Key Takeaways

- Under the Canada Business Corporations Act (CBCA), at least one-quarter of a corporation's directors must be resident Canadians, a structural constraint that foreign-owned entities must account for before filing an incorporation application.

- Corporations incorporated federally or in most provinces are required to maintain a register of individuals with significant control (ISC) at the corporate level, which must be made available to Corporations Canada or the relevant provincial authority upon request.

- The choice between federal incorporation under the CBCA and provincial incorporation under legislation such as the Ontario Business Corporations Act or the British Columbia Business Corporations Act determines which residency, naming, and compliance rules apply to the entity.

- Entity type, industry classification, and the residency profile of directors and shareholders all affect which specific requirements a corporation must satisfy, meaning there is no single universal checklist that applies to every Canadian incorporation.

Incorporation requirements in Canada are governed primarily by the Canada Business Corporations Act (CBCA), administered by Corporations Canada under Innovation, Science and Economic Development Canada. Businesses may also incorporate provincially under legislation such as the Ontario Business Corporations Act or the British Columbia Business Corporations Act, depending on the intended scope of operations.

This article covers the structural, documentary, and compliance requirements that apply to the incorporation process under federal and provincial frameworks.

Failure to satisfy these requirements results in rejection of the incorporation application or, where an entity operates without proper registration, exposure to penalties under applicable legislation.

Requirements vary depending on the entity type selected, the industry in which the business operates, and the residency profile of its directors and shareholders.

Foreign entrepreneurs, non-resident investors, and international firms seeking a Canadian legal presence will find this article directly relevant to their planning process.

