax regime with a flat CIT rate and a reduced rate available for qualifying smaller entities and new firms.

Businesses operating in or from Poland may establish one of several legal forms: Spółka z Ograniczoną Odpowiedzialnością (Sp. z o.o.), Spółka Akcyjna (S.A.), Prosta Spółka Akcyjna (P.S.A.), Spółka Jawna, Spółka Komandytowa, Spółka Komandytowo-Akcyjna, Spółka Partnerska, a Branch Office, a Representative Office, or a Sole Proprietorship (Jednoosobowa Działalność Gospodarcza).

Each structure carries distinct liability rules, governance requirements, and tax treatment — all of which the sections that follow examine in detail.

An Overview of Business Structures in Poland

Polish company law recognises seven distinct entity types, governed primarily by the Commercial Companies Code (Kodeks spółek handlowych, or KSH) of 15 September 2000. Alongside these, sole traders operate under the Entrepreneurs' Law (Prawo przedsiębiorców) of 6 March 2018. Each structure carries a different liability profile, capital requirement, and ownership framework.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Spółka Akcyjna (S.A.) | Joint Stock Company | Shareholders limited to shares | CIT taxable | Yes | 1 shareholder | KRS / KNF (if listed) | KSH |

| Prosta Spółka Akcyjna (P.S.A.) | Simple Joint Stock Company | Shareholders limited to shares | CIT taxable | Yes | 1 shareholder | KRS | KSH |

| Spółka z o.o. (Sp. z o.o.) | Limited Liability Company | Members limited to capital | CIT taxable | Yes | 1 member | KRS | KSH |

| Spółka Jawna | General Partnership | Partners bear unlimited liability | PIT / CIT transparent | Yes | 2 partners | KRS | KSH |

| Spółka Komandytowa | Limited Partnership | Mixed: general / limited | CIT taxable | Yes | 2 partners | KRS | KSH |

| Spółka Komandytowo-Akcyjna | Limited Joint Stock Partnership | Mixed: general / shareholders | CIT taxable | Yes | 2 partners | KRS | KSH |

| Spółka Partnerska | Professional Partnership | Partners limited in scope | PIT / CIT transparent | Yes | 2 licensed partners | KRS | KSH |

| Branch Office | Registered Branch | Parent bears full liability | CIT on Polish-source income | Yes | Parent company | KRS | Act on Foreign Trade |

| Representative Office | Non-trading presence | Parent bears full liability | Limited scope; not trading | No | Parent company | Ministry of Economy | Act on Foreign Trade |

| Sole Proprietorship (JDG) | Sole Trader | Owner bears unlimited liability | PIT taxable | Yes | 1 owner | CEIDG | Prawo przedsiębiorców |

Each of these structures is examined in full in the sections below.

