Key Takeaways

- The Securities and Exchange Commission (SEC) governs all corporations and partnerships in the Philippines under the Revised Corporation Code (Republic Act No. 11232), while sole proprietorships fall under a separate registration regime administered by the Department of Trade and Industry (DTI).

- Stock Corporations represent the largest share of SEC registrations, making them the most commonly used business structure for both local and foreign investors in the Philippines.

- Foreign firms must choose between a Branch Office, Representative Office, RHQ, or ROHQ based primarily on whether the entity is permitted to generate income within the Philippines.

- Introduced under the Revised Corporation Code, the One Person Corporation (OPC) allows a sole founder to establish a legally separate entity without requiring a second shareholder.

Introduction to Entity Types in Philippines

Located in Southeast Asia, the Philippines is an archipelago nation bordered by Taiwan to the north, Malaysia to the south, and Indonesia to the southwest. It is an independent republic governed under a presidential system, and its commercial environment is shaped by a civil law tradition with significant influence from American corporate law.

Company registration falls under the authority of the Securities and Exchange Commission (SEC), the primary regulatory body overseeing the formation and ongoing compliance of business entities in the country. Sole proprietorships are separately registered with the Department of Trade and Industry (DTI). The tax system is residential and source-based, administered by the Bureau of Internal Revenue (BIR), with corporate income generally taxed on income derived from Philippine sources.

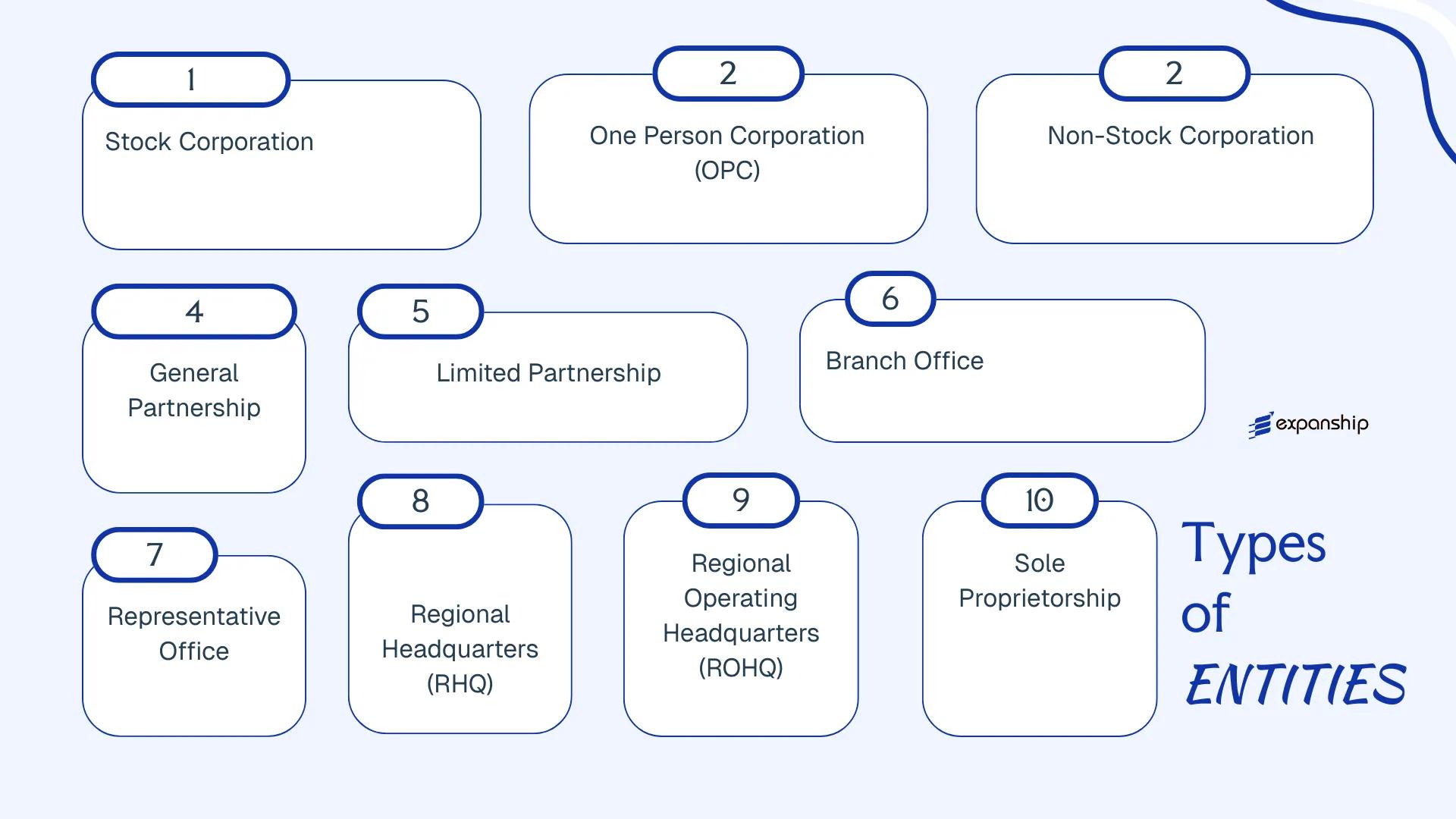

The types of business entities in Philippines available to local and foreign investors include:

- Stock Corporation

- One Person Corporation (OPC)

- Non-Stock Corporation

- General Partnership

- Limited Partnership

- Branch Office

- Representative Office

- Regional Headquarters (RHQ)

- Regional Operating Headquarters (ROHQ)

- Sole Proprietorship

Each structure carries distinct ownership requirements, liability frameworks, and regulatory obligations — this article examines each one in detail.

