Key Takeaways

- Peru's most commonly registered business structure is the Sociedad Anónima Cerrada (SAC), which offers limited liability without the public disclosure obligations required of the Sociedad Anónima Abierta (SAA).

- All legal entities in Peru must register with SUNARP through the Registro de Personas Jurídicas, while tax compliance is administered separately by SUNAT under the framework established by Decreto Legislativo N° 774.

- The Empresa Individual de Responsabilidad Limitada (EIRL) is the only structure available to sole operators who require legal separation between personal and business liability.

- Foreign companies entering Peru can establish either a Branch Office or a Representative Office without incorporating a new local entity under the Ley General de Sociedades.

Introduction to Entity Types in Peru

Peru is a sovereign republic on the western coast of South America, bordered by Ecuador, Colombia, Brazil, Bolivia, and Chile. Business registration falls under the authority of the Superintendencia Nacional de los Registros Públicos (SUNARP), which maintains the Registro de Personas Jurídicas — the official registry for legal entities. Tax obligations are administered separately by the Superintendencia Nacional de Aduanas y de Administración Tributaria (SUNAT), which enforces a territorial-based income tax system under Decreto Legislativo N° 774 and its successor legislation.

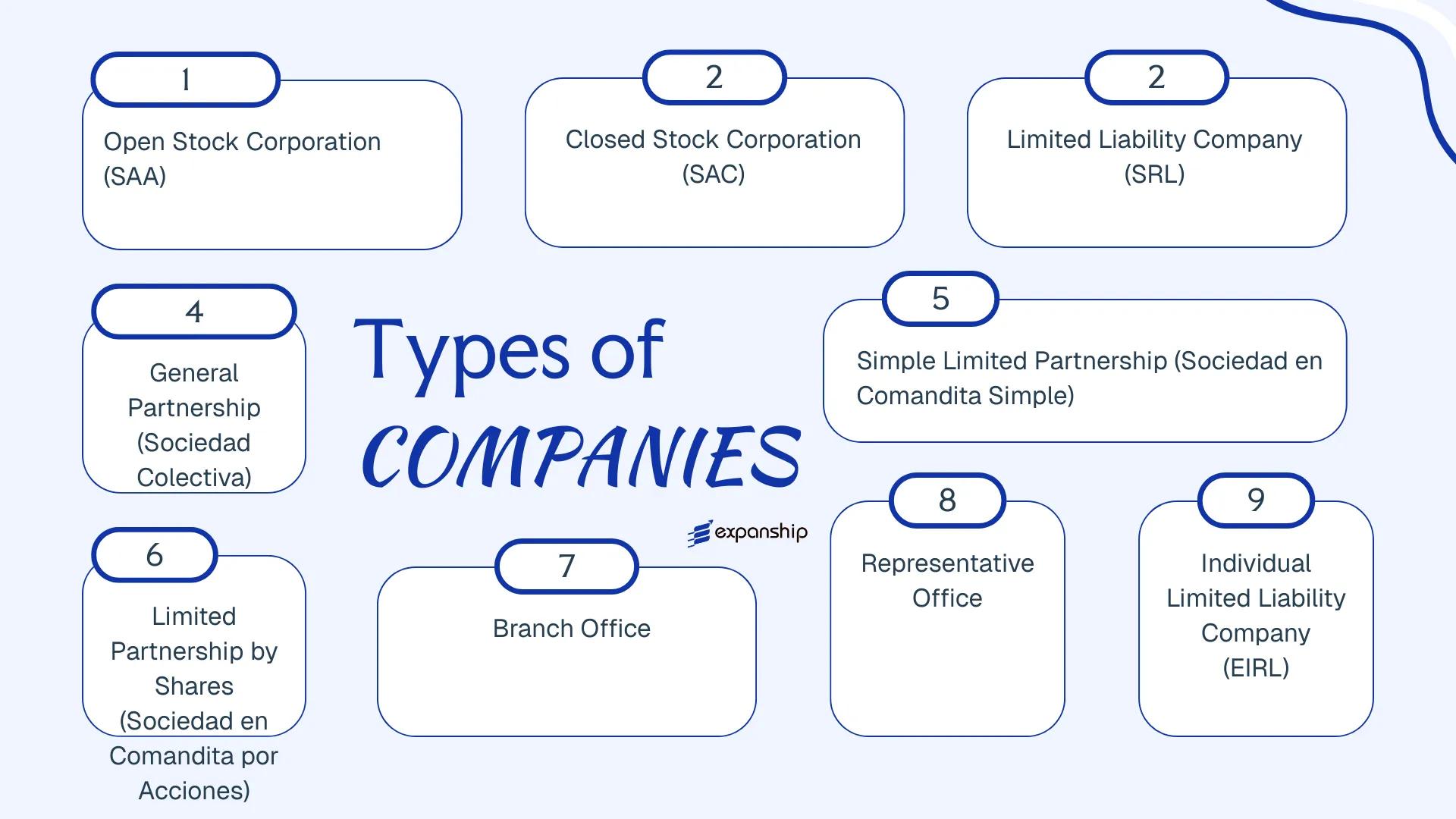

The types of business entities in Peru span both locally incorporated structures and foreign establishment options. Available forms include the Sociedad Anónima Abierta (SAA), Sociedad Anónima Cerrada (SAC), Sociedad de Responsabilidad Limitada (SRL), Sociedad Colectiva, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones, Branch Office, Representative Office, and the Empresa Individual de Responsabilidad Limitada (EIRL).

Each structure carries distinct implications for liability, ownership, governance, and tax treatment. This article examines each form in detail so your business can make an informed decision before committing to a structure.