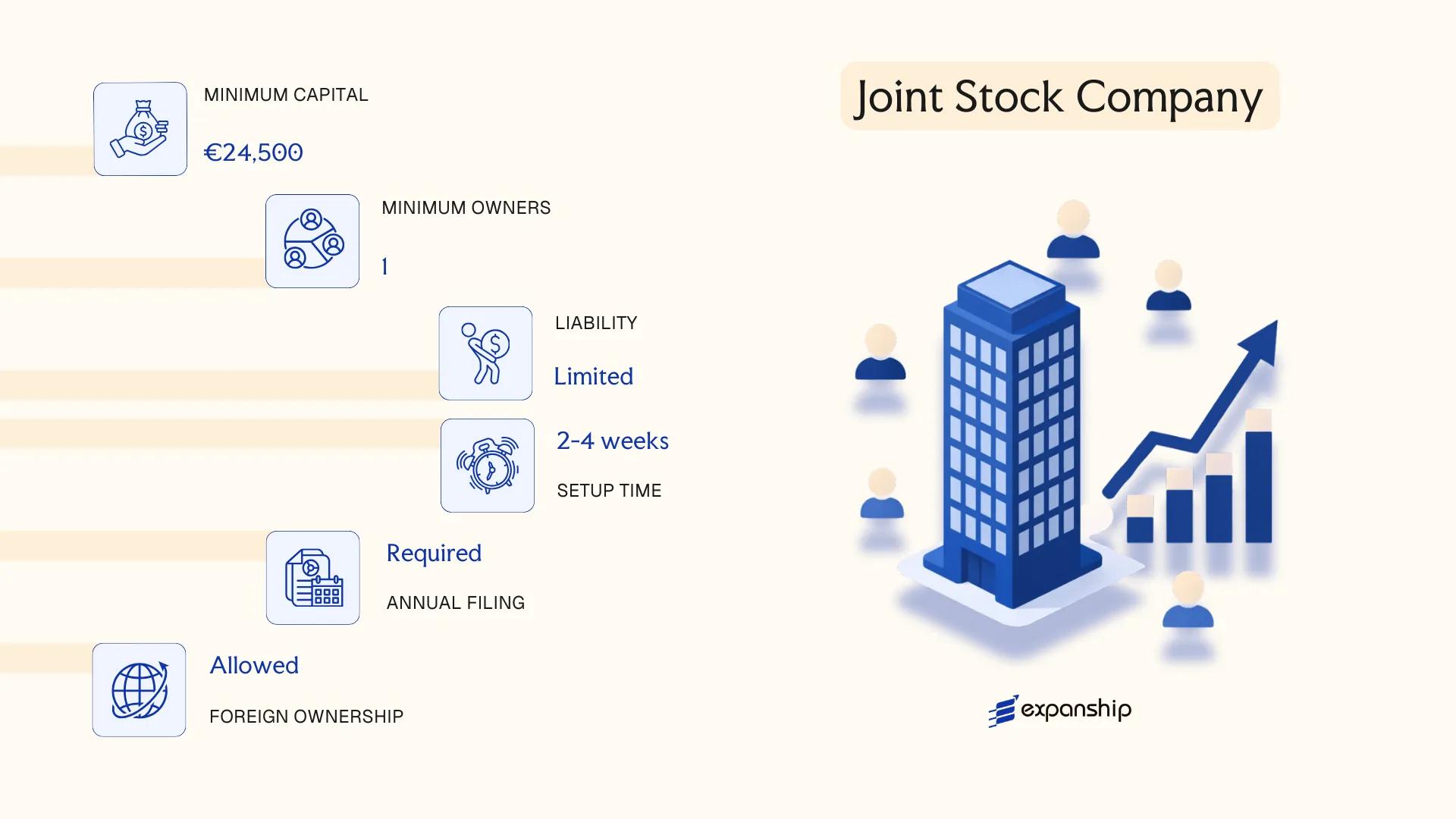

Spółka Akcyjna (S.A.) — Joint Stock Company

The Spółka Akcyjna joint stock company Poland framework is governed by the Code of Commercial Companies (Kodeks spółek handlowych), enacted in 2000. The S.A. carries full separate legal personality, meaning the entity holds rights and obligations independently of its shareholders.

Shareholders bear no personal liability beyond the value of their subscribed shares. The structure suits businesses that require access to capital markets, including those planning a public listing on the Warsaw Stock Exchange (GPW).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Spółka Akcyjna (S.A.) | Regulated under the Kodeks spółek handlowych, 2000 |

| Members | Shareholders: minimum 1; no maximum | Single-shareholder S.A. is permitted; shareholders hold shares, not quotas |

| Governing Bodies | Management Board (Zarząd) + Supervisory Board (Rada Nadzorcza) | Supervisory Board is mandatory; minimum 3 members |

| Minimum Share Capital | PLN 100,000 | At least 25% must be paid up at incorporation |

| Registered Office | Must maintain a registered address in Poland | No statutory requirement for a local director |

| Share Types | Registered shares and bearer shares (restricted) | Bearer shares are subject to dematerialisation requirements under current law |

| Privacy | Shareholder register kept internally; Management Board disclosed in KRS | Beneficial ownership reported to CRBR (Central Register of Beneficial Owners) |

Focus Points

- Taxation: Subject to Corporate Income Tax (CIT) at 19% standard rate (9% reduced rate for small taxpayers); VAT registration required for taxable supplies; dividend distributions subject to 19% withholding tax, reducible under applicable tax treaties or the EU Parent-Subsidiary Directive.

- Annual Compliance: Financial statements must be prepared under Polish Accounting Act standards (or IFRS for listed entities), approved by the Supervisory Board, and filed with the National Court Register (KRS).

- Treaty Access: As a Polish tax-resident entity, the S.A. accesses Poland's network of double taxation treaties.

- Conversion: An S.A. may be converted into other commercial company forms, including Sp. z o.o. or P.S.A., through a formal transformation procedure under the Kodeks spółek handlowych.

- Public Offering: An S.A. is the only Polish entity form eligible to list shares on the GPW main market; this requires compliance with Polish Financial Supervision Authority (KNF) regulations.

Closing

The S.A. suits large enterprises, joint ventures with multiple institutional investors, and businesses planning a public capital raise. Its mandatory dual-board structure provides strong governance but also creates administrative overhead that smaller businesses may find disproportionate.

Large or growth-stage companies planning institutional investment rounds or a future public listing on the Warsaw Stock Exchange.

Company Incorporation in Poland

Register your business entity in Poland with end-to-end support from Expanship.