An Overview of Business Structures in Philippines

Several business structures are available in the Philippines, governed primarily by the Revised Corporation Code (Republic Act No. 11232), which took effect in 2019, alongside the Civil Code of the Philippines for partnership arrangements. Sole proprietorships fall under the jurisdiction of the Department of Trade and Industry, while foreign vehicle registrations are processed through the Securities and Exchange Commission. Each structure carries distinct liability exposure, ownership requirements, and tax treatment.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Stock Corporation | Separate legal entity | Limited to shares | Taxed | Yes | 2 incorporators | SEC | RA 11232 |

| One Person Corporation | Separate legal entity | Limited | Taxed | Yes | 1 incorporator | SEC | RA 11232 |

| Non-Stock Corporation | Separate legal entity | Limited | Exempt (conditions apply) | Restricted | 5 trustees | SEC | RA 11232 |

| General Partnership | Not separate | Unlimited | Taxed | Yes | 2 partners | SEC | Civil Code |

| Limited Partnership | Partial separation | Mixed | Taxed | Yes | 2 partners (1 general) | SEC | Civil Code |

| Branch Office | Extension of parent | Parent liable | Taxed | Yes | N/A | SEC | RA 7042 |

| Representative Office | Extension of parent | Parent liable | Not taxed | No | N/A | SEC | RA 7042 |

| Regional HQ (RHQ) | Extension of parent | Parent liable | Exempt | No | N/A | SEC | RA 8756 |

| Regional Operating HQ (ROHQ) | Extension of parent | Parent liable | Taxed (preferential) | Limited | N/A | SEC | RA 8756 |

| Sole Proprietorship | No separation | Unlimited | Taxed | Yes | 1 owner | DTI | Business Name Law |

Each of these structures is examined in full in the sections below.

Stock Corporation

A stock corporation is the most widely used business structure for commercial activity in the Philippines, and stock corporation registration Philippines requires filing with the Securities and Exchange Commission (SEC) under the Revised Corporation Code (Republic Act No. 11232), which took effect in 2019. The entity holds a separate legal personality distinct from its shareholders, meaning personal assets are generally shielded from corporate liabilities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Stock Corporation | Governed by RA 11232; separate legal personality |

| Members | Shareholders (minimum 2, maximum 15 directors on the board) | Stockholders may be natural or juridical persons; no minimum number of stockholders under RA 11232 |

| Local Presence | Registered office address in the Philippines required | No mandatory resident agent, but a registered address must be on file with the SEC |

| Capital | No minimum authorized capital stock (general rule); specific industries may impose minimums | Stated in Philippine Peso (PHP); paid-up capital must be at least 25% of authorized capital, with at least 25% of subscribed capital paid up |

| Foreign Ownership | Up to 100% in most sectors; restricted or capped in sectors under the Foreign Investment Negative List | Verify current restrictions via the Foreign Investments Act |

| Privacy | Beneficial ownership disclosure required; SEC filings are publicly accessible | General Information Sheet (GIS) filed annually is a public document |

Focus Points

- Taxation: Subject to a 25% corporate income tax (20% for domestic corporations with net taxable income not exceeding PHP 5 million and total assets not exceeding PHP 100 million); 12% VAT applies to taxable transactions; dividends paid to non-resident foreign corporations are subject to a 15% or 25% withholding tax depending on treaty status; documentary stamp tax applies to share issuances. See BIR tax rates for current figures.

- Annual Compliance: Annual General Information Sheet and audited financial statements must be filed with the SEC; BIR registration renewal and local government business permit renewal required each year.

- Economic Substance: No formal economic substance regime equivalent to offshore jurisdictions, but tax residency and effective management tests apply for treaty access purposes.

- Treaty Access: As a domestic corporation, eligible for benefits under the Philippines' tax treaty network, subject to anti-treaty shopping provisions and BIR certification requirements.

- Conversion: A stock corporation may convert to a One Person Corporation (OPC) if shareholding reduces to one, or to a non-stock corporation if it ceases distributing dividends, subject to SEC approval.

Sub-Types

Publicly Listed Corporation

A stock corporation whose shares are listed and traded on the Philippine Stock Exchange (PSE), subject to additional regulation by the SEC and PSE rules, including disclosure obligations under the Securities Regulation Code (RA 8799). This structure is used by large enterprises seeking access to public capital markets.

Closely Held Corporation

A stock corporation where shares are held by a limited number of stockholders and are not publicly traded. Typically used for family-owned businesses or joint ventures where share transferability is restricted through a shareholders' agreement or the articles of incorporation.

When to Use This Structure

A stock corporation suits trading companies, operating subsidiaries, joint ventures, and businesses requiring external investment, though it carries relatively higher annual compliance obligations compared to simpler structures.

