Key Takeaways

- Malawi's corporate tax rate, administered by the Malawi Revenue Authority (MRA), sits at a level that measurably reduces after-tax returns compared to more competitive jurisdictions in the region.

- Company formation processed through the Malawi Business Registration System (MBRS) is subject to procedural delays that extend the timeline before a foreign entity can legally commence operations.

- Foreign investors face restrictions on land ownership rights and equity participation in certain sectors, limiting the structural flexibility available when establishing a local presence.

- The Companies Act framework, while providing the legal foundation for incorporation, operates alongside foreign exchange controls that complicate profit repatriation and cross-border capital movement for internationally operating businesses.

Malawi operates under an evolving regulatory framework, with company formation and ongoing compliance governed primarily by the Companies Act and administered through bodies such as the Registrar General's Department. The disadvantages of incorporating in Malawi span procedural, financial, infrastructural, and operational categories.

Not every challenge applies equally across all sectors. A manufacturing firm faces a different set of constraints than a professional services company, and the severity of each drawback shifts depending on your ownership structure and the scale of your operations.

This article is most relevant to foreign investors and internationally operating businesses considering a formal presence in the country, particularly those unfamiliar with the specific regulatory and commercial conditions that govern company registration and ongoing compliance here.

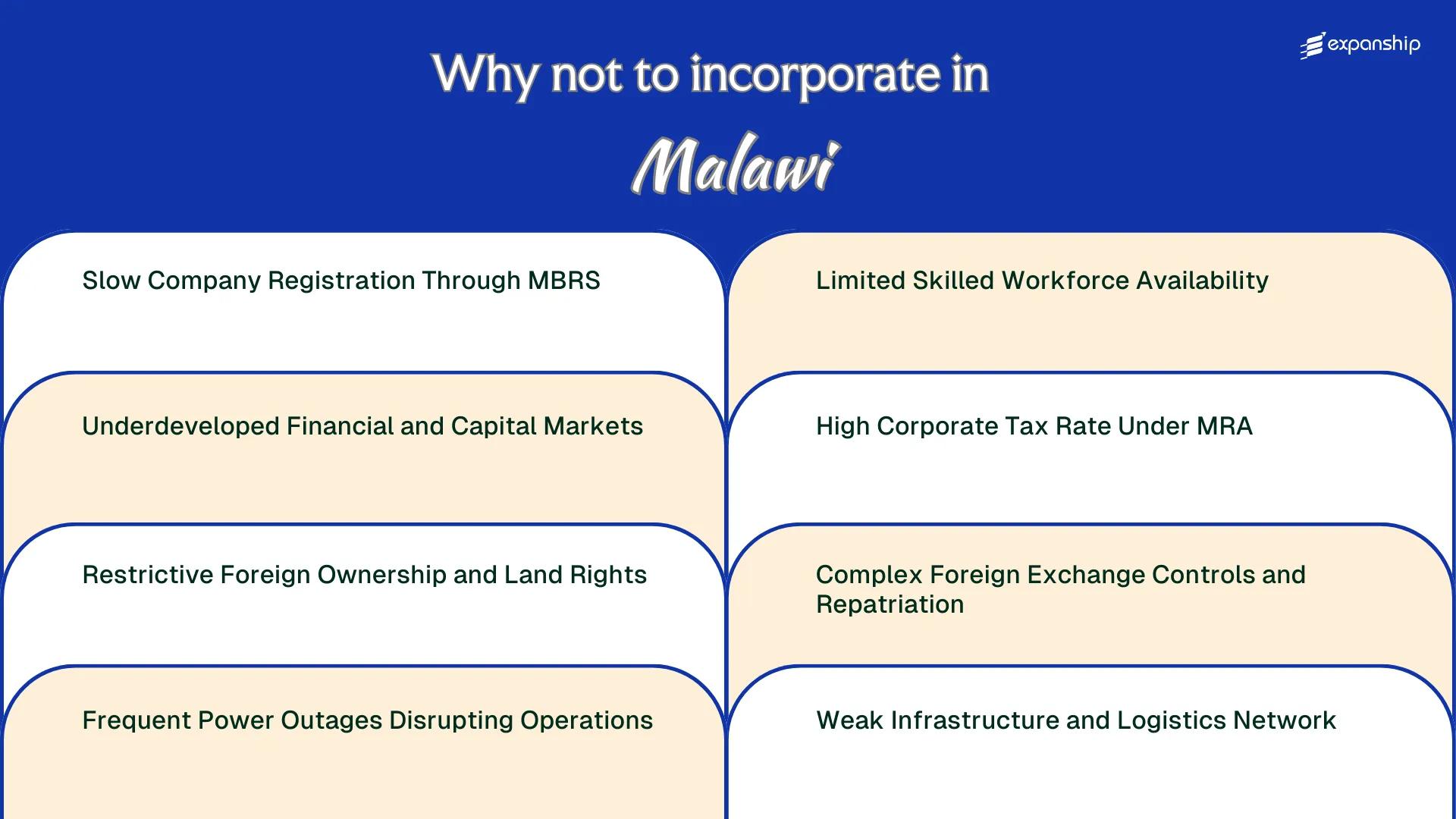

Slow Company Registration Through MBRS

Slow company registration through MBRS is a consistent friction point for foreign investors entering Malawi, where the official incorporation process often diverges sharply from published timelines.

Registry Backlogs and System Reliability

The Malawi Business Registration Service, established under the Companies Act 2013, serves as the central body for entity registration. System outages, manual processing fallbacks, and administrative backlogs mean that what the MBRS presents as a straightforward online process frequently extends well beyond the stated timeframe, directly delaying your ability to open bank accounts, sign contracts, or begin operations.

Registration delays are not uniformly distributed. Firms requiring additional approvals, such as those in regulated sectors, face compounding wait times because MBRS coordination with sector-specific regulators adds unpredictable layers to the process.

Practical Cost of Delayed Incorporation

Every week your entity remains unregistered represents a week in which local contracts cannot be executed under a Malawian legal identity. This has direct cost implications for businesses that have already committed to lease agreements, employment offers, or supplier arrangements.

The MBRS incorporation problems in Malawi disproportionately affect foreign businesses without local legal representatives who can physically follow up with the registry.