An Overview of Business Structures in Peru

Governed by the Ley General de Sociedades (General Companies Law, Law No. 26887), Peru recognises several distinct corporate forms, each designed for a different commercial purpose and ownership structure. The law establishes the framework for incorporating, operating, and dissolving business entities, with the Superintendencia Nacional de los Registros Públicos (SUNARP) handling registration and the Superintendencia Nacional de Aduanas y de Administración Tributaria (SUNAT) administering tax obligations. Each structure carries its own liability rules, membership requirements, and governance obligations.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedad Anónima Abierta (SAA) | Public corporation | Limited | Taxable | Permitted | 750+ shareholders | SUNARP / SMV | Law No. 26887 |

| Sociedad Anónima Cerrada (SAC) | Private corporation | Limited | Taxable | Permitted | 2–20 shareholders | SUNARP | Law No. 26887 |

| Sociedad de Responsabilidad Limitada (SRL) | LLC | Limited | Taxable | Permitted | 2–20 partners | SUNARP | Law No. 26887 |

| Sociedad Colectiva | General partnership | Unlimited | Taxable | Permitted | Min. 2 partners | SUNARP | Law No. 26887 |

| Sociedad en Comandita Simple | Limited partnership | Mixed | Taxable | Permitted | Min. 2 partners | SUNARP | Law No. 26887 |

| Sociedad en Comandita por Acciones | Share-based partnership | Mixed | Taxable | Permitted | Min. 2 partners | SUNARP | Law No. 26887 |

| Branch Office | Foreign branch | Parent liable | Taxable | Permitted | Parent company | SUNARP / SUNAT | Law No. 26887 |

| Representative Office | Liaison office | Parent liable | Generally exempt | Not permitted | Parent company | SUNAT | Law No. 26887 |

| Empresa Individual de Responsabilidad Limitada (EIRL) | Sole proprietorship | Limited | Taxable | Permitted | 1 individual | SUNARP | Decree Law No. 21621 |

Each of these structures is examined in full in the sections below.

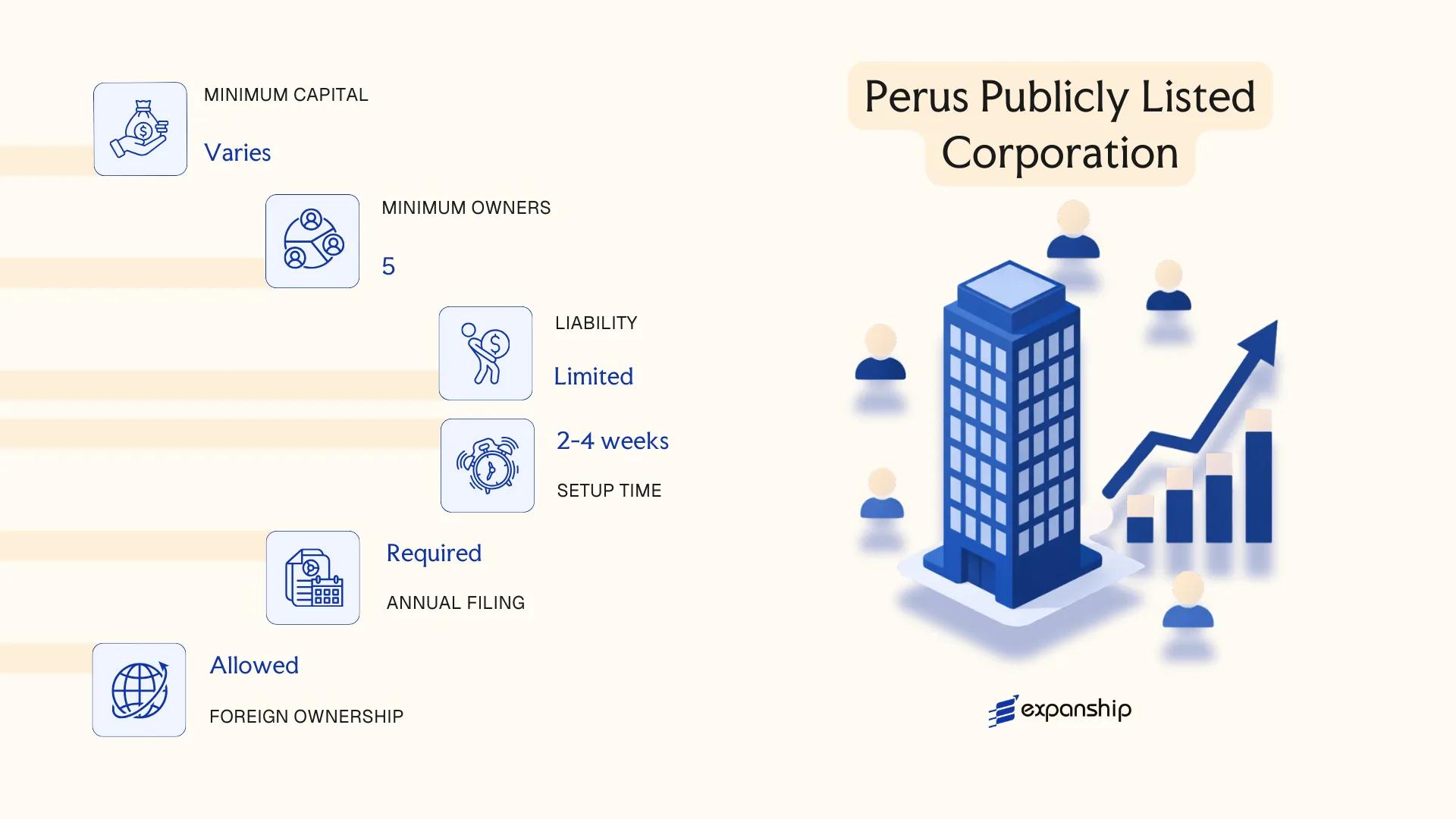

Sociedad Anónima Abierta (SAA) — Peru's Publicly Listed Corporation

The Sociedad Anónima Abierta Peru SAA is governed by the General Corporations Law, Ley General de Sociedades (Law No. 26887, 1997), specifically under Articles 249 to 264. It carries separate legal personality, meaning the entity's obligations are legally distinct from those of its shareholders.