Foreign investors and domestic entrepreneurs establishing a commercial operating business in the Philippines who anticipate multiple shareholders, external funding rounds, or eventual listing.

Company Incorporation in the Philippines

Incorporate a stock corporation in the Philippines with SEC registration support, document preparation, and ongoing compliance management.

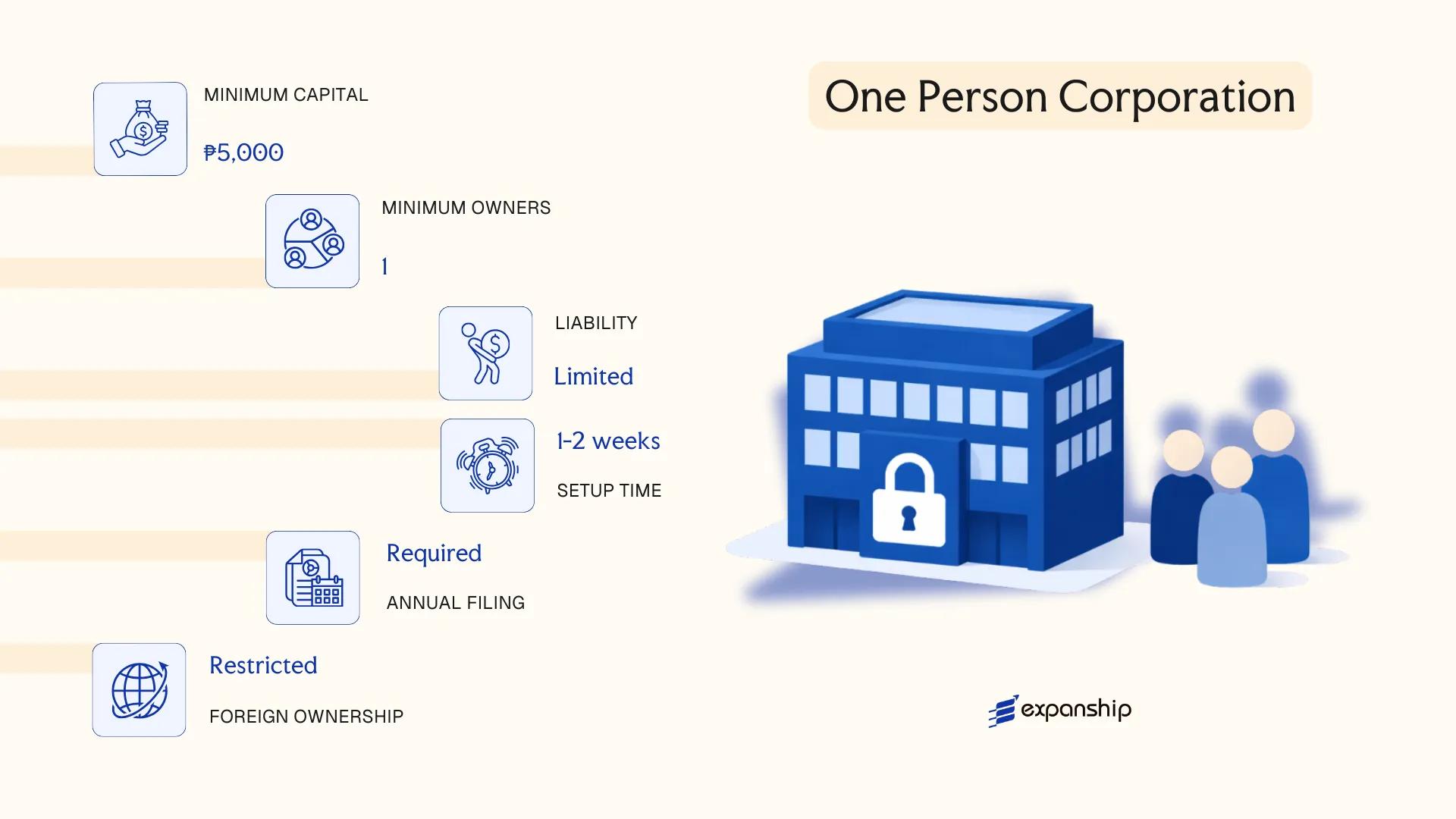

One Person Corporation (OPC)

Introduced under the Revised Corporation Code of the Philippines (Republic Act No. 11232), which took effect in February 2019, the One Person Corporation Philippines OPC is a structure that allows a single natural person, trust, or estate to form a corporation. It carries full juridical personality, meaning the entity is legally distinct from its owner, and the sole shareholder's liability is limited to their capital contribution.

Prior to RA 11232, a corporation required at least five incorporators. The OPC removed that threshold entirely, making it the first corporate form in the country designed for individual entrepreneurs who require limited liability without partners or co-incorporators.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Stock Corporation (single-shareholder) | Governed by RA 11232, Title XIII |

| Members | Sole Shareholder, President, Treasurer, Corporate Secretary | Shareholder must be a natural person, trust, or estate; officers may overlap |

| Minimum Members | 1 shareholder | Foreign nationals permitted subject to Foreign Investment Act restrictions |

| Local Presence | Registered office address required | No requirement for a resident agent, but a Corporate Secretary must be a Philippine resident |

| Capital | No minimum paid-up capital prescribed under RA 11232 | Sector-specific minimums may apply (e.g., retail trade, banking) |

| Privacy | Articles of Incorporation filed with SEC are public | Beneficial ownership disclosures required under AMLA regulations |

Focus Points

- Taxation: Subject to the standard 25% Corporate Income Tax (20% for qualified small corporations), 12% VAT on applicable transactions, creditable withholding taxes, and documentary stamp tax on share issuances and certain instruments.