Until your company receives its certificate of incorporation from MBRS, it has no legal standing to transact, employ staff, or open a local bank account, leaving time-sensitive business commitments legally unenforceable.

Underdeveloped Financial and Capital Markets

Underdeveloped capital markets in Malawi present a concrete financing problem for foreign businesses. The Malawi Stock Exchange (MSE) lists fewer than 20 securities, limiting your ability to raise equity capital or exit investments through public markets.

Debt financing is similarly constrained. Commercial banks operating under Reserve Bank of Malawi oversight maintain high lending rates, often exceeding 20%, which makes local borrowing an expensive alternative to foreign capital.

For a foreign-owned entity, these structural limitations translate into specific operational burdens:

- Raising growth capital locally is not a viable option, forcing dependence on offshore funding that must pass through foreign exchange controls

- Limited institutional investment activity means your business cannot attract local institutional co-investors or fund participation

- The absence of developed bond markets restricts access to long-term debt instruments, pushing short-term financing costs higher

- Thin market liquidity on the MSE reduces the prospect of a domestic equity exit, which complicates investor return strategies from the outset

Microfinance institutions and development finance bodies like the Malawi Development Corporation exist, but their mandates and capital availability do not substitute for a functioning capital market serving private commercial entities.

Company Incorporation in Malawi

Understand the full regulatory and financial environment before establishing your entity in Malawi.

Restrictive Foreign Ownership and Land Rights

Foreign ownership restrictions in Malawi create structural barriers that go beyond administrative inconvenience. Under the Companies Act 2013, foreign nationals may incorporate private limited companies, but certain sectors are reserved exclusively for Malawian citizens, limiting where your firm can legally operate.

Land ownership presents a separate and more acute constraint. The Malawi Constitution and the Land Act 2016 prohibit foreigners from owning freehold land. Your business can only access land through leasehold arrangements, typically granted for fixed terms by the Commissioner of Lands.

| Restriction | Applicable Law | Practical Burden |

|---|---|---|

| No freehold land ownership for foreigners | Land Act 2016 | Long-term asset security is unavailable; leasehold must be renegotiated |

| Lease terms subject to government discretion | Commissioner of Lands authority | Renewal is not guaranteed, creating operational uncertainty |

| Sector restrictions on foreign participation | Investment and Export Promotion Act | Limits the range of industries accessible to foreign-owned entities |

| Leasehold maximum terms vary by land category | Land Act 2016 | Short or mid-term leases increase planning and financing complexity |

Leasehold dependency means your business cannot use land as collateral in the same way a freehold owner could, which directly restricts access to local secured financing. Lenders typically discount leasehold security, particularly when remaining lease terms are short relative to loan tenure.