As a publicly listed structure, the SAA is subject to mandatory supervision by the Superintendencia del Mercado de Valores (SMV), Peru's securities regulator. Shares are freely transferable and may be offered to the public, which distinguishes this form from its closed counterpart.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Anónima Abierta | Public corporation under Law No. 26887 |

| Members | Shareholders (accionistas) | Minimum 750 shareholders required by law |

| Liability | Limited to share capital | Shareholders bear no personal liability for corporate debts |

| Local Presence | Registered office in Peru required | Must maintain a domicile registered with SUNARP |

| Share Capital | No statutory minimum; denominated in PEN | Shares must be registered with the SMV |

| Privacy | Low | Shareholder lists and financial statements are publicly disclosed |

Focus Points

- Taxation: Subject to 29.5% corporate income tax; VAT (IGV) applies at 18%; dividends distributed to non-residents attract a 5% withholding tax; no stamp duty on share transfers. Full details at SUNAT.

- Annual Compliance: Mandatory audited financial statements; annual general meeting required; continuous SMV reporting obligations apply.

- Economic Substance: No formal economic substance regime exists, but SMV listing rules require active operational presence and ongoing disclosure.

- Treaty Access: Peru has double taxation agreements with several countries; SAAs may access treaty benefits subject to beneficial ownership conditions.

- Conversion: An SAA must convert to a Sociedad Anónima Cerrada (SAC) if it falls below the 750-shareholder threshold and does not remedy the shortfall within a prescribed period.

Closing

The SAA suits large enterprises seeking public capital markets access or those with broad investor bases; however, the continuous SMV disclosure obligations and the 750-shareholder minimum make it unsuitable for closely held or family-owned businesses.

Large enterprises and institutional ventures seeking access to Peru's public capital markets through SMV-listed share offerings.

Company Incorporation in Peru

Incorporate your business entity in Peru with full compliance support across all entity types.

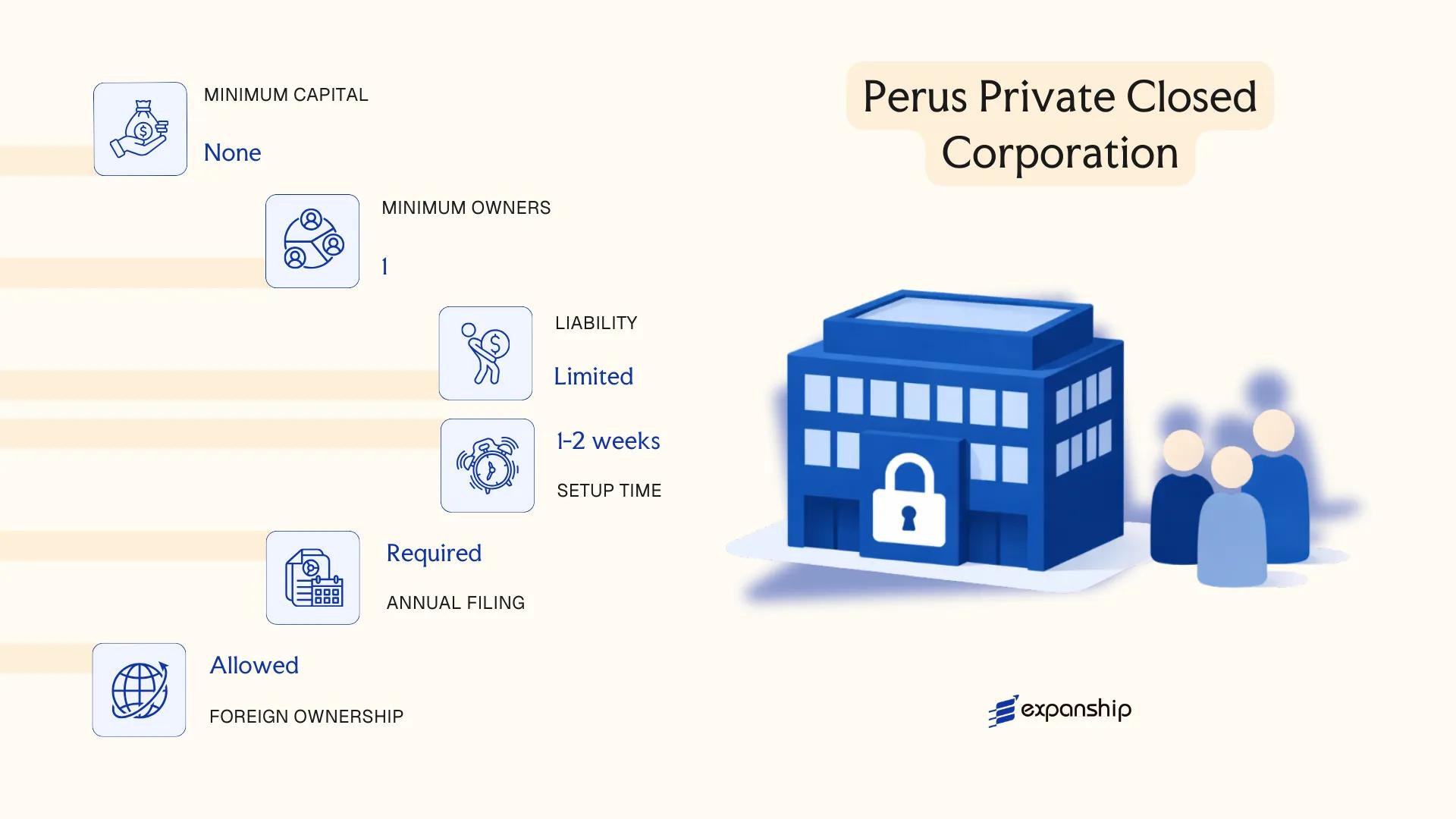

Sociedad Anónima Cerrada (SAC) — Peru's Private Closed Corporation

The Sociedad Anónima Cerrada Peru SAC is governed by the General Corporation Law, Ley General de Sociedades (Law No. 26887), enacted in 1997. It carries a separate legal personality, meaning liabilities rest with the entity rather than its shareholders.