- Annual Compliance: Must file audited financial statements and General Information Sheet with the Securities and Exchange Commission (SEC) annually; barangay, municipal, and BIR renewals also required.

- Conversion: An OPC may convert to an ordinary stock corporation by filing with the SEC; conversion triggers re-registration and updated Articles of Incorporation.

- Restrictions: Banks, quasi-banks, pre-need companies, trust companies, and certain other regulated entities are explicitly prohibited from registering as an OPC under RA 11232.

- Treaty Access: As a domestic corporation, an OPC can access Philippine tax treaty benefits, subject to beneficial ownership and substance requirements of the relevant treaty.

Recommendations

An OPC suits individual entrepreneurs, freelancers, and holding structures where a single owner requires corporate liability protection without the administrative complexity of a multi-shareholder corporation. The primary advantage is consolidated control with limited liability; the principal limitation is that it cannot be used for industries where a sole-ownership corporate structure is statutorily prohibited.

An OPC is most appropriate for solo founders or individual investors who need a legally separate entity with limited liability but do not intend to bring on co-shareholders in the near term.

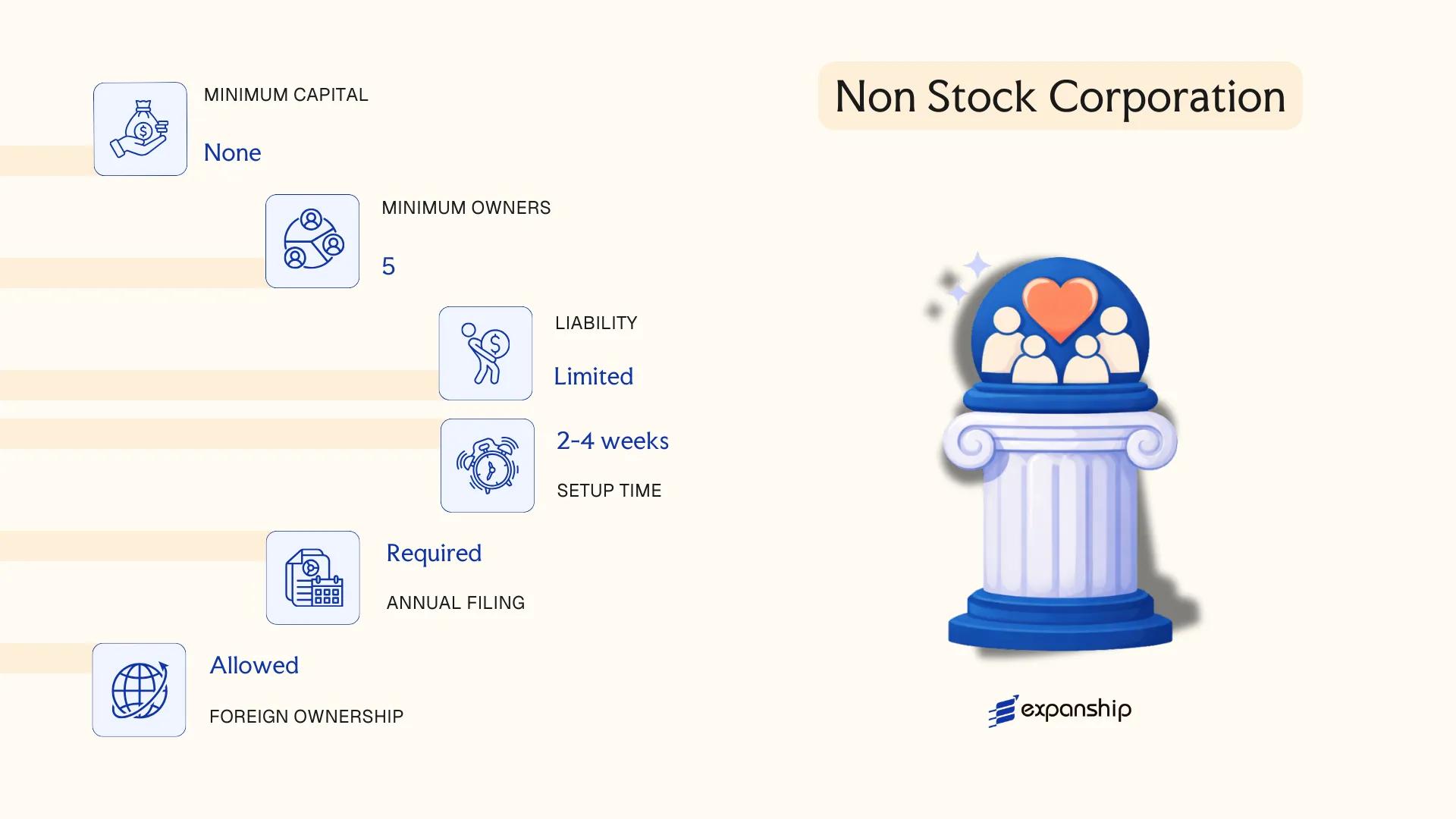

Non-Stock Corporation

Governed by the Revised Corporation Code of the Philippines (Republic Act No. 11232, enacted in 2019), a non-stock corporation is formed for purposes other than profit distribution to its members. It holds a separate legal personality distinct from its members, meaning it can own property, enter contracts, and sue or be sued in its own name.