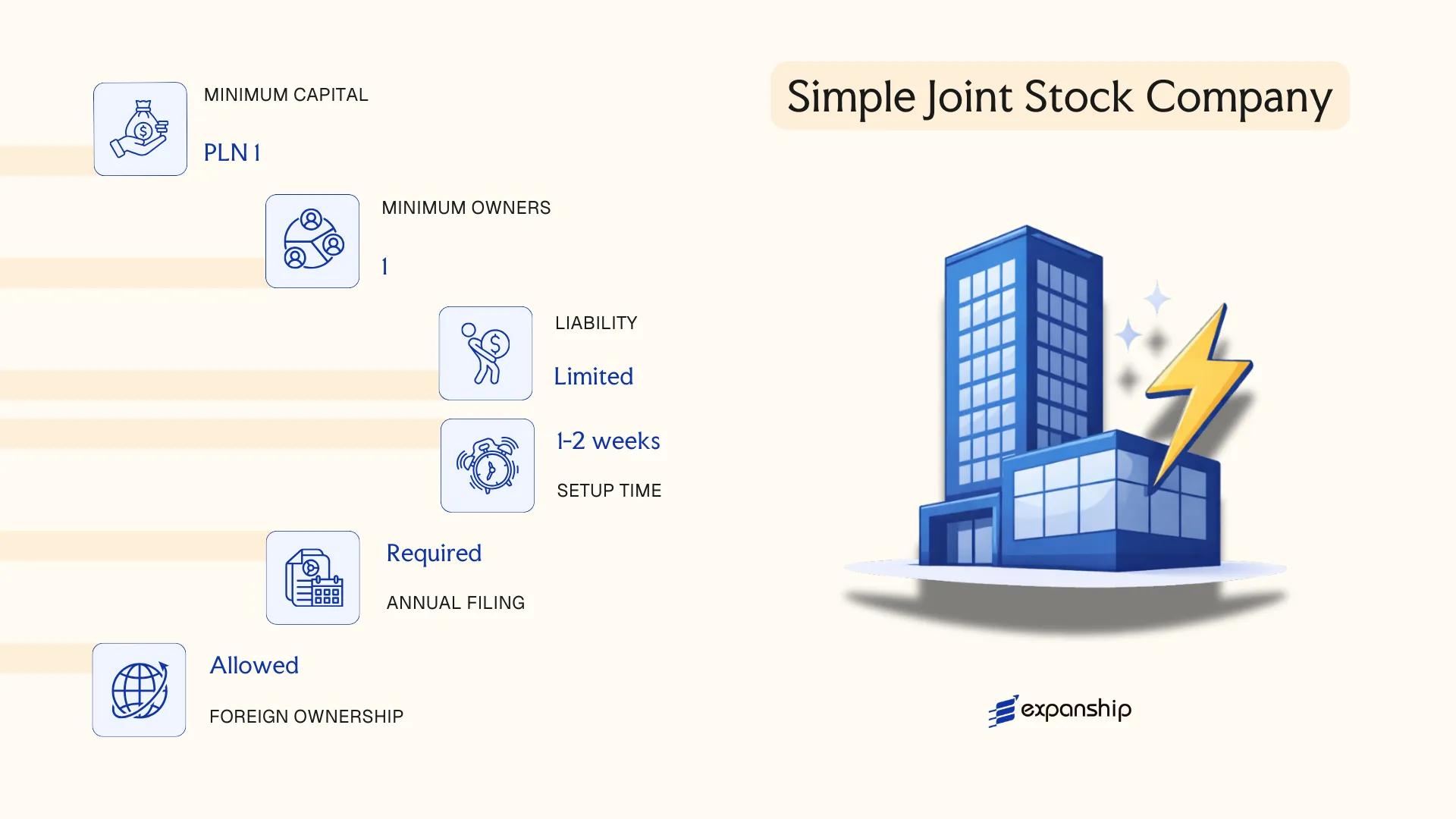

Prosta Spółka Akcyjna (P.S.A.) — Simple Joint Stock Company

Introduced under the Act of 19 July 2019 amending the Polish Commercial Companies Code, Prosta Spółka Akcyjna registration Poland became available from 1 July 2021. The P.S.A. was designed to address the limitations of existing corporate forms for early-stage and technology-driven businesses.

As a separate legal entity, the PSA company Poland provides shareholders with full limited liability. Its structure is deliberately hybrid — combining share capital flexibility from the joint stock model with governance simplicity closer to that of a limited liability company.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Simple Joint Stock Company (Prosta Spółka Akcyjna) | Governed by Articles 3001–30013 of the Commercial Companies Code |

| Members | Shareholders (akcjonariusze); min. 1, no maximum | Single-member formation permitted; shareholders bear no personal liability |

| Governance | Board of Directors or Supervisory Board + Management Board | Flexible one-tier or two-tier structure permitted |

| Registered Office | Registered address required in Poland | No statutory registered agent requirement |

| Share Capital | Minimum PLN 1 | Shares have no nominal value; capital contributions may include labour or services |

| Privacy | Shareholder data filed with KRS (National Court Register) | Beneficial owners registered in CRBR (Central Register of Beneficial Owners) |

Focus Points

- Taxation: Subject to standard CIT at 19% (or 9% reduced rate for small taxpayers); VAT applies at 23% standard rate; withholding tax on dividends generally 19%, subject to EU directives or tax treaty relief; no stamp duty on share capital contributions under standard rules.

- Annual Compliance: Annual financial statements must be filed with KRS; shareholder meeting required annually.

- Conversion: May be converted into a Spółka z o.o. or S.A. under standard transformation procedures in the Commercial Companies Code.

- Dematerialised Shares: All shares are dematerialised and must be registered in a shareholder registry; no physical share certificates are issued.

- Dissolution: Simplified liquidation procedure available, including dissolution without liquidation under specific conditions.

Closing

The simple joint stock company Poland structure suits founders of startups and innovation-driven ventures who require flexible equity arrangements, including the ability to contribute intellectual work as capital — though the absence of nominal share value can create complexity in certain cross-border investment or financing transactions.

The P.S.A. is best suited for technology startups, co-founder teams, and venture-backed businesses that need equity flexibility and a lean corporate structure from day one.

