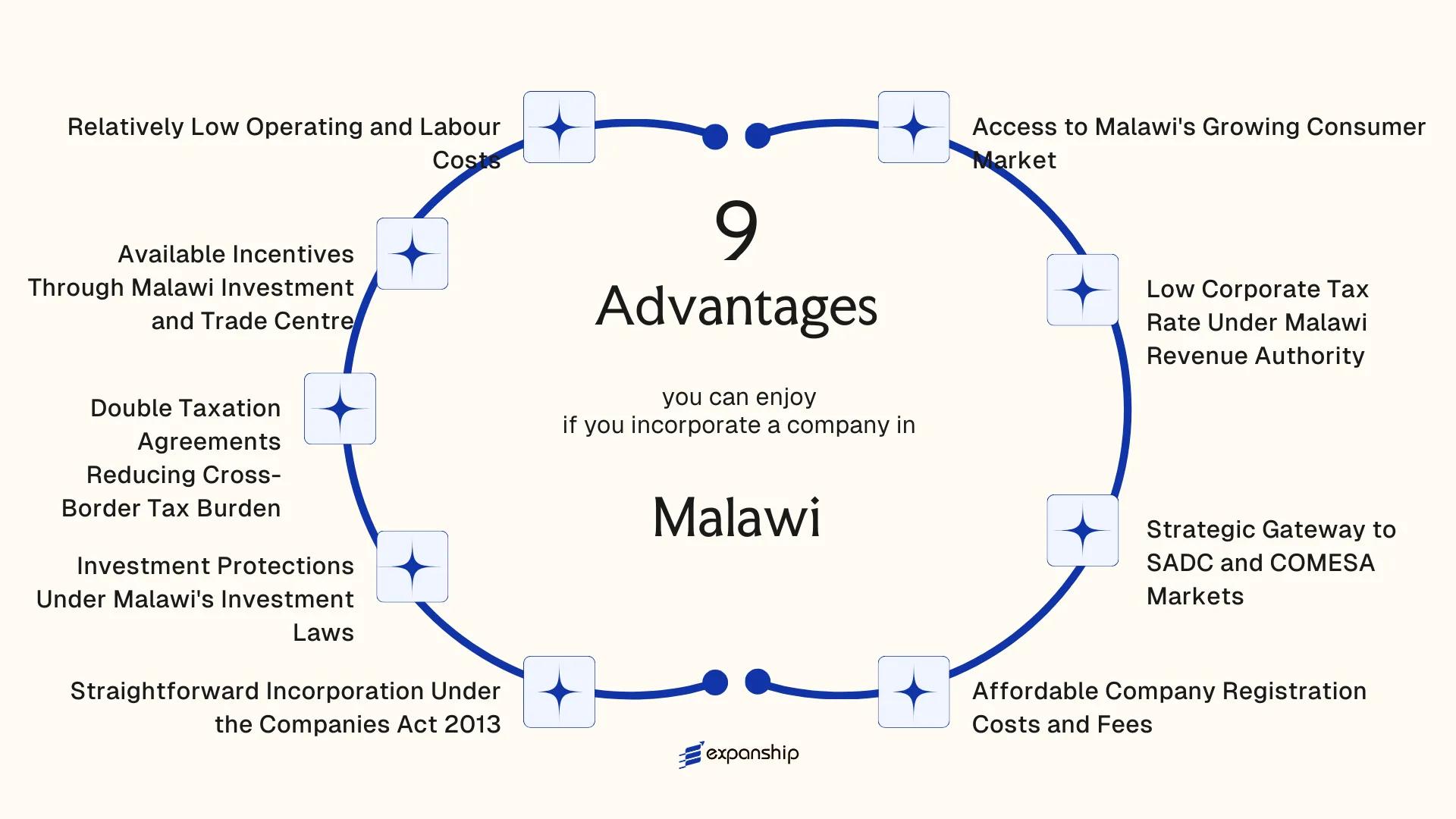

Key Takeaways

- Resident companies incorporated in Malawi are subject to a corporate tax rate of 30%, and where double taxation agreements apply, withholding obligations on cross-border income can be reduced further, lowering the effective cost of repatriating earnings.

- The Companies Act 2013 establishes a defined legal framework for company formation administered by the Registrar of Companies, giving foreign-owned entities a predictable and structured path to establishing a local presence.

- Membership in both SADC and COMESA grants businesses incorporated in Malawi preferential market access across a substantial regional trade bloc, reducing the tariff burden that non-member competitors face when moving goods across the same borders.