Proceeds generated by this type of entity must be used exclusively to further its stated purpose — whether charitable, educational, cultural, religious, or civic. Members do not receive dividends or any share of net income. Registration and ongoing compliance fall under the Securities and Exchange Commission (SEC).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Non-Stock, Non-Profit Corporation | Separate legal personality; no share capital issued |

| Members | Minimum 5 members; no statutory maximum | Members vote on corporate matters; no shareholders |

| Directors / Trustees | Minimum 5 trustees; must be members | At least 5 trustees required at incorporation |

| Local Presence | Registered office address in the Philippines required | Must be maintained at all times |

| Capital | No minimum capital requirement | Contributions used solely for stated purpose |

| Privacy | Member information disclosed to SEC | Beneficial ownership records maintained internally |

Focus Points

- Taxation: Exempt from corporate income tax on income directly related to its exempt purpose under the National Internal Revenue Code (NIRC); unrelated income is taxable at standard rates; VAT exemptions may apply depending on activities.

- Annual Compliance: Annual financial statements and general information sheets must be filed with the SEC; BIR registration and annual returns are required regardless of tax-exempt status.

- Tax Exemption Ruling: A separate application with the Bureau of Internal Revenue (BIR) is required to obtain a formal tax-exempt ruling; SEC registration alone does not confer tax exemption.

- Conversion: A non-stock corporation cannot convert into a stock corporation under the Revised Corporation Code.

- Foreign Participation: Foreign nationals may serve as trustees, subject to constitutional restrictions on certain activities and industries.

Closing

Non-stock corporations are used primarily by foundations, associations, NGOs, educational institutions, and religious organizations operating within a defined non-commercial mandate. The tax exemption on related income is a meaningful structural benefit, though obtaining and maintaining that exemption requires active engagement with both the SEC and BIR.

This structure suits foundations, civic organizations, and non-profit entities whose activities align with an exempt purpose recognized under Philippine tax law.

