Key Takeaways

- Foreign investors incorporating federally under the Canada Business Corporations Act (CBCA) face mandatory resident director requirements, meaning at least 25% of a corporation's directors must be Canadian residents — a structural constraint that limits governance flexibility for non-resident owners.

- Canada's layered federal and provincial tax system imposes a combined corporate tax rate that can exceed 26% depending on the province, creating a heavier fiscal burden than many comparable incorporation jurisdictions.

- Businesses operating across multiple provinces must satisfy dual compliance obligations — including separate registration, filing, and fee requirements at both the federal and provincial levels — significantly increasing administrative overhead.

- Companies supplying taxable goods or services above the $30,000 CAD annual revenue threshold are required to register for GST/HST and manage remittance obligations that vary in rate and structure across participating provinces, adding recurring regulatory complexity.

Canada operates under a heavily regulated corporate framework, administered at both the federal and provincial levels. Understanding the disadvantages of incorporating in Canada requires examining a broad set of compliance, structural, and operational obligations that affect foreign investors differently than domestic ones.

The drawbacks of Canada incorporation span tax, governance, disclosure, and sector-specific restrictions — each addressed separately in the sections that follow. How significantly these affect your business depends on its structure, the province of registration, and the industry it operates in.

The Canada Business Corporations Act (CBCA) governs federally incorporated entities, though provincial statutes apply if you register at that level instead. The cons of registering a company here are most relevant to non-resident entrepreneurs, foreign-owned holding structures, and international firms entering regulated sectors for the first time.