- Sector-specific incentives consolidated through the Malawi Investment and Trade Centre can meaningfully reduce capital outlay during the early stages of establishment for qualifying businesses.

Malawi is a landlocked, independent republic in southeastern Africa, bordered by Zambia, Tanzania, and Mozambique. Company registration falls under the oversight of the Registrar of Companies, which administers business formation under the Companies Act 2013. Foreign businesses establishing a local presence most commonly do so through a private limited company.

The country operates a territorial-based tax system, meaning tax liability generally applies to income sourced within its borders. On the question of foreign ownership, the regulatory framework is broadly open to foreign direct investment, and foreign nationals can typically hold shares in locally registered entities without restrictions tied to nationality.

Incorporating here is a structured process governed by a defined legal framework, and the benefits of incorporating in Malawi extend across areas that matter to internationally minded businesses. This article covers the key advantages relevant to companies considering formation in this jurisdiction.

Access to Malawi's Growing Consumer Market

Malawi's population exceeds 20 million people, with urbanisation steadily increasing demand for consumer goods, financial services, and manufactured products. For foreign investors, these Malawi growing consumer market benefits translate into a sizable addressable base that remains underpenetrated across multiple sectors.

A Domestic Market With Structural Demand

Household consumption accounts for a significant share of GDP, driven in part by a young population with a median age below 18 years. This demographic profile means demand for retail, telecommunications, and fast-moving consumer goods is expected to grow over the coming decade, giving your business a long-term demand runway rather than a saturated market entry point.

Regulatory Entry Points That Support Market Participation

Under the Companies Act 2013, a foreign-owned private limited company can trade directly within the domestic market without a mandatory local partner requirement. Registration with the Malawi Revenue Authority grants you tax identification, enabling formal commercial activity from the point of incorporation rather than requiring a secondary approval process.

A wholly foreign-owned entity can access domestic consumer demand directly under Malawian law, without equity-sharing obligations.

Low Corporate Tax Rate Under Malawi Revenue Authority

Malawi's standard corporate tax rate sits at 30% for most resident companies. While that figure is not the lowest globally, the Malawi Revenue Authority administers a tiered and incentive-laden regime that can materially reduce the effective rate for qualifying businesses, making the headline number less representative of what many foreign-owned entities actually pay.

For companies operating in designated priority sectors, the applicable rate can fall significantly below the standard threshold. Manufacturing firms, export-oriented businesses, and entities registered in special economic zones may access reduced rates or tax holidays administered through the MRA in conjunction with the Malawi Investment and Trade Centre. This means your effective tax burden depends heavily on the sector you operate in and the structure of your entity.

Several features of the MRA tax framework work in your favour as a foreign investor:

- Capital allowances under the Taxation Act permit accelerated depreciation on qualifying assets, reducing taxable profit in early operating years

- Export earnings may attract preferential treatment, directly improving after-tax margins on cross-border sales

- Farming and agro-processing activities carry sector-specific deductions not available in most comparable regional jurisdictions

The Taxation Act (Cap. 41:01) governs these provisions, giving them statutory backing rather than relying on discretionary policy.

Incorporate a Company in Malawi

Set up your Malawi-registered company with full compliance support from Expanship, covering MRA registration and sector-specific structuring.

Strategic Gateway to SADC and COMESA Markets

Positioned at the geographic heart of sub-Saharan Africa, Malawi holds membership in two of the continent's most significant regional trade blocs: the Southern African Development Community (SADC) and the Common Market for Eastern and Southern Africa (COMESA). Together, these two frameworks give a company registered here preferential access to a combined market exceeding 800 million people across more than 30 countries. For foreign investors, this is the Malawi gateway to SADC and COMESA markets that carries concrete commercial value.

Under COMESA's free trade area, qualifying goods traded between member states benefit from reduced or zero tariffs. SADC's Trade Protocol similarly provides for tariff liberalisation across its membership. A business incorporated locally can potentially access both frameworks simultaneously, which is a structural advantage not available in jurisdictions belonging to only one bloc.

| Trade Bloc | Member States | Key Trade Benefit |

|---|---|---|

| COMESA | 21 members | Preferential tariff rates within the free trade area |

| SADC | 16 members | Tariff liberalisation under the SADC Trade Protocol |

The practical implication is that your firm can use a single Malawian legal entity as the contracting and invoicing vehicle for cross-border trade across Eastern and Southern Africa. This reduces the need to establish separate subsidiaries in each target market. Eligibility for preferential treatment generally depends on meeting the rules of origin requirements stipulated in each bloc's respective protocols.