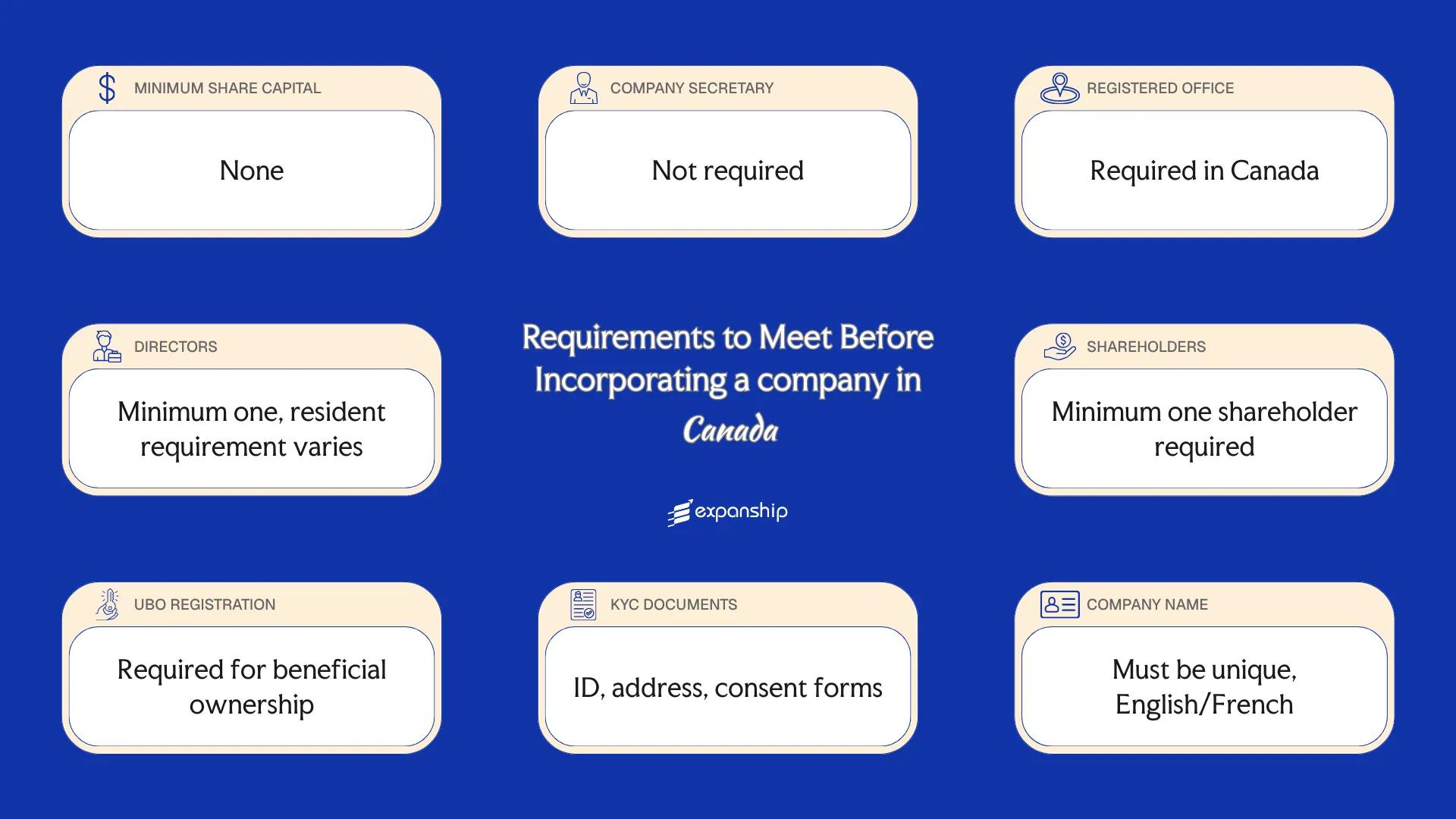

Minimum Share Capital Requirements in Canada

Under the Canada Business Corporations Act (CBCA), there are no minimum share capital requirements in Canada for federally incorporated companies. Corporations Canada, the federal registry under Innovation, Science and Economic Development Canada, does not require proof of capital deposit at the time of incorporation.

All shares issued under the CBCA are no-par value shares, meaning there is no assigned face value attached to each share. The amount received by the corporation upon issuance is credited to the stated capital account maintained for that class of shares.

| Parameter | Detail |

|---|---|

| Minimum Authorized Share Capital | No statutory requirement |

| Maximum Authorized Share Capital | No statutory requirement |

| Minimum Paid-Up Capital | No statutory requirement |

| Paid-Up Requirement at Incorporation | No statutory requirement |

| Accepted Currency | Canadian Dollar (CAD); foreign currencies permissible |

| Accepted Forms of Contribution | Cash, property, or past services |

| Timeframe to Deposit Capital | No statutory deadline |

A corporation still requires at least one issued share to have a valid shareholder. Incorporating without issuing any shares leaves the company without a legal owner of record, which can create compliance issues down the line.

Company Secretary Requirements in Canada

Under the Canada Business Corporations Act (CBCA), appointing a corporate secretary is not a statutory requirement for federally incorporated companies. Provincial legislation varies, though most provinces similarly treat the role as optional rather than mandatory. Your company secretary requirements Canada compliance posture will depend on whether your governing corporate statute or internal bylaws impose the position.

Where a corporate secretary is appointed, their responsibilities typically include maintaining the corporate minute book, recording resolutions, and ensuring that statutory registers reflect current officer and director information.

Qualification criteria for serving as a corporate secretary under the CBCA and most provincial regimes:

- No residency requirement applies; the secretary may be ordinarily resident outside Canada.

- Both individuals and, in some jurisdictions, corporate entities may hold the position.

- No licensing or professional designation is mandated by federal statute.

- A director of the same corporation may simultaneously serve as corporate secretary.

- No minimum age is prescribed beyond general legal capacity to act.

Incorporate a Company in Canada

Set up your Canadian corporation under the CBCA or a provincial statute, with guidance on structure, filings, and ongoing compliance obligations.

Registered Office Requirements in Canada

Registered office requirements in Canada apply to both federally incorporated entities under the Canada Business Corporations Act (CBCA) and provincially incorporated companies under their respective corporate statutes. Non-compliance with address obligations can result in administrative dissolution or the rejection of official notices served to the corporation.

- A physical street address is required; a post office box alone does not satisfy the registered office requirement under the CBCA or provincial equivalents.

- Virtual office addresses are generally permitted provided they include a physical civic address where documents can be received and the corporation can be reached.

- Federal corporations under the CBCA must maintain their registered office in the Canadian province or territory specified in their articles of incorporation.

- No ownership of the premises is required; a lease or service agreement confirming use of the address is sufficient.

- The registered office address is publicly listed on Corporations Canada's database for federal entities, making it accessible to third parties and government authorities.

- Any change to the registered office address must be filed with Corporations Canada using the prescribed form, or with the relevant provincial registry for provincially incorporated firms, and takes effect upon filing.