Sector exclusions compound the land access problem. If your intended business activity falls within a protected category, restructuring ownership to include a Malawian partner becomes a practical requirement rather than a choice, diluting your control over the entity.

Frequent Power Outages Disrupting Operations

Power outages disrupting business in Malawi represent one of the most immediate operational risks for any foreign entity establishing a presence in the country. The Electricity Supply Corporation of Malawi (ESCOM) manages the national grid, which relies heavily on hydropower generated along the Shire River. During drought periods, reduced water levels directly cut generation capacity, triggering extended load shedding schedules that can affect commercial operations for eight to twelve hours per day.

For a foreign firm running time-sensitive processes, that kind of interruption is not a minor inconvenience. It translates into lost productivity, equipment damage from voltage fluctuations, and supply chain delays that compound across weeks.

Backup generation through diesel generators adds a recurring cost that is absent in more grid-stable markets across southern Africa, such as South Africa or Zambia during non-drought cycles.

- Load shedding schedules are subject to change without advance notice from ESCOM

- Businesses in manufacturing or cold-chain logistics face disproportionate exposure to outage-related losses

- Generator fuel costs must be factored into operational budgets as a baseline expense, not a contingency

- Voltage instability during grid restoration periods can damage unprotected equipment

- No statutory compensation mechanism exists for commercial losses caused by supply interruptions

Malawi generates over 90% of its electricity from hydropower, meaning a single prolonged dry season can destabilize the entire national grid simultaneously.

Limited Skilled Workforce Availability

Sourcing adequately trained professionals is one of the more concrete limited skilled workforce Malawi drawbacks that foreign businesses encounter when establishing operations there.

Structural Gaps in Human Capital

Malawi's education system produces a relatively small pool of graduates with technical, financial, or managerial qualifications each year. For a foreign-incorporated entity requiring specialist roles in accounting, engineering, or ICT, this scarcity directly translates into longer recruitment cycles and higher compensation premiums to retain qualified local staff.

The National Council for Higher Education oversees tertiary institutions, but graduate output remains insufficient relative to private sector demand. Businesses operating under the Companies Act 2013 still face implicit pressure to prioritize local hiring, which compounds the talent shortage challenge when specialized roles cannot be filled domestically.

Operational and Cost Consequences

Filling senior or technical vacancies through expatriate hires triggers work permit obligations under the Immigration Act, adding both processing time and administrative cost. Each work permit application requires justification that no qualified Malawian candidate was available, creating a compliance burden that delays operational timelines.

This dependency on expatriate talent is not uniform across all sectors; labor-intensive industries face different pressures than knowledge-based firms, but human capital limitations incorporating in Malawi affect most foreign entities above a certain operational complexity.

Addressing Workforce and Operational Challenges in Malawi

Get structured guidance on managing compliance obligations, work permit requirements, and incorporation considerations when setting up in Malawi.

High Corporate Tax Rate Under MRA

The high corporate tax rate Malawi MRA enforces creates a measurable cost disadvantage for foreign-incorporated entities from the moment the business turns profitable. The standard corporate income tax rate sits at 30%, collected and administered by the Malawi Revenue Authority under the Taxation Act (Cap. 41:01).

- At 30%, the standard corporate income tax rate directly reduces post-tax returns available for reinvestment or repatriation, which raises the effective cost of operating through a locally incorporated entity.

- The MRA requires companies to pay provisional tax in quarterly installments throughout the fiscal year, meaning your firm carries a continuous cash flow obligation before final liability is even confirmed.

- Non-resident companies face a withholding tax on dividends paid out of Malawi, adding a second layer of tax friction on top of the corporate rate when distributing profits abroad.

- Transfer pricing rules under the Taxation Act impose documentation requirements on related-party transactions, creating compliance costs that fall disproportionately on foreign-owned subsidiaries with cross-border intragroup dealings.

Complex Foreign Exchange Controls and Repatriation

Foreign exchange controls Malawi imposes on cross-border transactions create measurable friction for foreign-owned entities seeking to move capital out of the country. The Reserve Bank of Malawi (RBM) governs all foreign currency transactions under the Exchange Control Act, and while the kwacha became formally convertible on the current account, capital account restrictions remain in place.