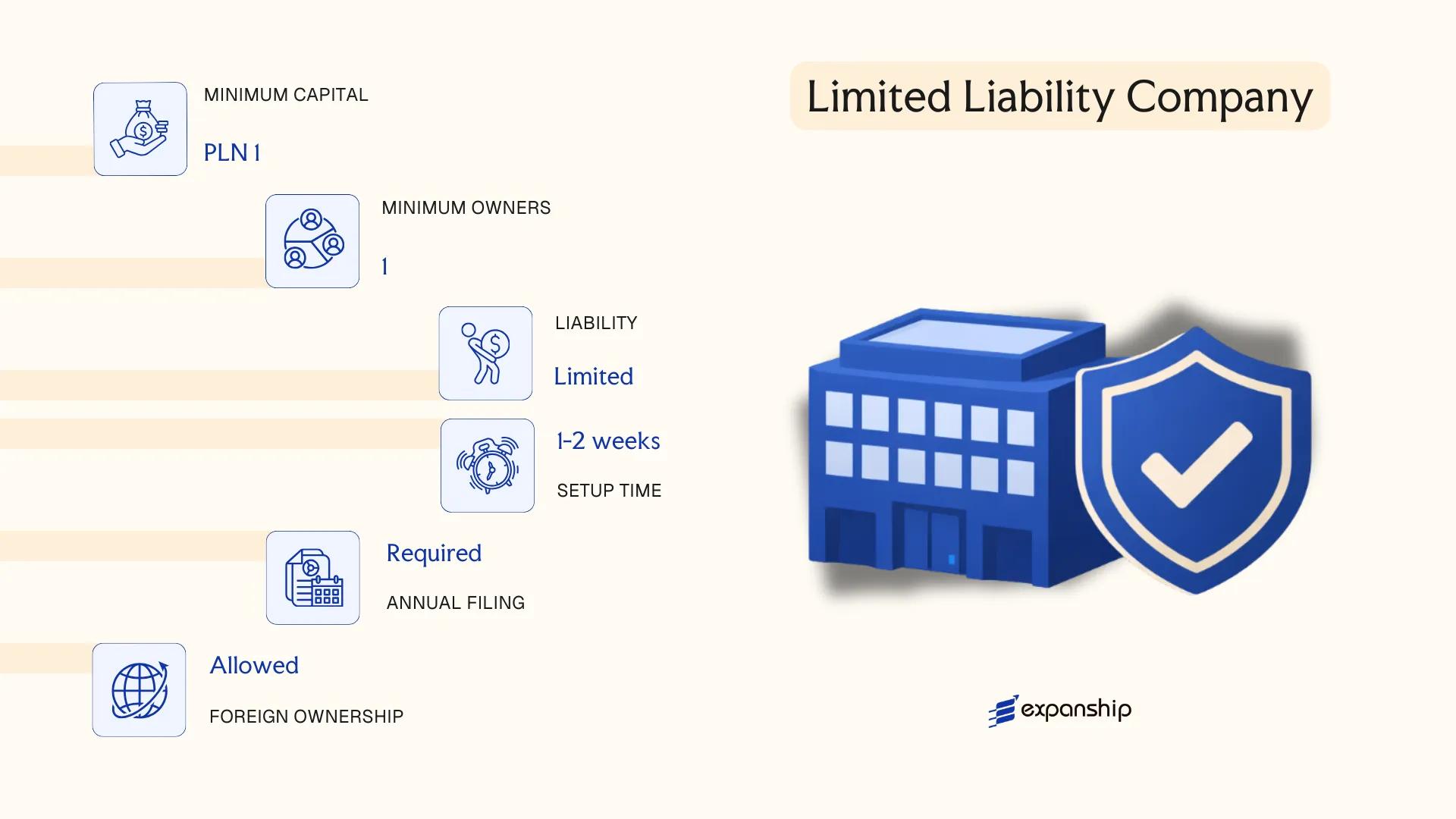

Spółka z Ograniczoną Odpowiedzialnością (Sp. z o.o.) — Limited Liability Company

Governed by the Polish Commercial Companies Code (Kodeks spółek handlowych, enacted in 2000), the Sp. z o.o. is the most widely used vehicle for Spółka z oo company formation Poland. It holds separate legal personality from its shareholders, meaning the entity owns assets, enters contracts, and incurs liabilities in its own name.

Shareholders bear no personal liability for the company's debts beyond the value of their subscribed shares. This hybrid character — combining corporate liability protection with relatively flexible internal governance — makes the structure accessible to both domestic operators and foreign investors.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private limited liability company | Regulated under the Kodeks spółek handlowych (KSH) |

| Members | Shareholders (wspólnicy); minimum 1, no statutory maximum | Cannot be formed solely by another single-member Sp. z o.o. |

| Management | Management Board (Zarząd); minimum 1 member | Supervisory Board optional unless share capital exceeds PLN 500,000 or shareholders exceed 25 |

| Registered Office | Must maintain a registered address in Poland | No mandatory local director requirement |

| Share Capital | Minimum PLN 5,000; minimum share value PLN 50 | Sp. z o.o. minimum share capital Poland is among the lowest for capital companies |

| Privacy | Shareholders listed in the National Court Register (KRS); beneficial owners disclosed in CRBR | Limited privacy; both registers are publicly accessible |

Focus Points

- Taxation: Subject to 19% CIT (9% reduced rate for small taxpayers); standard VAT at 23%; withholding tax applies to dividends, interest, and royalties paid abroad; no stamp duty on share transfers, though civil law transaction tax (PCC) may apply.

- Annual Compliance: Mandatory annual financial statements filed with KRS; audit required if two of three thresholds are exceeded (50 employees, PLN 5M net revenue, PLN 2.5M total assets).

- Economic Substance: No formal substance test, but tax residency and CFC rules under Polish corporate tax law require genuine management and control to be exercised locally.

- Treaty Access: As a tax resident entity, eligible for Poland's extensive double tax treaty network covering 80+ jurisdictions.

- Conversion: Statutory conversion to S.A., P.S.A., or partnership forms is permitted under KSH without dissolving the entity.

Closing

The Sp. z o.o. suits trading operations, holding structures, and Polish limited liability company setup for regional subsidiaries of foreign groups. Its low capital threshold accelerates market entry, though the public disclosure of shareholder identity in KRS limits its suitability where ownership confidentiality is a priority.

Foreign investors and SMEs seeking a straightforward Polish operating entity with capped liability and access to EU market advantages.