Director Requirements in Canada

Under the Canada Business Corporations Act (CBCA), director requirements Canada incorporation rules establish that directors assume personal liability for specific statutory obligations, including unpaid wages owed to employees for up to six months and unremitted source deductions under the Income Tax Act. Upon appointment, each director becomes bound by fiduciary duties to act honestly, in good faith, and in the best interests of the corporation.

| Parameter | Detail |

|---|---|

| Minimum Number of Directors | One director is required for a private corporation; publicly distributing corporations require a minimum of three directors. |

| Maximum Number of Directors | No statutory maximum, though the number must align with what is specified in the articles of incorporation. |

| Local/Resident Director Required | Under the CBCA, at least 25% of directors must be resident Canadians; corporations with fewer than four directors must have at least one resident Canadian director. |

| Nationality Restrictions | No nationality restrictions apply, though residency-based requirements under the CBCA indirectly affect composition for federally incorporated entities. |

| Minimum Age Requirement | Directors must be at least 18 years of age. |

| Corporate Directors Permitted | Corporate directors are not permitted; only individuals may serve as directors under the CBCA. |

| Director Must Be a Shareholder | No statutory requirement for a director to hold shares in the corporation. |

| Publicly Listed on Registry | Director information is filed with Corporations Canada and is accessible through the federal corporate registry. |

| Disqualification Conditions | A person is disqualified if they are under 18, are of unsound mind as determined by a court, have the status of a bankrupt, or do not meet the residency quota requirements. |

Several Canadian provinces, including British Columbia and Alberta, have eliminated the resident Canadian director requirement entirely under their own provincial corporate statutes, meaning a corporation incorporated provincially rather than federally can have an all-foreign board with no residency obligations.

Shareholder Requirements in Canada

Under the Canada Business Corporations Act (CBCA), a corporation requires at least one shareholder. No statutory maximum applies, meaning the structure scales from a single-shareholder entity to a broadly held public company.

Nationality and Residency Restrictions

Shareholders face no residency or citizenship requirements under the CBCA. Foreign nationals and non-resident entities may hold shares without restriction on ownership percentage.

Corporate Shareholders

Corporate entities are permitted to act as shareholders in a Canadian corporation. No special conditions are imposed solely by virtue of the shareholder being a legal entity rather than an individual.

Shareholder Liability

Liability is limited to the amount paid or outstanding on each shareholder's shares. Piercing the corporate veil remains an exceptional judicial remedy, applied only where a court finds the corporate structure was used to perpetrate fraud or serious wrongdoing.

Register of Shareholders

The CBCA requires every corporation to maintain a register of shareholders at its registered office or designated records location. This register is not publicly accessible, though it must be available for inspection by shareholders and creditors upon request.

Set Up Your Canadian Corporation With Confidence

Get tailored guidance on shareholder structuring and ownership compliance when incorporating in Canada.

UBO / Beneficial Ownership Reporting Requirements in Canada

Under the Canada Business Corporations Act (CBCA) and equivalent provincial statutes, a beneficial owner is any individual who directly or indirectly owns or controls 25% or more of a corporation's shares or voting rights.

- Identify all individuals meeting the 25% ownership or control threshold and record them in the corporation's internal register of individuals with significant control (ISC).

- Maintain the ISC register at the corporation's registered office or another prescribed location.

- File ISC information annually with Corporations Canada through the Annual Return for federally incorporated entities.

- Update the register within 15 days of becoming aware of any change in beneficial ownership.

| Parameter | Detail |

|---|---|

| Ownership Threshold for UBO Status | 25% of shares or voting rights, or significant influence or control |

| Filing Authority | Corporations Canada (federal); provincial registrars for provincially incorporated entities |

| Disclosure Deadline at Incorporation | Register must be established upon incorporation |

| Publicly Accessible Register | No statutory requirement for public access at the federal level |

| Penalties for Non-Disclosure | Fines up to CAD 200,000 and possible imprisonment under the CBCA |