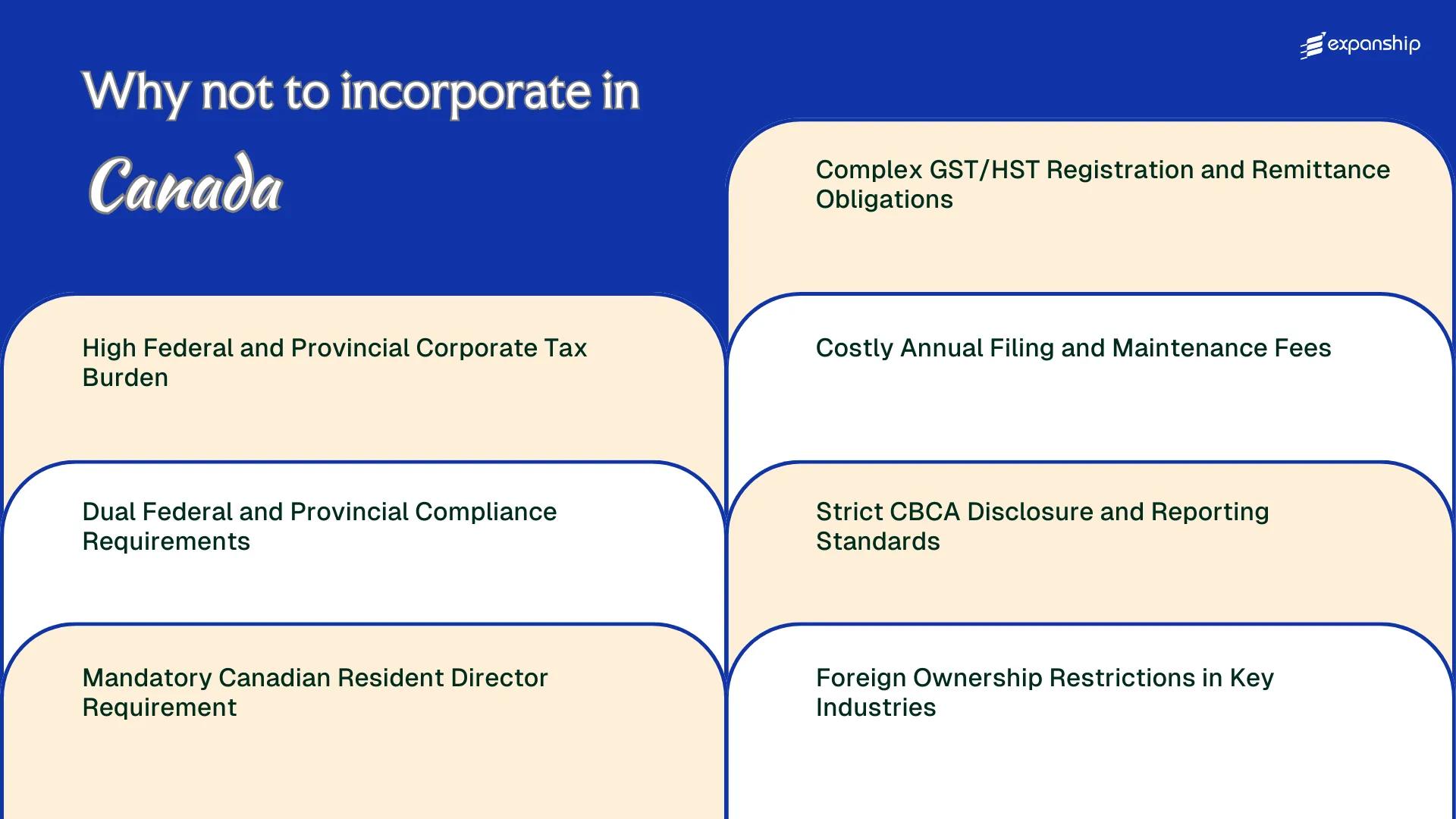

High Federal and Provincial Corporate Tax Burden

Canada corporate tax burden disadvantages are felt most acutely when you account for the layered structure of federal and provincial rates operating simultaneously. Unlike single-tier tax systems, your firm faces two separate tax authorities with independent rate-setting powers.

Combined Federal and Provincial Rate Exposure

The federal corporate income tax rate sits at 15% for general corporations after the federal abatement, but each province and territory adds its own layer on top. Ontario levies an 11.5% general provincial rate, while British Columbia charges 12%, pushing combined rates past 26% in major business hubs.

For a foreign-owned entity without access to the Small Business Deduction, which phases out based on passive income and associated corporation rules under the Income Tax Act, the full general rate applies from the outset.

Passive Income Thresholds and Tax Integration Costs

Under federal rules, earning over $50,000 in passive investment income annually begins to erode a Canadian-controlled private corporation's access to the small business rate, compressing tax planning options. For foreign-controlled corporations, this threshold is structurally irrelevant since they don't qualify for the small business rate at all, meaning the effective combined rate ceiling is the default position.

Provincial tax compliance also requires separate filings in each province where your business has a permanent establishment, multiplying administrative costs across jurisdictions.

A foreign-controlled corporation incorporated in Canada is taxed at the full combined federal-provincial rate with no access to preferential small business rates, making pre-incorporation profit modeling against the actual applicable rate essential.

Dual Federal and Provincial Compliance Requirements

Dual compliance requirements in Canada corporations face stem from a structural feature of the country's legal system: federal and provincial governments each impose their own distinct corporate obligations. Incorporating under the Canada Business Corporations Act (CBCA) does not exempt your business from provincial registration requirements in every province where it carries on business.

Most provinces, including Ontario, British Columbia, and Alberta, require a separately registered extra-provincial or provincial license for federally incorporated entities operating within their borders. Each registration triggers its own filing deadlines, fees, and annual return obligations, multiplying the administrative burden across jurisdictions.

For a foreign business owner, this creates friction in several concrete ways:

- Maintaining separate registered agents or addresses in multiple provinces increases your ongoing operational costs.

- Missing a provincial annual return in one jurisdiction can result in dissolution or loss of good standing, even if your federal CBCA filings are current.

- Changes to your corporate structure, such as a director update, must be reported to Corporations Canada and to each relevant provincial registry separately.

- Provincial regulators like Ontario's ServiceOntario and BC Registry Services operate on their own timelines and fee schedules, requiring you to track multiple compliance calendars simultaneously.

Businesses operating in only one province and incorporating provincially rather than federally can avoid some of this layering, but federally incorporated entities with multi-province operations have no mechanism to consolidate these filings into a single submission.

Company Incorporation in Canada

Incorporate your business in Canada with full support for both federal CBCA registration and provincial compliance requirements across all active jurisdictions.