Repatriating dividends, loan repayments, or proceeds from asset sales requires prior RBM approval in most cases. Delays in that approval process can hold funds in-country for weeks or months, creating currency exposure during that period.

The Malawian kwacha has historically been subject to significant depreciation pressure. If your approval is delayed and the kwacha weakens further against your reporting currency, the real value of what you repatriate shrinks without any change in the underlying business performance.

Documentary requirements for repatriation transactions are also substantial. Your firm must typically provide audited accounts, tax clearance certificates from the Malawi Revenue Authority, and evidence of the original investment.

Hypothetical scenario: A foreign investor repatriating $200,000 in dividends faces a 90-day approval delay. If the kwacha depreciates 8% against the USD during that window, the effective value transferred drops to approximately $184,000, a loss of $16,000 attributable entirely to the repatriation process, not business performance.

Weak Infrastructure and Logistics Network

Weak infrastructure logistics Malawi risks are most pronounced in freight movement and supply chain reliability. The country is landlocked, making all import and export activity dependent on transit corridors through neighbouring countries, primarily through Mozambican ports such as Beira and Nacala. Any disruption along those corridors, whether from political instability, port congestion, or cross-border delays, directly stalls your operations.

Road conditions present a structural constraint. A significant portion of the national road network is unpaved or poorly maintained, and heavy seasonal rains regularly render rural and peri-urban routes impassable.

- Delivery lead times are unpredictable, complicating inventory planning and contractual fulfilment timelines.

- Cold chain logistics are limited, which affects businesses in agriculture, pharmaceuticals, and food processing.

- Rail infrastructure, managed under historical concession frameworks, offers minimal reliable freight capacity.

For businesses that depend on time-sensitive goods movement, these transport network challenges translate directly into higher logistics costs and missed delivery windows.

If your business model requires consistent, time-bound import or export cycles, the absence of a reliable domestic freight network means you will carry logistics risk that cannot be resolved through entity structuring alone.

Overcoming These Incorporation Challenges

Overcoming Malawi incorporation challenges requires structural preparation before the business is registered, not reactive adjustments after problems emerge. No single workaround eliminates the friction entirely, but deliberate entity structuring and regulatory alignment reduce material exposure.

- Register your company through the MBRS portal in advance of operational timelines to absorb processing delays without disrupting launch schedules.

- Structure equity arrangements to comply with the Companies Act 2013 and any sector-specific foreign ownership thresholds before submitting incorporation documents.

- Apply to the Reserve Bank of Malawi for the relevant foreign exchange approvals prior to transferring capital, to avoid repatriation blocks at a later stage.

- Source backup power infrastructure contractually before commencing operations, given the regularity of ESCOM grid interruptions.

- Engage directly with the Malawi Revenue Authority to confirm applicable corporate tax obligations and available deductions under the Taxation Act.

Mitigating risks of incorporating in Malawi depends on how thoroughly a foreign firm maps its structure against the existing regulatory framework before entry. The steps above address documented friction points, but they do not remove the underlying structural constraints of the jurisdiction.

Malawi's Overall Investment Viability

Malawi investment viability risks assessment places the country in a challenging but not dismissible category. The structural constraints covered in this blog are real and measurable, yet the country maintains a functioning legal framework for foreign business under the Companies Act 2013, a stable multiparty political system, and access to regional markets through COMESA and SADC membership. For the right business profile, those foundations carry weight.

| Pros | Cons |

|---|---|

| Companies Act 2013 provides a codified legal framework for foreign-owned entities | MBRS registration processes remain slow, creating delays before a business can legally operate |

| COMESA and SADC membership opens preferential trade access across East and Southern Africa | Foreign ownership restrictions apply in certain sectors, limiting full equity control |

| Malawi Revenue Authority administers a defined corporate tax structure with published rates | The standard corporate tax rate is high relative to comparable regional jurisdictions |

| Agricultural and natural resource sectors offer documented commercial opportunities | Persistent power outages increase operating costs and reduce productivity |

| The Malawi kwacha is a convertible currency with a formal exchange rate regime | Repatriation of profits is subject to foreign exchange controls that can delay fund transfers |

Weak logistics infrastructure adds friction to supply chains, and a limited skilled labour pool narrows hiring options for firms requiring specialised functions.