| Ongoing Update Obligation | Within 15 days of any known change |

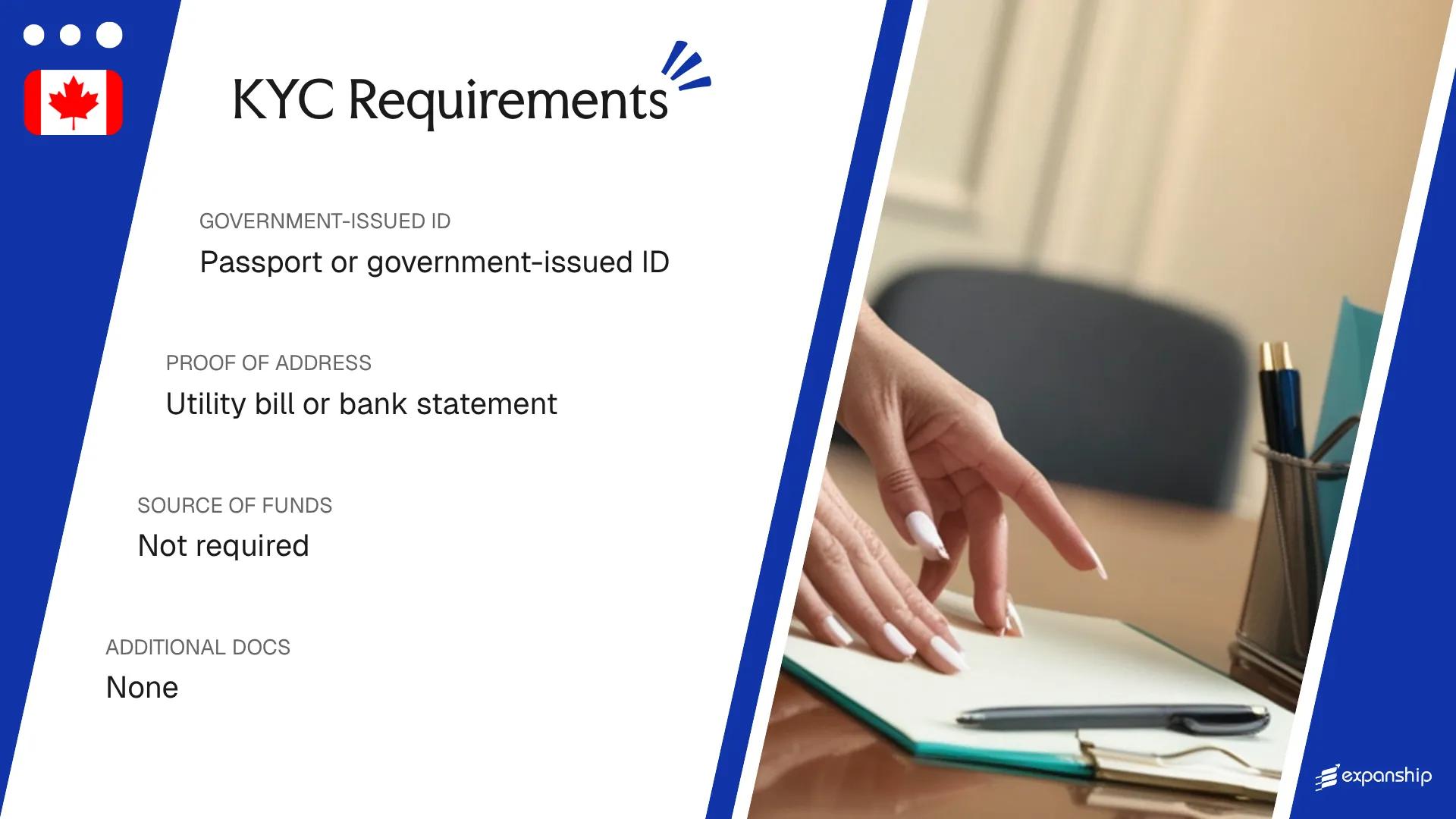

KYC / Document Requirements in Canada

KYC document requirements Canada company incorporations fall under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act, administered by FINTRAC, which sets out identity verification obligations applicable to regulated intermediaries involved in entity formation.

Individual / Personal Documents

- Government-issued photo identification (passport or national identity card) for each director and individual shareholder

- Proof of residential address dated within 90 days, such as a utility bill or bank statement

- Completed and signed director consent form where required by the incorporating jurisdiction

- Social Insurance Number or equivalent tax identification number may be requested by the registered agent

Corporate Documents

- Certificate of incorporation or equivalent constitutional document for any corporate shareholder or director

- Articles of association or by-laws confirming the entity's internal governance structure

- Register of directors confirming current officeholders of the corporate entity

- Proof of registered address for the corporate entity, such as a utility bill or official correspondence

Source of Funds Documentation

- Recent bank statements (typically the last three to six months) evidencing the origin of invested capital

- Audited financial statements where the investing entity is an established business

- Written declaration of source of funds where bank documentation is unavailable

Notarisation and Apostille Requirements

- Foreign-issued identity documents may require notarisation by a qualified notary public

- Canada is not a party to the Hague Apostille Convention, so foreign public documents may require consular legalisation instead

- Official translations into English or French must accompany documents issued in other languages

Incomplete or unverified proof of residential address for individual directors is the most frequent cause of incorporation filing delays in Canada.