Affordable Company Registration Costs and Fees

Registering a business through the Registrar of Companies in Malawi carries affordable company registration Malawi benefits that directly reduce your upfront capital commitment. Government filing fees are structured to be accessible, and the total statutory cost of incorporating a private limited company remains modest by regional standards. That difference in cost translates into more working capital retained for actual operations from day one.

Under the Companies Act 2013, the incorporation process involves a defined set of payments, including name reservation and registration fees. Because these are fixed statutory charges rather than variable professional minimums, your exposure to unpredictable formation costs is limited.

Keep these points in mind to fully realise the cost advantage:

- Confirm current fee schedules directly with the Registrar of Companies, as rates are subject to periodic revision

- Account for the mandatory requirement to appoint a local registered address, which carries its own annual cost

- Verify whether your business activity triggers any sector-specific licensing fees payable to separate regulatory bodies

- Foreign-owned entities may face additional compliance steps that carry their own associated charges

Low cost business setup in Malawi also reflects the relatively short formation timeline. A faster registration process means less time paying advisors and waiting on administrative clearance before your firm can begin generating revenue.

Malawi's company registration fees are denominated in Malawian Kwacha, meaning foreign investors whose home currency is stronger effectively pay even less in real terms when settling statutory costs.

Straightforward Incorporation Under the Companies Act 2013

The Companies Act 2013 governs how businesses are formed and maintained in Malawi, and its structure reflects a deliberate effort to reduce administrative friction for incoming investors. The Malawi Companies Act 2013 incorporation benefits are most apparent when you examine how quickly a foreign entrepreneur can establish a legally recognised entity without navigating layers of pre-approval bureaucracy.

Registration Through a Single Legal Instrument

All private companies, public companies, and external companies operating in Malawi draw their legal authority from the Companies Act 2013, administered through the Registrar of Companies under the Office of the Registrar General. This unified framework means your business formation does not depend on sector-specific licences before incorporation can proceed. For a foreign investor, the absence of parallel registration tracks removes a common source of delay found in jurisdictions with fragmented corporate legislation.

Defined Requirements That Limit Uncertainty

Straightforward company registration under the Malawi Companies Act requires a minimum of one director and one shareholder, with no mandatory residency requirement for either. That single-person threshold means you can incorporate without first establishing a local management structure, which lowers the upfront organisational cost considerably. The Act also sets out prescribed constitutional documents, so there is no ambiguity about what the Registrar will accept at the point of filing.

Get Clarity on Your Malawi Incorporation

Speak with a specialist about structuring your company formation correctly under the Companies Act 2013.

Investment Protections Under Malawi's Investment Laws

Malawi investment protection laws for foreign investors are anchored in the Malawi Investment and Trade Centre Act and the broader investment regulatory framework, which together establish formal protections that reduce legal exposure for foreign-owned entities.

- The Investment and Trade Centre Act grants foreign investors the right to repatriate profits, dividends, and capital. Your business can transfer returns abroad without government interference, which removes a common barrier that makes operating through a foreign subsidiary financially impractical in other markets.

- Protection against expropriation without compensation is a statutory principle under Malawian investment law. The state is prohibited from nationalising or seizing foreign-owned assets without providing fair and prompt compensation, giving your firm a defined legal remedy rather than leaving you exposed to unilateral government action.

- Malawi is a member of the Multilateral Investment Guarantee Agency (MIGA), a World Bank Group body. MIGA membership means eligible investors can access political risk insurance covering non-commercial losses such as currency inconvertibility or civil disturbance, adding a layer of security that sits outside domestic legal systems.

- Dispute resolution mechanisms available to foreign investors include access to international arbitration under frameworks recognised by the state. This matters because local court proceedings can be slow, and an arbitration clause provides a predictable, enforceable path to resolving commercial disputes.

Double Taxation Agreements Reducing Cross-Border Tax Burden

Malawi double taxation agreements benefits are most visible when profits, dividends, or royalties cross borders. Without treaty protection, the same income can be taxed twice: once in the country where it is earned and again in the recipient's home country.

Malawi has concluded tax treaties with several countries, including the United Kingdom, South Africa, and Zimbabwe, among others. Each agreement allocates taxing rights between the two contracting states, which typically reduces or eliminates withholding taxes on dividends, interest, and royalties paid between treaty partners. For a foreign-owned entity repatriating profits, that reduction directly affects net returns.

Treaty relief is generally available to residents of the contracting states, so structuring your business correctly under Malawian law is a prerequisite for accessing reduced rates.