Partnerships in Poland [Spółka Jawna (General Partnership), Spółka Komandytowa (Limited Partnership), Spółka Komandytowo-Akcyjna (Limited Joint Stock Partnership), Spółka Partnerska (Professional Partnership)]

Partnership structures in Poland are governed by the Code of Commercial Companies and Partnerships (Kodeks spółek handlowych), enacted in 2000 (Journal of Laws 2000, No. 94, item 1037). Four distinct partnership forms exist under this legislation, each carrying different liability profiles and membership requirements.

Three of the four forms — Spółka Jawna, Spółka Komandytowa, and Spółka Komandytowo-Akcyjna — lack separate legal personality in the traditional sense, though they can acquire rights and incur obligations in their own names. Spółka Partnerska is reserved exclusively for licensed professionals such as attorneys, physicians, and architects.

Key Characteristics

| Requirement | Spółka Jawna (General Partnership) | Spółka Komandytowa (Limited Partnership) | Spółka Komandytowo-Akcyjna (Limited Joint Stock Partnership) | Spółka Partnerska (Professional Partnership) |

|---|---|---|---|---|

| Legal Form | Unincorporated partnership | Unincorporated partnership | Hybrid — partnership with share capital | Unincorporated professional partnership |

| Members | Partners (wspólnicy); min. 2, no maximum | General partners (komplementariusze) + limited partners (komandytariusze); min. 1 of each | General partners (komplementariusze) + shareholders (akcjonariusze); min. 1 of each | Partners (partnerzy); min. 2; must be licensed professionals |

| Local Presence | Registered office in Poland required | Registered office in Poland required | Registered office in Poland required | Registered office in Poland required |

| Share Capital | None required | None required | Minimum PLN 50,000 | None required |

| Liability | All partners: unlimited personal liability | General partners: unlimited; limited partners: liable up to agreed contribution | General partners: unlimited; shareholders: limited to shares held | Partners generally limited; exceptions apply for acts performed personally |

| Privacy | Partners disclosed in KRS (National Court Register) | All partner classes disclosed in KRS | General partners and shareholders disclosed in KRS | Partners disclosed in KRS |

Focus Points

- Taxation: Spółka Jawna and Spółka Partnerska are fiscally transparent by default — income is taxed at the partner level under PIT or CIT depending on partner type; Spółka Komandytowa has been subject to CIT at the entity level since January 2021; Spółka Komandytowo-Akcyjna is a CIT taxpayer; standard VAT rules apply to all trading activities; dividend withholding tax may apply on profit distributions from CIT-liable entities.

- Annual Compliance: All four forms must be registered in the KRS and file annual financial statements with the Court Register within prescribed deadlines.

- Conversion: Polish law permits conversion between partnership forms and into capital companies via a formal transformation procedure under the Code of Commercial Companies and Partnerships.

- Professional Restrictions: Spółka Partnerska membership is restricted to individuals holding specific regulated professional licences listed exhaustively in Article 88 of the Code.

- Treaty Access: CIT-liable partnerships (Spółka Komandytowa, Spółka Komandytowo-Akcyjna) may access Poland's tax treaty network; fiscally transparent forms distribute treaty eligibility to individual partners.

Sub-Types

Spółka Komandytowo-Akcyjna (Limited Joint Stock Partnership)

This form combines a partnership structure with a share capital component, making it distinct from a standard limited partnership. It is typically used by larger ventures seeking capital from passive investors (shareholders) while retaining operational control within a defined group of general partners.

Closing

Partnerships suit joint ventures between known parties, professional service firms, and structures where pass-through taxation at the partner level is a deliberate planning objective. The main limitation across all forms is that at least one partner class carries unlimited personal liability for entity obligations.

Partnerships are best suited to two or more co-founders — including licensed professionals forming a Spółka Partnerska — who accept defined liability roles and prefer structural flexibility over the formality of a capital company.