Company Name Requirements in Canada

Proposed company name requirements Canada must be assessed before incorporation is approved. A name search report, known as a NUANS report, is required to confirm the proposed name does not conflict with existing corporate or trademark registrations.

Names must end with a legal element such as "Limited," "Incorporated," or "Corporation," or their French equivalents or abbreviations. Bilingual names combining both English and French forms are permitted.

Certain words are prohibited outright or require prior consent from the relevant federal authority. Terms suggesting a connection to the Crown, a government body, or a regulated profession fall into this category.

Name reservation is available and can be secured through a NUANS search. The reservation remains valid for 90 days from the date the report is issued, during which your proposed name is held against conflicting registrations.

Corporate Compliance Services for Companies in Canada

Ongoing compliance obligations for Canadian corporations include annual returns, director updates, and registered office maintenance. Our team manages these requirements on your behalf.

Conclusion

Meeting Canada corporation compliance requirements involves a defined set of obligations under the Canada Business Corporations Act and applicable provincial statutes. Residency requirements for directors remain one of the more structurally significant obligations for foreign-owned entities, as at least one-quarter of directors must be resident Canadians. The register of individuals with significant control, maintained at the corporate level and accessible to Corporations Canada or provincial equivalents upon request, adds a layer of ongoing disclosure that extends beyond initial formation. Once these requirements are understood, the practical focus shifts to structuring ownership, appointing qualified directors, and maintaining statutory records in good standing.

Expanship's Corporate Services for Canada Expansion

Expanship's Canada company incorporation services are built around the specific requirements that federal and provincial frameworks impose, from CBCA director residency conditions to ISC beneficial ownership filings. Our role is to reduce the administrative load these obligations place on your team, not to sidestep them.

We support businesses at every stage of the incorporation and compliance cycle in Canada. Our services include:

- Preparing and filing incorporation documents with Corporations Canada or the relevant provincial registry on your behalf.

- Providing a registered office address and resident Canadian director solutions where required.

- Handling government filings and liaising directly with regulatory bodies, including the CRA, throughout the process.

- Managing ongoing compliance obligations after your entity is incorporated and active.

- Facilitating introductions to Canadian banking institutions suited to your business structure.

- Coordinating GST/HST registration and local tax authority requirements as your operations take shape.

To discuss your requirements, contact Expanship Canada.

Frequently Asked Questions (FAQ)

Under the CBCA, if a corporation has fewer than four directors, at least one must be a Canadian resident. The 25% threshold is effectively replaced by this minimum-one rule at smaller board sizes. This distinction matters when structuring a lean board, since the residency obligation cannot be avoided simply by limiting the number of directors.

Failure to maintain a valid registered office as required under the CBCA or applicable provincial legislation can result in the corporation being struck from the register or losing its certificate of incorporation. The registered office must be a physical address in the jurisdiction of incorporation, not a P.O. box, and must be kept current with Corporations Canada or the relevant provincial registry. Failing to update this address following a change is treated as a compliance breach.

Private corporations incorporated under the CBCA are required to maintain a register of individuals with significant control (ISC), defined as those holding 25% or more of voting shares or voting rights. As of amendments enacted in 2023, this information must be filed with Corporations Canada, though the public accessibility of the federal register remains more limited than some other jurisdictions. Provincially incorporated entities are subject to separate beneficial ownership rules that vary by province.

No minimum paid-up share capital is required to incorporate under the CBCA. A corporation can be formed with a single share issued at a nominal value, giving you flexibility in how you structure the initial capitalization. This also means there is no statutory deposit or proof-of-capital requirement as part of the federal registration process.

Directors of a Canadian corporation must be individuals; a corporate entity cannot hold a directorship. Under the CBCA, directors must also be at least 18 years of age, not bankrupt, and not been found to be of unsound mind by a court. These personal eligibility criteria apply regardless of whether the director is a Canadian resident or a foreign national.

Before a federal corporation can be registered under the CBCA, a NUANS (Newly Upgraded Automated Name Search) report must be obtained to confirm the proposed name does not conflict with existing corporate names, trademarks, or trade names. If the NUANS report identifies a conflict, Corporations Canada will reject the name and require a revised submission. The NUANS report is valid for 90 days from the date of issue, so registration must be completed within that window.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.