Structurally, the SAC sits between a large public corporation and a small sole proprietorship. Shares are not listed on any stock exchange, and transfers are restricted by law, making this structure suited for closely held private businesses.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Anónima Cerrada | Private share-based company; shares not publicly traded |

| Members | Shareholders: 2 minimum, 20 maximum | Shareholders elect a Board of Directors or appoint a sole manager (Gerente) |

| Local Presence | Registered address in Peru required | No mandatory resident director, but a legal representative (Gerente General) must be designated |

| Share Capital | No statutory minimum; denominated in PEN or USD | Capital divided into shares; contributions can be monetary or in-kind |

| Privacy | Shareholder register held internally | Not publicly searchable; however, company records are filed with SUNARP |

Focus Points

- Taxation: Subject to 29.5% corporate income tax; VAT (IGV) applies at 18%; dividend distributions to non-residents attract 5% withholding tax; no stamp duty on share transfers.

- Annual Compliance: Financial statements must be prepared annually; companies meeting size thresholds must file with SUNAT and may require an external audit.

- Economic Substance: No formal substance requirements, though a Gerente General must be designated and operational decisions should be documented locally.

- Share Transfer Restrictions: Existing shareholders hold a statutory right of first refusal under Law No. 26887 before shares can be transferred to third parties.

- Conversion: An SAC can be converted to a Sociedad Anónima Abierta (SAA) if it exceeds 750 shareholders or lists on the stock market, triggering additional regulatory obligations.

Recommendations

The SAC is well-suited for trading operations, family-owned businesses, and joint ventures requiring limited liability without public disclosure obligations. Its share transfer restrictions provide internal control, though they can complicate exits for investors seeking liquidity.

This entity works best for small to mid-sized private businesses, foreign investors entering through a locally registered vehicle, and family-held companies that need defined shareholder control without public market exposure.

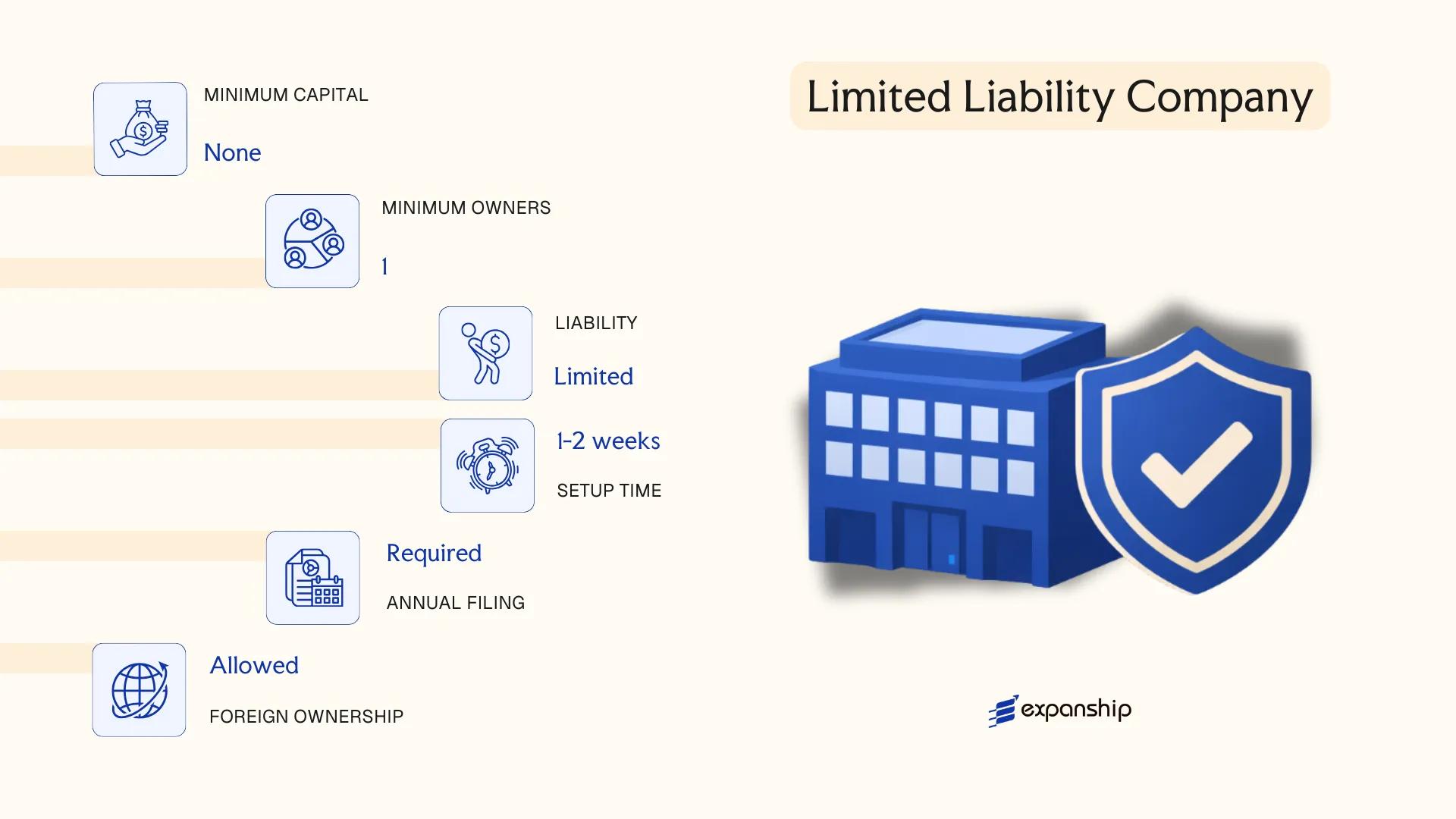

Sociedad de Responsabilidad Limitada (SRL) — Limited Liability Company

The Sociedad de Responsabilidad Limitada Peru SRL is governed by the Ley General de Sociedades, Ley No. 26887, enacted in 1997. As a distinct legal entity, it separates the personal assets of its members from the obligations of the business.