Corporate Compliance Services for Companies in Malawi

Maintain good standing with the Registrar of Companies and meet your ongoing obligations under Malawian law, from annual returns to regulatory filings.

Conclusion

Malawi presents a measurable set of cons of incorporating in Malawi that any firm must assess before committing capital. Foreign exchange controls administered under the Reserve Bank of Malawi's framework, combined with high corporate tax exposure under the Malawi Revenue Authority, create sustained financial pressure on registered entities. Unreliable power supply further compounds operational costs in ways that affect day-to-day business continuity. Structural remedies for these constraints exist, but they typically require local legal counsel, sector-specific licensing knowledge, and a clear understanding of how the Companies Act 2013 applies to your intended business structure.

Expanship's Services for Malawi Expansion

Incorporating in Malawi involves working through the Malawi Business Registration System, meeting MRA tax obligations, and managing foreign exchange approvals through the Reserve Bank of Malawi. Expanship's Malawi company expansion services are structured to reduce the administrative weight these processes place on foreign businesses, particularly during the registration and early compliance phases. Your team can focus on operations while Expanship handles the procedural groundwork.

Beyond registration, Expanship covers the full formation and maintenance cycle for your entity in Malawi.

- Preparing and submitting company registration documents through MBRS on your behalf.

- Providing a registered agent and local office address to satisfy statutory presence requirements.

- Liaising with government offices, including the MRA and the Registrar General's Department, for filings and approvals.

- Managing ongoing post-incorporation compliance obligations as they fall due.

- Facilitating introductions to local banking institutions to support account opening.

- Handling tax registration and coordinating with local authorities on your firm's behalf.

Reach out through Expanship Malawi to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The Malawi Revenue Authority (MRA) applies a standard corporate tax rate of 30% to most resident companies. Certain sectors, such as those operating under approved development agreements or qualifying for special economic zone incentives, may attract different treatment, but the standard rate is what most foreign-owned firms will face. This rate, combined with other levies and withholding taxes, makes the overall tax burden meaningfully higher than in several competing regional jurisdictions.

Repatriating profits from Malawi requires prior approval through the Reserve Bank of Malawi, and delays in obtaining that approval can lock up working capital for extended periods. The Foreign Exchange Act governs these transactions, and non-compliance or incomplete documentation can trigger additional scrutiny or outright rejection. For businesses that depend on regular dividend flows back to a parent entity, this creates a structural cash flow risk that is difficult to plan around.

Restrictions on foreign ownership in Malawi are legally grounded, not merely administrative preferences. Certain sectors limit or prohibit foreign participation entirely, and foreigners cannot hold freehold title to land under the Malawi Land Act, which affects site acquisition for any business requiring physical premises. Leasehold arrangements exist as an alternative, but they introduce their own constraints around tenure length and renewal terms that add long-term uncertainty.

Malawi ranks among the weaker infrastructure environments in the COMESA and SADC regions. Chronic power outages, a landlocked geography with limited road and rail connectivity, and dependence on ports in Mozambique, Tanzania, and Zambia all add cost and transit time to supply chains. For businesses in manufacturing, agribusiness, or physical distribution, these constraints directly affect unit economics in ways that tax incentives rarely offset.

Failure to meet MRA compliance obligations, including corporate tax filings, PAYE submissions, and VAT returns, exposes the company to penalty surcharges and interest accruals under the Taxation Act. The MRA has the authority to issue assessments and, in persistent cases, pursue enforcement action including asset attachment. Foreign directors should be aware that non-residency does not shield a locally registered entity from these consequences.

The skills gap in Malawi is most acute in technical, financial, and managerial roles, while sectors requiring semi-skilled or unskilled labor are less affected. Foreign firms that require locally hired accountants, engineers, or compliance professionals often face either significant recruitment timelines or the added cost of expatriate placements, which in turn requires navigating work permit approvals through the Malawi Immigration Department. Industries dependent on specialist knowledge are disproportionately exposed to this constraint.

Foreign investors can hold majority or full ownership in certain company structures in Malawi, but sector-specific restrictions apply, and some industries require local equity participation. Beyond ownership percentages, the inability of foreign nationals to acquire freehold land under the Malawi Land Act 2016 creates a practical ceiling on asset ownership for businesses that rely on owned real property. Any corporate structure built around land ownership requires legal structuring to account for this restriction from the outset.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.