A company incorporated in Malawi and owned by a UK-resident parent could, under the Malawi-UK tax treaty, pay dividends to the parent at a reduced withholding rate rather than the standard domestic rate, meaningfully increasing the after-tax amount received in the UK.

Outside treaty countries, domestic relief provisions under the Taxation Act (Cap. 41:01) may still apply, offering unilateral credits for foreign taxes paid. This provides a baseline level of protection even where no bilateral treaty exists.

Available Incentives Through Malawi Investment and Trade Centre

The Malawi Investment and Trade Centre (MITC) serves as the government's primary interface for investors, administering a range of incentives that reduce the cost and risk of establishing operations in the country. These incentives are grounded in the Investment and Export Promotion Act, which provides the legal basis for MITC's mandate.

Registered investors can access the following incentives through MITC:

- Duty-free importation of capital equipment and machinery for qualifying investment projects

- Access to the Malawi Special Economic Zones, where additional fiscal concessions may apply

- Investment certificates that formally recognise your business and facilitate dealings with other government agencies

- Facilitated work and residence permit processing for foreign investors and key personnel

Securing an investment certificate through MITC grants your firm a degree of institutional recognition that can simplify regulatory interactions across multiple government bodies. For businesses importing specialised equipment, duty exemptions directly reduce capital expenditure at the setup stage, which matters most when cash flow is tightest.

MITC also coordinates with sector-specific regulators, reducing the burden of navigating multiple agencies independently.

Incentive eligibility under MITC is typically tied to minimum investment thresholds and sector classifications, so confirm your project qualifies before factoring these benefits into your financial projections.

Relatively Low Operating and Labour Costs

The low operating costs Malawi business advantage begins with wages. Average formal sector wages remain among the lower tiers across sub-Saharan Africa, meaning your payroll expenditure stretches further here than in more industrialised regional economies. For labour-intensive operations, that differential has a direct effect on unit cost structures.

Wage Levels and the Employment Act

Employment relationships are governed by the Employment Act (Cap. 55:02), which sets out minimum wage thresholds, working hour limits, and termination procedures. The statutory minimum wage applies across sectors, though specific rates are periodically reviewed by the government. Because the minimums are set at levels consistent with the country's income profile, businesses in manufacturing, agro-processing, and services can maintain leaner cost bases without deviating from statutory requirements.

Office and Facility Costs

Commercial real estate in cities such as Blantyre and Lilongwe remains significantly more affordable per square metre than in comparable regional hubs like Nairobi or Lusaka. Leasing industrial or warehouse space outside the central business districts reduces overhead further, which is a practical consideration for firms establishing physical operations rather than purely holding structures.

Utility and Infrastructure Costs

Electricity is supplied primarily through the Electricity Supply Corporation of Malawi (ESCOM), and tariff rates for commercial consumers are generally lower than the regional average. For energy-dependent production facilities, this translates to a measurable reduction in recurring operational expenditure compared to more infrastructure-developed markets.

How Malawi Stacks Up Against Regional Competitors

Businesses evaluating Malawi vs regional competitors for business advantages often weigh the same core variables: incorporation costs, tax treatment, treaty access, and market connectivity. The jurisdictions most relevant to this comparison are Zambia, Mozambique, and Zimbabwe — all geographically proximate, all targeting similar foreign investor profiles, and all members of overlapping regional trade blocs. What the comparison reveals is not that one jurisdiction dominates across every metric, but that Malawi holds a distinct position on several structural factors that matter most during the setup and early operational phase of a foreign-owned entity.

Corporate tax policy and registration accessibility are where the difference becomes most practical. Zambia's standard corporate tax rate sits at 30%, Zimbabwe's at 25%, and Mozambique's at 32% — all higher than Malawi's 30% headline rate, which can reduce further under sector-specific incentives administered through the Malawi Investment and Trade Centre. For businesses that qualify under the Companies Act 2013 as private limited companies, the registration process through the Companies Registry is entirely online, removing the procedural friction that remains common in several neighbouring systems.

| Parameter | Malawi | Zambia | Mozambique | Zimbabwe |

|---|---|---|---|---|

| Standard Corporate Tax Rate | 30% | 30% | 32% | 25% |

| COMESA Membership | Yes | Yes | No | Yes |

| SADC Membership | Yes | Yes | Yes | Yes |

| Online Company Registration | Yes | Partial | Partial | Partial |

| Investment Protection Legislation | Yes | Yes | Yes | Yes |

| Minimum Share Capital (Foreign Entity) | None mandated | None mandated | Required | Required |

Compliance Services for Companies in Malawi

Stay current with Malawi's regulatory and filing obligations, including annual returns, tax registration, and ongoing statutory requirements under the Companies Act 2013.