Structurally, the SRL sits between a corporation and a partnership. Liability is capped at each member's capital contribution, yet decision-making remains informal compared to the Sociedad Anónima variants — making it a practical choice for closely held businesses.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Separate legal personality under Ley No. 26887 |

| Members | 2 minimum, 20 maximum | Referred to as socios; no shares issued — interests represented by participaciones |

| Management | One or more gerentes (managers) | Managers need not be members; at least one must be designated |

| Registered Address | Local registered office required | Must be maintained within Peru; used for SUNAT and SUNARP correspondence |

| Capital | No statutory minimum; denominated in PEN | Contributions must be fully paid upon incorporation |

| Privacy | Member names filed with SUNARP | Registry records are publicly accessible |

Focus Points

- Taxation: Subject to 29.5% corporate income tax; VAT (IGV) applies at 18%; profit distributions to foreign members attract a 5% withholding tax; no separate stamp duty regime on equity contributions.

- Annual Compliance: Must file annual financial statements and tax returns with SUNAT; no mandatory external audit unless thresholds trigger statutory requirements.

- Transfer Restrictions: Participaciones are not freely transferable — existing members hold a right of first refusal, and transfers require approval per the company's estatuto.

- Treaty Access: Peru's double taxation treaties may apply, subject to beneficial ownership and substance requirements at the member level.

- Conversion: An SRL may convert to a Sociedad Anónima Cerrada or other recognised form through a formal process registered with SUNARP.

Closing

The SRL suits small to mid-sized trading and services businesses where ownership remains concentrated among a limited group of partners. Its simplified governance reduces administrative overhead, though the 20-member cap makes it unsuitable for ventures requiring broad equity participation or external investment rounds.

Closely held domestic or foreign-owned operating companies with a small, stable ownership group that does not require share issuance or public capital access.

Partnerships in Peru [Sociedad Colectiva, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones]

Partnership structures in Peru, including the Sociedad Colectiva, are governed by the Ley General de Sociedades (General Corporation Law), Ley No. 26887, enacted in 1997. All three partnership forms recognized under this legislation acquire separate legal personality upon registration with the Registros Públicos (SUNARP), distinguishing them from simple contractual arrangements.

Unlike capital-based structures, these entities place greater emphasis on the identity and personal standing of their partners. The degree of personal liability each partner assumes depends on the specific form chosen.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Colectiva (SC), Sociedad en Comandita Simple (SCS), Sociedad en Comandita por Acciones (SCA) | Three distinct forms under Ley No. 26887 |

| Members | SC: minimum 2 partners (no maximum); SCS: at least 1 general + 1 limited partner; SCA: at least 1 general partner + shareholders | All general partners bear unlimited personal liability |

| Local Presence | Registered address in Peru required; registered with SUNARP | No statutory requirement for a local resident manager, though general partners are personally accountable |

| Capital | No statutory minimum capital; SCA issues shares for limited partners | Capital contributions defined by the partnership agreement (escritura social) |

| Privacy | Partner names are disclosed in public registry filings | Limited confidentiality; all partners appear on record at SUNARP |

Focus Points

- Taxation: Partnerships are generally treated as pass-through entities for Peruvian income tax purposes, with profits attributed to partners; VAT obligations apply to commercial activities at the standard 18% rate; withholding tax may apply to distributions to non-resident partners.

- Annual Compliance: Entities must file annual financial statements and maintain accounting records in accordance with SUNAT requirements; the SC and SCS have lighter reporting burdens than the SCA, which issues shares.

- Liability Exposure: General partners in all three forms bear unlimited, joint, and several liability for entity obligations — a significant structural risk for operating businesses.

- Conversion: Under Ley No. 26887, partnerships may convert to other recognized corporate forms through a formal transformation process (transformación), subject to partner consent.

- Restrictions: Foreign nationals may act as general partners, but all entities must comply with Peruvian foreign investment registration requirements under applicable PROINVERSIÓN regulations.

Sub-Types

Sociedad Colectiva (SC)

All partners hold equal unlimited liability, and management rights are shared among them unless the partnership agreement specifies otherwise. This structure is uncommon in practice and is rarely used for anything beyond small, closely-held professional or family operations.

Sociedad en Comandita Simple (SCS)

Peru limited partnership registration under this form introduces two partner classes: general partners with unlimited liability who manage the entity, and limited partners (comanditarios) whose liability is capped at their capital contribution. Limited partners cannot participate in management without risking the loss of their limited liability status.

Sociedad en Comandita por Acciones (SCA)

The SCA divides capital into shares held by limited partners, while one or more general partners retain full personal liability and management control. This hybrid structure resembles a corporation in its capital mechanics but retains the personal liability exposure characteristic of the Sociedad en Comandita Peru framework.

Closing

These partnership forms are rarely chosen for commercial trading or holding purposes given the unlimited liability exposure carried by general partners; they appear most often in professional services or legacy family business arrangements where partner identity is central to the venture. The primary limitation is the personal liability of general partners, which creates meaningful financial risk.

These structures are best suited for small professional firms or family ventures where the partners have an established relationship and are comfortable with shared personal liability.