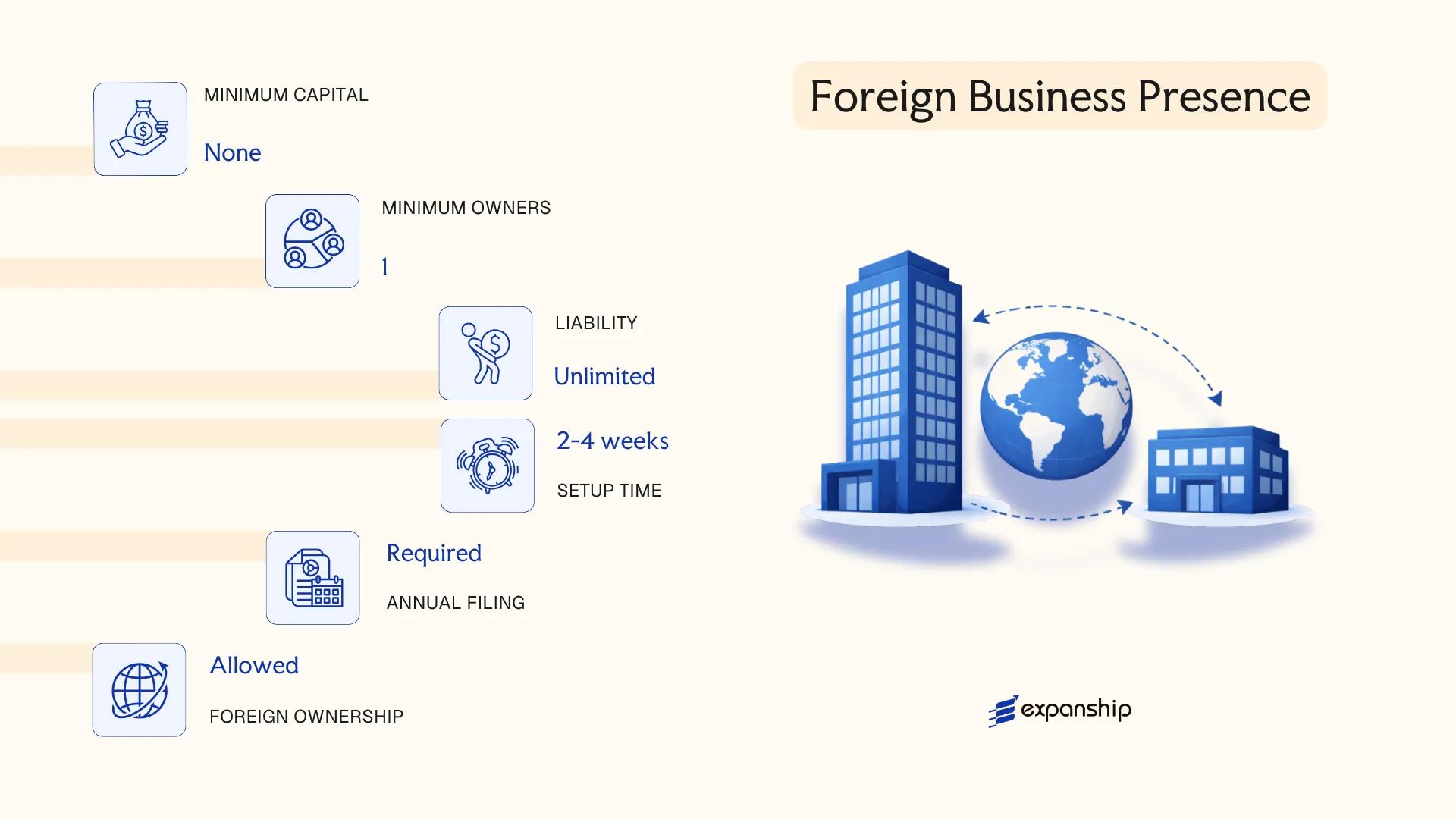

Foreign Business Presence in Poland [Branch Office, Representative Office]

Establishing a foreign company branch office in Poland is governed primarily by the Act on the Rules of Participation of Foreign Entrepreneurs and Other Foreign Persons in Trade on the Territory of the Republic of Poland of 6 March 2018. Neither a branch nor a representative office constitutes a separate legal entity — both remain extensions of the parent company, which bears full legal and financial responsibility for their activities.

Registration is handled through the National Court Register (KRS) for branches and the Ministry of Economic Development and Technology for representative offices. The two forms differ fundamentally in permitted scope: a branch may conduct the same business activities as its parent, while a representative office is restricted to promotional and advertising activities on behalf of the foreign firm.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent entity | None — extension of parent entity |

| Permitted Activities | Same as parent company's statutory scope | Promotion and advertising only |

| Registration Body | National Court Register (KRS) | Ministry of Economic Development and Technology |

| Local Representative | Designated representative required | Designated representative required |

| Registered Address | Required in Poland | Required in Poland |

| Duration | Indefinite | Maximum 2 years; renewable |

Focus Points

- Taxation: Branches are subject to 19% Corporate Income Tax (CIT) on Polish-sourced income; VAT registration is required if taxable turnover thresholds are met; representative offices generally have no taxable income given their restricted scope.

- Transfer Pricing: Branches must maintain arm's-length pricing with their parent and may face transfer pricing documentation obligations under Polish tax law.

- Treaty Access: Branches can access Poland's double tax treaty network as the parent entity is the treaty-eligible person, though treaty relief applies at the parent level.

- Compliance: Branches must file annual financial statements with KRS and maintain separate accounting records under the Polish Accounting Act; representative offices have lighter reporting obligations.

- Restrictions: A representative office cannot generate revenue or enter commercial contracts — any violation risks deregistration by the Ministry.

Closing Paragraph

A branch suits foreign companies seeking an operational footprint without incorporating a separate subsidiary, while a representative office serves firms whose immediate need is market research or brand presence ahead of a fuller market entry.

A branch office is best suited for foreign companies that want direct operational activity in the Polish market without the administrative overhead of a standalone subsidiary; a representative office fits firms in an exploratory or pre-market phase.