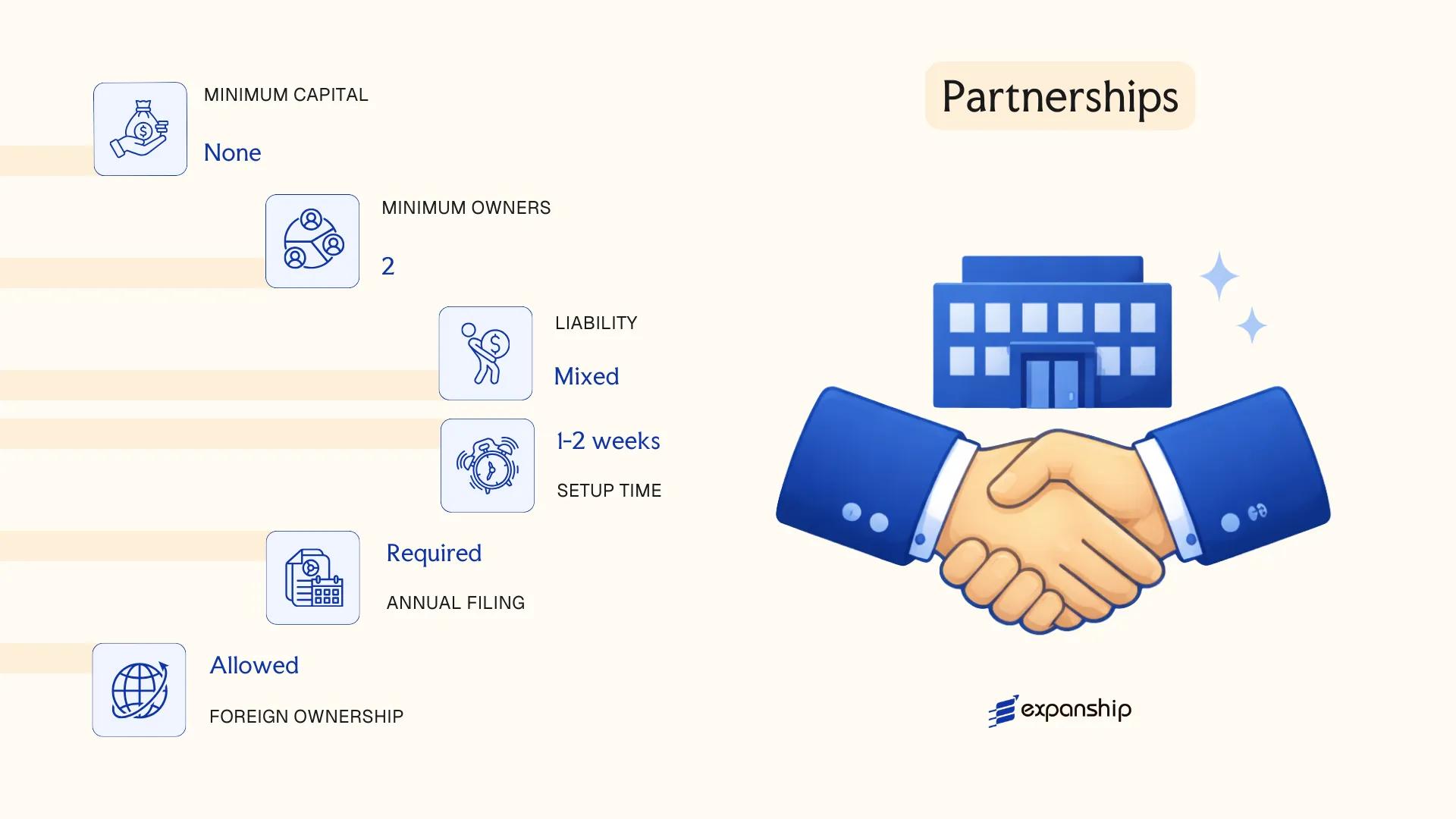

Partnerships [General Partnership, Limited Partnership]

Under the Civil Code of the Philippines (Republic Act No. 386), both general and limited partnership Philippines structures are treated as juridical persons — meaning each holds a separate legal personality distinct from its partners. A limited partnership must file a certificate of limited partnership with the Securities and Exchange Commission (SEC), whereas a general partnership is formed by contract and similarly requires SEC registration once capital reaches a threshold requiring formal documentation.

Key Characteristics

| Requirement | General Partnership | Limited Partnership |

|---|---|---|

| Legal Form | Juridical person; governed by the Civil Code | Juridical person; requires SEC-filed certificate |

| Members | At least 2 general partners; no maximum | At least 1 general partner + 1 limited partner; no maximum |

| Liability | All partners: unlimited, joint and several | General partner: unlimited; limited partner: capped at contribution |

| Minimum Capital | No statutory minimum; PHP 3,000+ triggers SEC registration | No statutory minimum; same SEC registration threshold applies |

| Local Presence | Registered office address in the Philippines required | Registered office address in the Philippines required |

| Privacy | Partner names disclosed in SEC filings; not publicly searchable online by default | Certificate of limited partnership is a public SEC record |

Focus Points

- Taxation: Partnerships (except general professional partnerships) are taxed at the 25% corporate income tax rate; partners pay an additional 10% final tax on their share of distributable income; VAT applies if annual revenue exceeds PHP 3 million.

- General Professional Partnerships: Formed exclusively by licensed professionals, these are exempt from corporate income tax — partners instead declare their respective shares as individual income.

- Annual Compliance: Partnerships must file audited financial statements and General Information Sheets with the SEC annually; BIR registration and annual renewal are also mandatory.

- Conversion: A partnership may be converted to a corporation, subject to SEC approval and compliance with the Revised Corporation Code (Republic Act No. 11232).

- Foreign Participation: Foreign nationals may form or join a partnership, subject to foreign equity restrictions under the Foreign Investments Act and the Foreign Investment Negative List.

Sub-Types

General Partnership

All partners bear unlimited, joint and several liability for the firm's obligations. This structure is most commonly used by small professional or family-run businesses where all principals are actively involved in management.

Limited Partnership

One or more limited partners contribute capital but do not participate in management, with liability confined to their contributed amount. The general partner retains full management authority and unlimited liability, making this arrangement suitable for investment vehicles or projects where passive investors are involved.

Closing

Partnerships suit professional services groups, joint ventures, and investment arrangements where a pass-through or hybrid liability structure is preferred over full corporate formation. The key drawback is that at least one general partner always carries unlimited personal liability.

Philippine partnerships work best for licensed professionals forming a practice group, or for two or more parties structuring a project-specific venture where full incorporation is not warranted.

Foreign Business Vehicles [Branch Office, Representative Office, Regional Headquarters (RHQ), Regional Operating Headquarters (ROHQ)]

Foreign corporations seeking a presence in the Philippines without incorporating a local entity have four recognised structures under the Revised Corporation Code (Republic Act No. 11232) and the Foreign Investments Act (Republic Act No. 7042), administered by the Securities and Exchange Commission (SEC). Each structure carries distinct operational permissions and legal obligations. None of these vehicles constitutes a separate legal entity from the foreign parent; they are extensions of the parent corporation.

Choosing among these foreign business vehicles in the Philippines depends largely on whether your firm intends to derive income locally. Income-generating operations require either a Branch Office or a Regional Operating Headquarters, while non-income structures such as Representative Offices and Regional Headquarters serve liaison or supervisory functions only.