Conclusion

Incorporating in Malawi offers a coherent set of structural advantages that hold up under practical scrutiny. The corporate tax rate of 30% for resident companies, combined with the double taxation agreements that reduce withholding obligations on cross-border income, directly lowers the effective cost of operating from this jurisdiction. Access to preferential trade terms under both SADC and COMESA means your goods can move across a substantial regional market without the tariff burden that applies to non-member competitors.

The Companies Act 2013 provides a clear legal framework for registration, and the Malawi Investment and Trade Centre consolidates sector-specific incentives that reduce early-stage costs for qualifying businesses. These are not minor conveniences — they represent measurable reductions in capital outlay and administrative friction for a foreign-owned entity getting established.

That said, the fit depends on your industry, your intended markets, and how your group structure interacts with local ownership and tax residency rules. A business oriented toward regional trade will find the SADC and COMESA positioning particularly relevant. One focused on domestic consumer activity will weigh the growing middle-income population and the relatively low labour costs differently. The path forward from due diligence to an operational, compliant Malawian company requires precise execution at each stage of the formation and licensing process.

Start Your Malawi Company Formation With Expanship Today

Malawi company formation with Expanship covers the full incorporation cycle, from preparing and legalising your constituent documents under the Companies Act 2013, to filing with the Registrar General and meeting the ongoing compliance obligations administered by the Malawi Revenue Authority. The entity types, tax positions, and investment protections examined throughout this blog each carry specific procedural and regulatory requirements that Expanship manages on your behalf.

Expanship's services across the Malawi engagement include:

- Preparation and notarisation of incorporation documents, including the memorandum and articles of association

- Registered office and resident agent provision to satisfy statutory address requirements

- Filing with the Registrar General and liaison with the Malawi Revenue Authority for tax registration

- Post-incorporation compliance management, covering annual returns and director obligations

- Banking introduction assistance to support account opening with local or regional financial institutions

- Coordination with the Malawi Investment and Trade Centre for applicable incentive applications

Engaging a specialist reduces the administrative burden of coordinating across multiple government bodies, each with their own timelines, documentation standards, and fee structures. For a foreign entity without a local presence, that coordination is not a minor inconvenience; it directly affects how quickly your business becomes operational and compliant.

To discuss your incorporation requirements, contact Expanship Malawi directly.

Frequently Asked Questions (FAQ)

The standard corporate income tax rate administered by the Malawi Revenue Authority is 30% for resident companies. Businesses operating in qualifying sectors or special economic zones may be eligible for reduced rates or tax holidays under incentive frameworks administered through the Malawi Investment and Trade Centre. The applicable rate can vary depending on the nature and location of business activities.

Registration timelines under the Companies Act 2013 vary, but the process is generally completed within a few business days once all required documentation has been submitted to the Registrar of Companies. Delays can occur if submitted documents are incomplete or require additional verification. Engaging a local registered agent can help keep the process on schedule.

Malawi has entered into double taxation agreements with a number of countries, which can reduce withholding tax obligations on dividends, interest, and royalties paid across borders. The specific relief available depends on the treaty in force between Malawi and the investor's home country. Businesses should confirm treaty coverage with the Malawi Revenue Authority or a qualified tax adviser before structuring cross-border payments.

Foreign investors benefit from protections under the Malawi Investment and Trade Centre Act and broader investment promotion legislation, which address matters such as repatriation of profits and protection against expropriation without compensation. These frameworks are designed to provide a degree of legal certainty for foreign-owned entities. Additional protections may be available under bilateral investment treaties to which Malawi is a party.

Malawi's company registration fees and general operating costs are comparatively lower than several regional peers, though direct comparisons depend on the specific jurisdictions being evaluated and the sector involved. Labour costs in Malawi are among the lower in the SADC region, which can reduce overhead for labour-intensive operations. Tax treaty access, COMESA membership, and incentive availability also factor into a meaningful cost-benefit comparison.

A registered office address within Malawi is a requirement under the Companies Act 2013 for all incorporated entities. While the Act does not universally mandate a locally resident director for private companies, having at least one director with an understanding of local compliance obligations is advisable given the reporting requirements under Malawian law. Specific requirements should be confirmed at the time of incorporation, as regulatory practice can evolve.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.