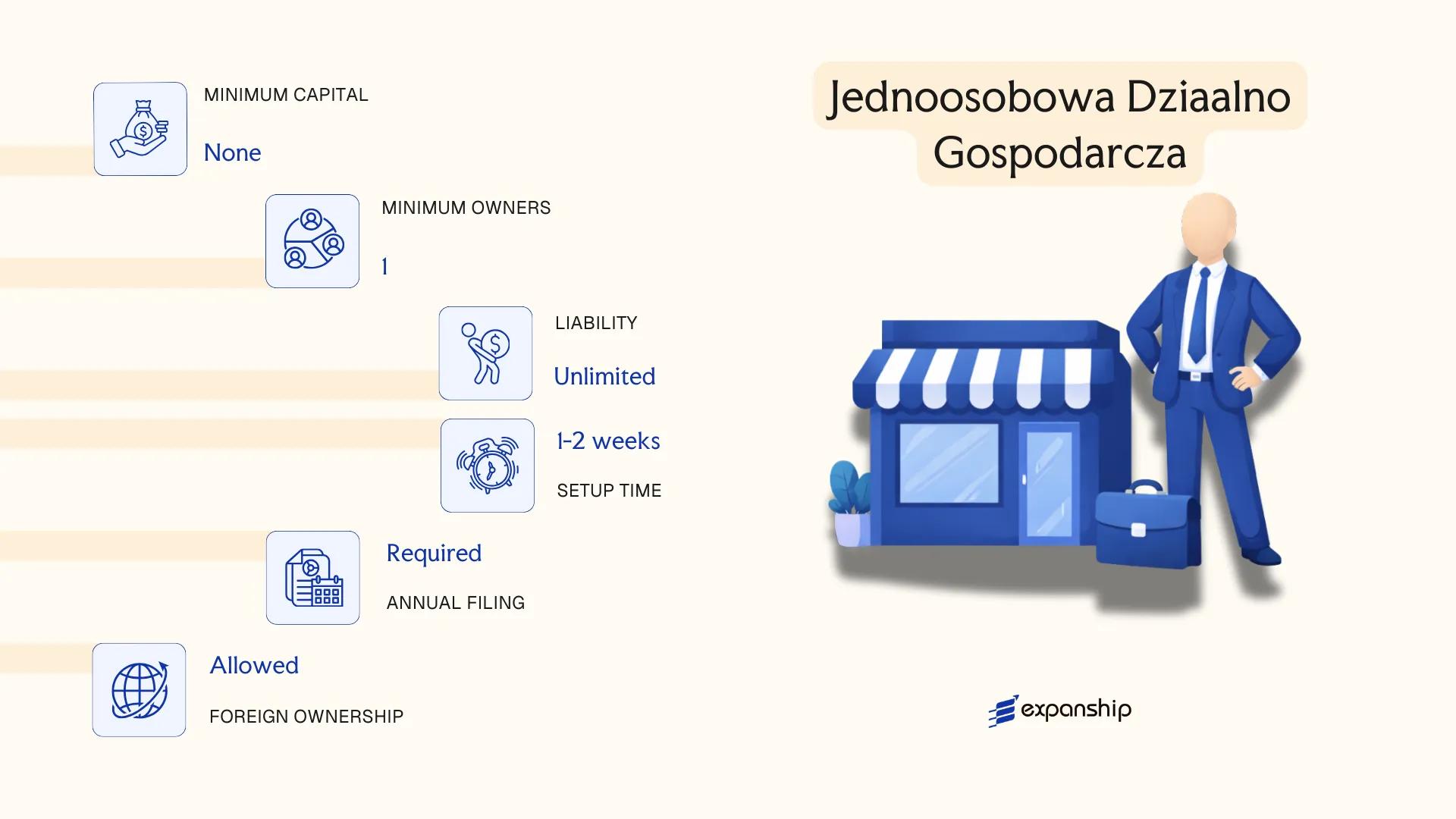

Sole Proprietorship — Jednoosobowa Działalność Gospodarcza

Jednoosobowa Działalność Gospodarcza Poland is the simplest and most widely used form of self-employment available under Polish law. Governed primarily by the Act on Entrepreneurs' Law of 2018 (Prawo przedsiębiorców), it does not create a separate legal entity — the proprietor and the business are legally the same person.

Registration is handled through the Central Register and Information on Business Activity (CEIDG), an online public register administered by the Ministry of Economic Development. Because no share capital is required and the setup process is brief, this structure suits individuals beginning commercial activity without significant upfront investment.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole proprietorship (unincorporated) | No separate legal personality from the owner |

| Member Type | Proprietor | Single natural person only |

| Liability | Unlimited personal liability | Business debts are recoverable against personal assets |

| Registered Address | Required in Poland | Must be a physical address listed in CEIDG |

| Minimum Capital | None | No statutory capital requirement |

| Privacy | Owner's name and address are publicly listed in CEIDG | No beneficial ownership concealment |

Focus Points

- Taxation: Subject to personal income tax (PIT); the proprietor may choose between the progressive scale (12%/32%), flat 19% tax, or lump-sum (ryczałt) rates; VAT registration required once turnover exceeds the statutory threshold; no corporate income tax applies.

- Social Contributions: Mandatory ZUS (Social Insurance Institution) contributions apply from day one, with reduced rates available during the first 24 months of operation.

- Annual Compliance: No annual financial statements are required for entities using simplified tax forms, though full accounting records (księgi rachunkowe) become obligatory once revenue exceeds EUR 2 million.

- Conversion: Can be converted into a Sp. z o.o. through a formalised transformation procedure under the Commercial Companies Code, preserving business continuity.

- Restrictions: Only a natural person may operate this structure; it cannot be used by foreign legal entities seeking a commercial presence.

Closing

This structure suits freelancers, consultants, and small-scale traders who operate alone and do not anticipate significant liability exposure. The absence of minimum capital is an advantage, but unlimited personal liability remains the defining drawback for anyone carrying material financial risk.

Individual Polish residents or EU nationals conducting low-risk, single-person commercial activity who prioritise minimal administrative overhead over liability protection.

How to Choose the Right Entity Type in Poland

Selecting the correct legal structure from the outset determines your tax position, liability exposure, and administrative obligations for as long as the entity remains active.

Why Your Entity Choice Matters

Choosing the wrong structure produces concrete legal and financial consequences:

- A representative office conducting direct commercial activity exceeds its permitted scope under Polish law, exposing the foreign principal to penalties and potential forced closure by the National Court Register (Krajowy Rejestr Sądowy).