Key Characteristics

| Requirement | Branch Office | Representative Office | RHQ | ROHQ |

|---|---|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality | Extension of foreign parent | Extension of foreign parent |

| Permitted Activities | Income-generating; same business as parent | Non-income; liaison only | Non-income; supervisory/coordination only | Income-generating services to affiliates only |

| Assigned Capital | USD 200,000 minimum inward remittance | USD 30,000 minimum annual remittance | USD 50,000 minimum annual remittance | USD 200,000 minimum annual remittance |

| Local Office | Required; must maintain a registered Philippine address | Required | Required | Required |

| Resident Agent | Must appoint a resident agent for service of process | Required | Required | Required |

| SEC Registration | Required; Certificate of Authority to do Business | Required | Required; PEZA endorsement may apply | Required; endorsed by BOI or PEZA |

Focus Points

- Taxation: Branch Offices are subject to 25% corporate income tax on Philippine-sourced income plus a 15% branch profit remittance tax on profits sent abroad; ROHQs are taxed at a preferential 10% rate on taxable income; Representative Offices and RHQs have no Philippine income tax exposure as they derive no local income; VAT and withholding tax obligations apply where income-generating activities exist.

- Annual Compliance: All four vehicles must file annual reports with the SEC; Branch Offices submit audited financial statements covering Philippine operations.

- Restrictions: Representative Offices and RHQs cannot earn revenue from Philippine sources under any circumstances; ROHQs may only bill affiliated entities, not third-party Philippine clients.

- Foreign Equity: All four structures are 100% foreign-owned by definition, but remain subject to the Foreign Investment Negative List for restricted activities.

- Conversion: A Branch Office can apply to convert into a domestic subsidiary corporation, though this requires a separate incorporation process with the SEC.

Sub-Types

Branch Office

A Branch Office may conduct the same revenue-generating activities as its parent and is the only foreign vehicle permitted to serve Philippine-domiciled third-party clients directly.

Representative Office

Limited strictly to market research, information dissemination, and liaison functions, this structure cannot generate any income and is funded entirely through remittances from the parent.

Regional Headquarters (RHQ)

An RHQ coordinates and supervises the parent's subsidiaries and affiliates across the Asia-Pacific region but is prohibited from participating in any commercial transactions or earning income locally.

Regional Operating Headquarters (ROHQ)

An ROHQ may render qualifying services — including general administration, business planning, and logistics — exclusively to its regional affiliates, making it suitable for shared service centre arrangements.

Closing

Foreign business vehicles suit firms that need a Philippine operational footprint without committing to full local incorporation; the Branch Office offers direct market access, while the ROHQ structure suits regional service delivery. A firm material limitation across all four structures is the absence of separate legal personality, meaning the parent remains directly liable for obligations incurred locally.

These structures are best suited for established foreign corporations that want to test or serve the Philippine market, manage regional operations, or run intra-group service functions without forming a locally incorporated entity.

Sole Proprietorship

Sole proprietorship registration Philippines is governed by Republic Act No. 3883, also known as the Business Name Law, and administered by the Department of Trade and Industry (DTI). Unlike a corporation, a sole proprietorship has no separate legal personality — the owner and the business are legally the same entity, meaning personal assets are fully exposed to business liabilities.

Registration with the DTI is required before commencing operations. The DTI business name registration is valid for five years and must be renewed prior to expiry.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality from the owner |

| Members | Single proprietor | No minimum capital prescribed under DTI registration |

| Local Presence | DTI-registered business name; local address required | Must maintain a Philippine address for official correspondence |

| Capital | No statutory minimum | Owner bears full financial responsibility |

| Privacy | Owner's name linked to business name on public DTI records | Limited privacy relative to corporate structures |

Focus Points

- Taxation: Subject to personal income tax rates (0%–35%) on net business income; VAT registration required if annual gross sales exceed PHP 3,000,000; also subject to percentage tax and applicable withholding tax obligations.

- Annual Compliance: DTI business name renewal every five years; annual income tax return filing with the Bureau of Internal Revenue (BIR); barangay and local government unit permits require annual renewal.

- Treaty Access: No access to tax treaty benefits, as treaties apply to corporations and qualifying entities, not unincorporated sole proprietors.

- Conversion: Can be converted to a corporation or partnership, though this requires a new registration process rather than a structural amendment.

- Restrictions: Foreign nationals are generally prohibited from operating a sole proprietorship, as this structure is reserved for Filipino citizens under the Foreign Investments Act.

Closing

A sole proprietorship suits small-scale, locally operated trading or service businesses where simplicity and low administrative cost are priorities; its primary drawback is unlimited personal liability, with no legal separation between business obligations and the owner's personal estate.

Filipino citizens running small, single-owner businesses who require minimal compliance overhead and do not require foreign equity participation.

How to Choose the Right Entity Type in Philippines

Selecting the correct structure at the outset shapes your tax position, liability exposure, and operational capacity for the life of the business. Getting this decision wrong produces concrete, often costly outcomes.

Why Your Entity Choice Matters

- A branch office that conducts activities beyond its approved scope violates SEC registration conditions and may face suspension or revocation of its license to do business.

- Registering as a non-stock corporation when you intend to generate profit disqualifies you from distributing earnings to members, locking in a structure incompatible with your commercial model.

- Choosing a sole proprietorship — registered with the Department of Trade and Industry — provides no separate legal personality, meaning personal assets remain exposed to business liabilities without limit.

- Forming a One Person Corporation when you later need to bring in equity partners requires structural conversion, adding regulatory steps and SEC filing costs that a stock corporation would have avoided from the start.