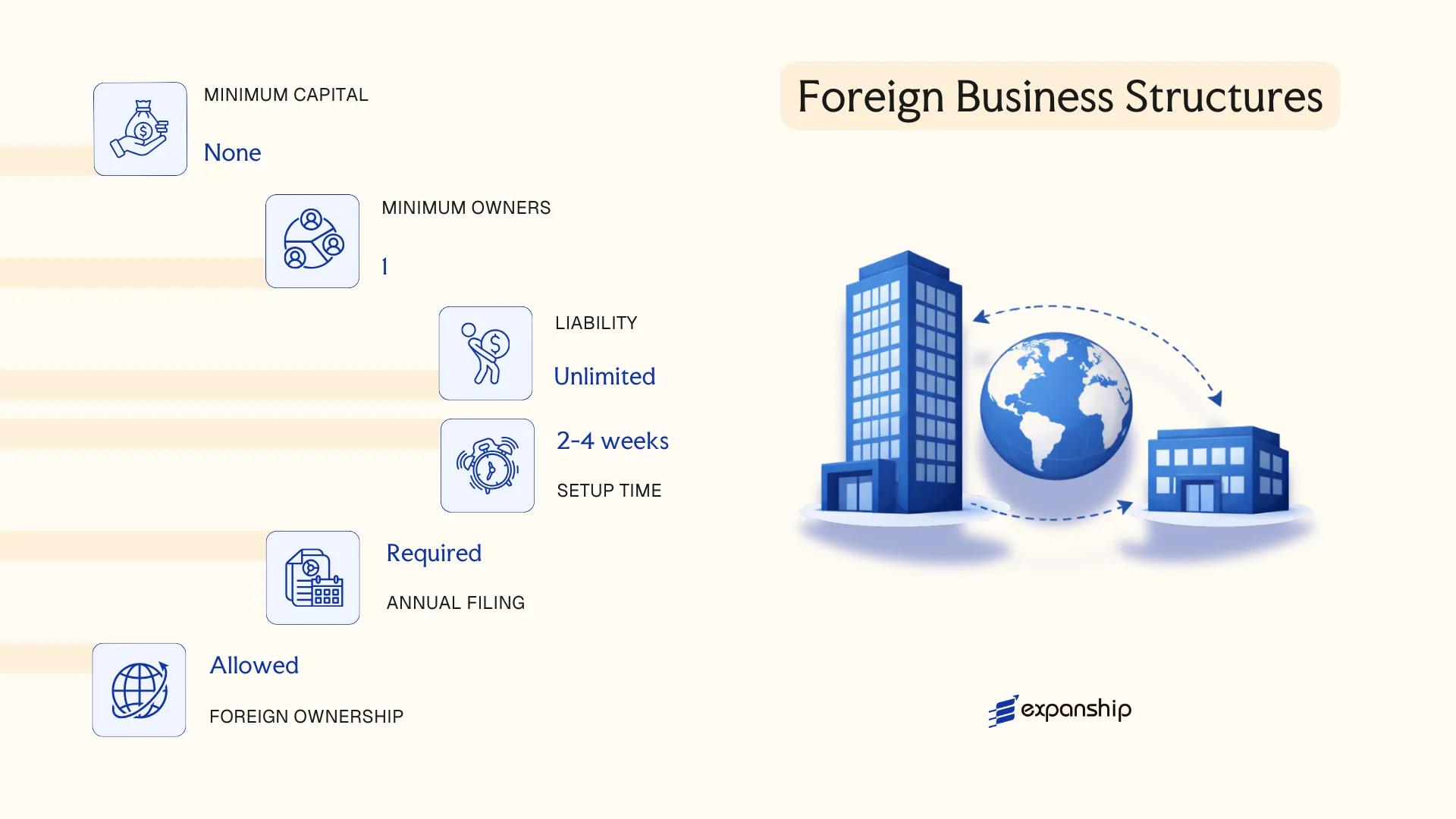

Foreign Business Structures in Peru [Branch Office, Representative Office]

Foreign companies seeking to operate in Peru without incorporating a separate local entity have two principal options: a branch office (sucursal) or a representative office (oficina de representación). Foreign branch office in Peru registration is governed by the General Corporations Law (Ley General de Sociedades, Law No. 26887), specifically Articles 396 to 406, which outline the obligations and limitations applicable to foreign entities establishing a permanent presence.

A branch (sucursal) is not a separate legal entity — it remains an extension of the parent company, which bears full liability for its obligations in Peru. Registration is processed through the Public Registry (SUNARP), and the branch must also obtain a tax identification number (RUC) from SUNAT.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Legal Representative | Appointed local representative (apoderado) required | Appointed local representative required |

| Liability | Parent company bears unlimited liability | Parent company bears unlimited liability |

| Permitted Activities | Full commercial and trading operations | Liaison and promotional activities only; no revenue-generating operations |

| Local Registration | SUNARP registration + RUC from SUNAT | RUC from SUNAT; SUNARP registration may apply depending on activity |

| Capital | No statutory minimum; parent must assign working capital | No capital assignment required |

Focus Points

- Taxation: Branch profits are subject to the standard corporate income tax rate of 29.5%; remittances to the foreign parent attract an additional withholding tax of 5% (applicable to deemed dividends); VAT at 18% applies to taxable supplies; no separate stamp duty on branch registration.

- Economic Substance: The branch must maintain demonstrable operational activity in Peru and file annual financial statements with SUNAT.

- Annual Compliance: Obligations include monthly tax filings, annual income tax returns, and renewal of the appointed representative's powers where applicable.

- Treaty Access: Peru's tax treaty network is limited; treaty benefits depend on the parent's jurisdiction and the specific treaty provisions covering permanent establishments.

- Restrictions: A representative office cannot invoice clients or generate local revenue; any commercial activity converts the structure into a taxable permanent establishment.

Sub-Types

Branch Office (Sucursal)

A fully operational extension of the foreign parent, permitted to conduct commercial transactions, sign contracts, and generate revenue. Registration with SUNARP is mandatory, and the branch must file independently with SUNAT for all Peruvian tax purposes.

Representative Office (Oficina de Representación)

Restricted to non-commercial functions such as market research, promotion, and liaison with local contacts. It cannot enter revenue-generating contracts on behalf of the parent, and its scope must remain auxiliary to the parent's overseas operations.