- Registering a structure that falls outside Poland's tax treaty network — such as a transparent partnership where treaty eligibility sits with the partners, not the entity — can forfeit withholding tax reductions available to Polish resident companies.

- Selecting a Sp. z o.o. or S.A. when a foundation structure would serve asset-holding objectives locks shareholders into annual general meeting obligations, mandatory financial reporting, and dividend distribution rules that do not apply to non-commercial entities.

- Choosing an entity required to file audited financial statements when your operation is a single-person consultancy adds recurring statutory audit costs without operational justification.

Key Factors to Consider

- Business Activity: Trading actively, holding assets passively, or operating in a regulated sector each points to a structurally different entity under the Code of Commercial Companies (*Kodeks spółek handlowych*).

- Ownership and Management: Single-owner operations suit a sole proprietorship or single-member Sp. z o.o., while multi-party ventures may require a board structure or a defined profit-sharing mechanism.

- Tax Objectives: Whether your business qualifies for the Estonian CIT regime, requires treaty access, or benefits from small taxpayer status shapes which entity fits your fiscal position.

- Substance Capacity: If you cannot maintain a physical presence, payroll, or local decision-making, structures with lower substance thresholds — such as a branch of an EU entity — may be more appropriate.

- Privacy Requirements: Shareholder and director details for capital companies are publicly visible in the KRS; nominee arrangements are permissible but add compliance layers.

- Exit Strategy: Conversion between entity types, redomiciliation, and voluntary winding-up procedures vary in complexity; a P.S.A., for example, was designed with startup exit scenarios in mind.

Compliance Services for Companies in Poland

Ongoing compliance support for Polish entities, including KRS filings, financial reporting obligations, and statutory deadline management.

Conclusion

Incorporating a company in Poland requires matching the legal structure to the intended use, ownership profile, and liability expectations of the business. The Sp. z o.o. remains the most widely registered entity in the country, favored by small and mid-sized businesses for its manageable capital requirements and limited liability. The S.A. suits larger enterprises with complex shareholder structures or public listing ambitions, while the P.S.A. was designed specifically for startups and ventures where equity flexibility matters. Partnerships serve operators who accept personal liability in exchange for structural simplicity, and foreign businesses entering without a local legal entity typically do so through a branch or representative office.

Poland's regulatory framework continues to evolve, with ongoing digitization of the KRS registration process and active participation in the OECD's international tax reform agenda signaling a trajectory toward greater transparency and administrative modernization. Expanship's team works directly within this framework to support each stage of the process.

How Expanship Can Assist You

Our corporate services for Poland company setup cover the full formation process — from selecting between a Sp. z o.o., S.A., or P.S.A. to filing registration documents with the Krajowy Rejestr Sądowy (KRS). Expanship Poland incorporation services are structured around your specific structure choice, not a generic checklist.

From document preparation to post-registration compliance, here is what your engagement with us includes:

- Document preparation, notarization, and legalization

- Registered office and registered agent provision

- KRS filing and liaison with the Central Registration and Information on Business (CEIDG) where applicable

- Tax identification (NIP) and statistical number (REGON) registration support

- Post-incorporation compliance management, including annual reporting obligations

- Banking introduction assistance for corporate account opening in Poland

Reach out to discuss your structure and timeline with our Poland team at Expanship Poland.

Frequently Asked Questions (FAQ)

The Spółka z Ograniczoną Odpowiedzialnością (Sp. z o.o.) is the most frequently formed entity, primarily because it combines limited liability with a relatively low minimum share capital of PLN 5,000. Its straightforward governance structure and compatibility with both domestic and cross-border operations make it the default choice for most commercial purposes.

A Sp. z o.o. is governed by Articles 151–300 of the Commercial Companies Code (Kodeks Spółek Handlowych) and suits closely held businesses, while an S.A. is designed for larger entities that may seek public capital through share issuance. The S.A. carries heavier disclosure and supervisory board requirements, making annual compliance more demanding than for a Sp. z o.o.

The Sp. z o.o. and S.A. both require disclosure of beneficial owners in the Central Register of Beneficial Owners (CRBR), so neither offers full anonymity under current Polish law. Nominee arrangements are legally permissible but do not exempt the ultimate beneficial owner from CRBR registration obligations.

A Sp. z o.o. and a Prosta Spółka Akcyjna (P.S.A.) can each be formed by a single founder. Partnerships — including the Spółka Jawna and Spółka Komandytowa — require at least two partners by definition, and a sole Sp. z o.o. cannot itself be the sole shareholder of another Sp. z o.o.

Non-residents and foreign nationals may form a Sp. z o.o., S.A., or P.S.A. without restriction. Access to partnership structures — such as the Spółka Komandytowa — may depend on the applicant's country of origin and applicable bilateral agreements, though EU/EEA nationals generally face no additional barriers.

The Commercial Companies Code permits transformation (przekształcenie) between most registered entity types, including conversion from a Sp. z o.o. to an S.A. or P.S.A. The process requires shareholder resolutions, preparation of a transformation plan, and registration with the National Court Register (KRS); full legal continuity is preserved throughout.

Capital companies — the Sp. z o.o., S.A., and P.S.A. — hold full legal personality from the moment of KRS registration. General partnerships (Spółka Jawna) and limited partnerships (Spółka Komandytowa) have legal capacity under Article 8 of the Commercial Companies Code but are not considered legal persons in the strict civil-law sense.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.