Key Factors to Consider

- Business Activity: Regulated sectors such as banking, insurance, and securities require specific entity types as prescribed by the Bangko Sentral ng Pilipinas or the Insurance Commission, independent of your preference.

- Foreign Equity: Certain activities under the Foreign Investment Negative List restrict foreign ownership percentages, making entity selection inseparable from ownership planning.

- Ownership and Management: A single foreign founder may prefer an OPC, but multi-party ventures typically require a stock corporation with a formal board structure under the Revised Corporation Code (Republic Act No. 11232).

- Tax Objectives: ROHQs receive preferential tax treatment under the Tax Code, while standard domestic corporations are subject to the regular corporate income tax rate.

- Operational Scope: If your firm will not derive income from Philippine sources, a representative office avoids income tax exposure but prohibits revenue-generating activity entirely.

- Exit Strategy: Not all entity types permit redomiciliation or conversion — confirm in advance whether the structure allows dissolution, merger, or conversion without triggering disproportionate tax consequences.

Corporate Compliance Services in the Philippines

Maintain good standing with the SEC, BIR, and other Philippine regulatory bodies through structured compliance support.

Conclusion

Selecting the right structure is the first substantive decision in any Philippines company formation guide summary. Corporations registered under the Revised Corporation Code (Republic Act No. 11232) remain the most commonly formed entities, with the Stock Corporation accounting for the largest share of registrations with the Securities and Exchange Commission. The One Person Corporation suits solo founders who need separate legal personality without a co-shareholder requirement. Non-Stock Corporations serve civic, educational, or charitable purposes. Partnerships offer a lighter registration path, while sole proprietorships fall under the Department of Trade and Industry rather than the SEC.

Foreign firms choosing between a Branch, Representative Office, RHQ, or ROHQ do so primarily on whether income-generating activity is permitted. Incorporating in Philippines has grown more procedurally accessible following SEC digitization efforts, and the country continues to expand its tax treaty network. Professional guidance on structure selection reduces the risk of misclassification and subsequent compliance exposure.

How Expanship Can Assist You

Expanship provides corporate services Philippines business setup clients need across the full incorporation cycle — from entity selection to post-registration compliance. This blog has covered structures registered with the Securities and Exchange Commission (SEC), from Stock Corporations and One Person Corporations to Branch Offices and ROHQs, and our team works directly within those frameworks.

From a single point of contact, your business can access:

- Document preparation, notarization, and consular legalization

- Registered agent and local registered office provision

- SEC filing, DTI registration, and government agency liaison

- Post-incorporation compliance management, including annual reporting

- Corporate secretary and resident agent services

- Banking introduction assistance for local account opening

Each engagement is scoped to your entity type and activity, not a generic checklist applied across the board.

Reach out to Expanship Philippines to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Stock Corporation is the most frequently registered business structure, primarily because it allows for multiple shareholders, transferable shares, and a clear governance framework suited to businesses planning external investment or growth. Its flexibility under the Revised Corporation Code makes it the default choice for both domestic entrepreneurs and foreign joint venture participants.

A Branch Office is an extension of its foreign parent and is not a separate legal entity under Philippine law, meaning the parent bears full liability for its Philippine operations. A Stock Corporation is an independent legal person, subject to the same tax rates on Philippine-sourced income but with greater autonomy in governance and profit retention. Compliance obligations differ as well: a Branch requires Securities and Exchange Commission (SEC) registration and must remit a branch profits remittance tax of 15% on profits sent abroad, whereas a corporation's dividends to foreign shareholders are taxed at 25% unless a tax treaty applies.

Among registered structures, the One Person Corporation (OPC) limits public disclosure to the sole incorporator, with no requirement to name additional shareholders. Beneficial ownership information is filed with the SEC but is not freely accessible to the general public. Nominee arrangements are not a recognized feature of OPCs under the Revised Corporation Code.

A sole individual can form an OPC or a Sole Proprietorship, both designed for single-person ownership. Partnerships, whether General or Limited, require at least two partners under the Civil Code of the Philippines. A Stock Corporation requires a minimum of two incorporators, while a Non-Stock Corporation requires at least five.

Foreign individuals and entities can register a Stock Corporation, Branch Office, Representative Office, Regional Headquarters (RHQ), or Regional Operating Headquarters (ROHQ) with the SEC. Foreign equity limits apply in sectors covered by the Foreign Investment Negative List, which restricts or caps ownership in industries such as mass media, utilities, and certain retail categories. An OPC is currently restricted to Filipino citizens under SEC regulations.

The Revised Corporation Code permits a Stock Corporation to convert to an OPC and vice versa, subject to SEC approval and compliance with specific procedural requirements. A Sole Proprietorship converting to a corporation requires a new SEC registration rather than a direct conversion. Partnerships converting to corporations follow a separate process involving dissolution of the partnership and fresh incorporation.

Stock Corporations, OPCs, and Non-Stock Corporations are juridical persons distinct from their owners under Philippine law. A General Partnership also has legal personality under the Civil Code, though partners remain personally liable for partnership obligations. Sole Proprietorships and Branch Offices do not possess separate legal personality; the individual owner and the foreign parent, respectively, remain directly liable.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.