Both structures suit foreign companies testing the Peruvian market or managing regional operations before committing to full local incorporation. The branch offers operational flexibility without separate legal incorporation, though the parent's unlimited liability exposure is a material consideration.

Foreign companies with established operations seeking direct market access in Peru without forming a separate legal entity — particularly those in trading, services, or regional coordination roles.

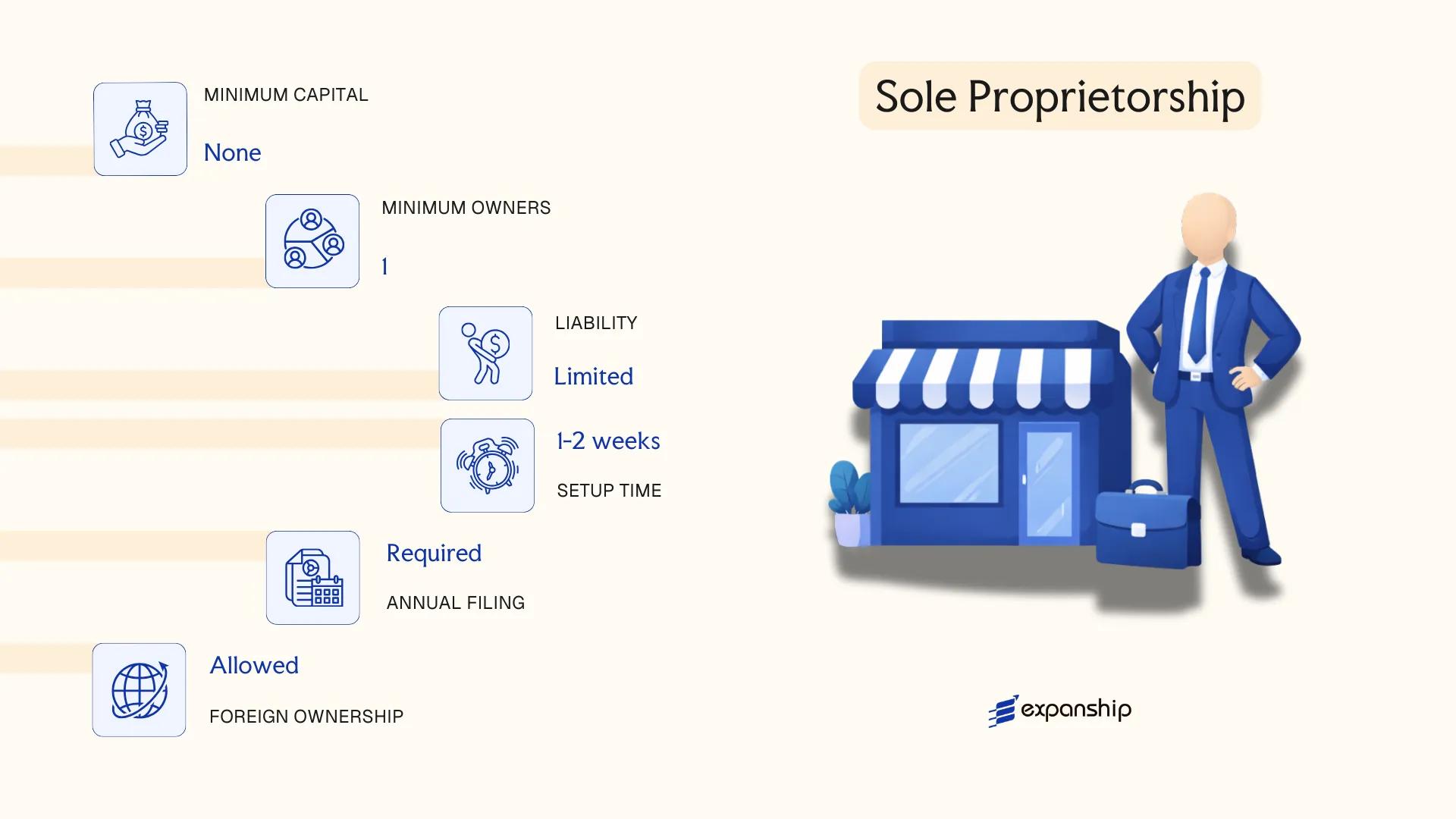

Sole Proprietorship in Peru [Empresa Individual de Responsabilidad Limitada (EIRL)]

The Empresa Individual de Responsabilidad Limitada Peru EIRL is the only single-person business structure in the country that carries separate legal personality. Governed by Decree Law No. 21621 of 1976, it creates a distinct legal entity whose patrimony is separate from the proprietor's personal assets, providing liability protection that a simple sole trader arrangement does not.

Structurally, the EIRL is a hybrid: it functions like a limited liability company yet has exactly one natural person as its owner. The proprietor's exposure is confined to the capital contributed to the entity. Registration is processed through SUNARP (Superintendencia Nacional de los Registros Públicos), and the firm must also obtain a RUC (Registro Único de Contribuyentes) from SUNAT before commencing operations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Empresa Individual de Responsabilidad Limitada | Separate legal personality; distinct patrimony from proprietor |

| Owner | Single natural person (Titular) | Legal persons (companies) cannot form an EIRL |

| Local Presence | Registered address in Peru required | No statutory registered agent requirement, but a domicile must be declared with SUNARP |

| Share Capital | No statutory minimum; denominated in PEN | Capital is declared at formation and ring-fenced from personal assets |

| Management | Gerente (Manager) appointed by the Titular | Titular may also serve as Gerente |

| Privacy | Ownership details filed with SUNARP and are publicly accessible | No meaningful privacy protection |

Focus Points

- Taxation: Subject to corporate income tax at 29.5% on net profits; VAT (IGV) applies at 18% on taxable transactions; subject to SUNAT's standard withholding and payroll tax regimes where applicable.

- Annual Compliance: Must file annual income tax returns with SUNAT and maintain accounting records in accordance with Peruvian GAAP.

- Conversion: Can be converted into a SAC or SRL if the business grows and requires additional shareholders, following procedures under the Ley General de Sociedades (Law No. 26887).

- Restrictions: Only natural persons resident or non-resident may form an EIRL; corporate entities are excluded as proprietors under Decree Law No. 21621.

- Treaty Access: As a tax-resident entity, the EIRL may access Peru's double taxation agreements, subject to meeting beneficial ownership and substance requirements.

Closing

The EIRL suits small-scale trading, service provision, or early-stage operations where a single founder requires liability separation without the administrative overhead of a multi-member structure. Its principal limitation is the restriction to one natural-person owner, which makes it unsuitable for any venture requiring equity participation from investors or co-founders.

The EIRL is best suited for individual entrepreneurs and freelancers who need personal asset protection but operate independently without partners or institutional investors.

How to Choose the Right Entity Type in Peru

Knowing how to choose a company type in Peru requires more than a preference for limited liability. The structure you register has direct legal, fiscal, and operational consequences that are difficult to reverse once formation is complete.

Why Your Entity Choice Matters

The wrong structure can produce concrete, costly outcomes:

- A foreign firm registering a representative office while conducting direct commercial transactions violates the terms under which SUNARP registered the entity, exposing it to administrative sanctions and forced closure.

- Selecting an EIRL when a business grows to multiple investors forces a full dissolution and re-registration, since the EIRL structure is legally restricted to a single natural person as owner.

- Choosing a structure that requires audited financial statements under the Ley General de Sociedades when your operation is a one-person consultancy introduces annual compliance costs with no corresponding regulatory benefit.

- Operating through an SAC while exceeding 750 shareholders triggers mandatory conversion obligations under securities law, with non-compliance resulting in regulatory action by the SMV.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sectors each point to different structures under Peru's Ley General de Sociedades (Ley N° 26887).

- Ownership Structure: A single natural person owner is limited to the EIRL, while multi-party ownership requires an SAC, SAA, or SRL depending on the number and type of shareholders.

- Shareholder Cap: The SAC is capped at 750 shareholders; exceeding this threshold requires conversion to an SAA subject to SMV oversight.

- Tax Objectives: Your eligibility for specific regimes — including the Régimen MYPE Tributario or the general corporate tax regime — depends partly on entity type and annual revenue thresholds.

- Management Flexibility: The SRL and SAC permit simplified governance without mandatory board structures, while the SAA requires a formal directorio and broader disclosure obligations.

- Exit and Conversion: Not all structures allow redomiciliation or conversion without full dissolution; confirm exit pathways before registering.

Corporate Compliance Services in Peru

Maintain good standing with SUNARP, SUNAT, and other Peruvian regulatory bodies through structured compliance support.

Conclusion

Selecting the right structure is one of the most consequential decisions in any incorporating a company in Peru guide. Each entity under the Ley General de Sociedades serves a distinct purpose: the SAC suits closely held businesses with a small shareholder group; the SAA applies to firms seeking public capital markets access; the SRL fits professional services and family-owned operations; the EIRL serves sole operators who require liability separation; branch offices address foreign companies testing the local market; and partnerships accommodate ventures where personal liability is accepted by design. Among these, the SAC is the most frequently registered structure, reflecting a broad preference for limited liability without public disclosure obligations. SUNARP registration volumes consistently show this trend. Peru has expanded its tax treaty network in recent years, and SUNAT continues to align transfer pricing enforcement with OECD standards, signaling a regulatory environment that rewards structured, compliant incorporation from the outset. Expanship maintains current working knowledge of these requirements across all entity types.

How Expanship Can Assist You

Accessing corporate services for Peru company formation means working within a system governed by the Ley General de Sociedades (Ley N° 26887) and overseen by the Superintendencia Nacional de los Registros Públicos (SUNARP). Whether your business suits a Sociedad Anónima Cerrada, a Sociedad de Responsabilidad Limitada, or another structure covered in this guide, Expanship manages the process directly with the relevant Peruvian authorities.

Our team handles every procedural and compliance stage on your behalf:

- Document preparation, notarization, and legalization

- Registered agent and local registered address provision

- Filing with SUNARP and coordination with SUNAT for tax registration

- Ongoing compliance management, including annual obligations

- Banking introduction assistance to support account opening in Peru

Ready to move forward? Contact Expanship Peru to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The Sociedad Anónima Cerrada (SAC) is the most frequently formed entity. Its shareholder limit of up to 20, optional supervisory board, and restriction on public share transfer make it practical for small and medium-sized businesses.

A Branch Office has no independent legal personality and its parent company bears full liability for local obligations, while a SAC is a separate legal entity with liability confined to its capital. Branch offices are also restricted from issuing shares, whereas a SAC can distribute equity among up to 20 shareholders.

The Sociedad de Responsabilidad Limitada (SRL) and the SAC both limit publicly accessible ownership data relative to open corporations, but neither offers nominee shareholding frameworks comparable to offshore jurisdictions. Beneficial ownership disclosures are required under SUNAT and UIF-Peru regulations regardless of entity type.

No. The Empresa Individual de Responsabilidad Limitada (EIRL) is the only structure expressly designed for a sole founder. Partnerships such as the Sociedad Colectiva require at least two partners, and SACs require a minimum of two shareholders.

Foreign nationals may incorporate a SAC, SAA, or SRL without residency requirements at the shareholder level. However, at least one director or manager with a local tax registration (RUC) and, in practice, a Peruvian address is generally required for operational compliance with SUNAT.

The LGS permits the transformation of one corporate form into another through a formal transformation process, provided shareholders approve it and public notice requirements are met. An SRL can convert to a SAC, or a SAC to an SAA, without dissolving and reconstituting the entity from scratch.

Not all. The SAC, SAA, SRL, and EIRL each hold separate legal personality under Peruvian law. A Representative Office, by contrast, is not an independent legal entity and cannot enter into contracts or generate revenue in its own name.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.