Mandatory Canadian Resident Director Requirement

One of the more operationally inconvenient Canada resident director requirement drawbacks is the statutory obligation under the Canada Business Corporations Act (CBCA). Under the CBCA, at least 25% of a corporation's directors must be resident Canadians. For a board of fewer than four directors, at least one must meet this residency threshold. If your business operates entirely outside the country with no local personnel, this requirement forces you to recruit, compensate, and trust an individual you may have no prior relationship with.

| Board Size | Minimum Canadian Resident Directors Required | Non-Resident Control Risk |

|---|---|---|

| 1 director | 1 (100% must be Canadian resident) | Foreign owner cannot sole-direct |

| 2 directors | 1 (50% must be Canadian resident) | Significant veto exposure |

| 3 directors | 1 (33% must be Canadian resident) | Outsider holds board seat |

| 4+ directors | 25% must be Canadian resident | Ongoing recruitment burden |

A resident director carries legal authority. That person has signing power and fiduciary duties that intersect with your business decisions, introducing an external party into governance from day one.

Nominee director service providers exist, but they carry fees and introduce counterparty risk that a purely foreign-owned structure would otherwise avoid. Provinces incorporated under provincial acts, such as Ontario's Business Corporations Act (OBCA), impose similar residency rules, meaning the constraint persists regardless of the incorporating statute your firm selects.

Complex GST/HST Registration and Remittance Obligations

Canada GST HST registration challenges begin the moment your business exceeds the $30,000 CAD small supplier threshold in any single calendar quarter or over four consecutive quarters. At that point, registration with the Canada Revenue Agency (CRA) under the Excise Tax Act becomes mandatory, regardless of where your company is incorporated.

The structure itself adds friction. Provinces that have not harmonized with the federal GST operate separate provincial sales tax (PST) regimes, meaning a business selling across multiple provinces faces distinct registration and filing obligations under different provincial authorities.

Reporting periods are assigned by the CRA based on annual taxable supplies, and missing a remittance deadline triggers interest charges and penalties. For a foreign-owned entity without local finance staff, tracking input tax credits, filing deadlines, and province-specific rules creates a recurring administrative burden with direct cost implications.

- Registration is mandatory once taxable supplies exceed $30,000 CAD in a qualifying period under the Excise Tax Act

- Provinces such as British Columbia, Saskatchewan, and Manitoba impose separate PST obligations outside the HST framework

- Reporting frequency (monthly, quarterly, or annual) is determined by the CRA, not elected freely by the business

- Input tax credit claims require documentation that meets CRA evidentiary standards; incomplete records result in disallowed credits

- Non-resident businesses supplying digital services to Canadian consumers face GST/HST registration obligations under rules introduced in 2021

A non-resident business with no physical presence in Canada can still be legally required to collect and remit GST/HST solely because its digital services are consumed by Canadian users.

Costly Annual Filing and Maintenance Fees

Maintaining a corporation registered under the Canada Business Corporations Act or a provincial equivalent generates recurring costs that accumulate well beyond the initial setup, making Canada annual filing fees disadvantages a practical concern for foreign operators managing lean budgets.

Annual Return Obligations Across Registries

Federal corporations must file an annual return with Corporations Canada, while provincial registrations require separate filings with each province's corporate registry, such as the Ontario Business Registry or BC Registry Services. Each filing carries its own fee, and missing a deadline can trigger dissolution proceedings, forcing you to absorb reinstatement costs on top of the original arrears.

Compounding Administrative Costs for Foreign-Held Entities

Corporate upkeep expenses extend beyond government fees to include mandatory registered agent services, which foreign-owned firms must retain because they lack a domestic address for service of process. If your entity operates across multiple provinces, the costs multiply with each jurisdiction, since there is no consolidated national maintenance mechanism that satisfies all provincial requirements simultaneously.

Support for Managing Corporate Compliance Costs in Canada

Expanship helps foreign business owners understand the full scope of annual filing obligations and maintenance requirements before and after incorporation in Canada.

Strict CBCA Disclosure and Reporting Standards

CBCA disclosure requirements drawbacks extend beyond annual returns, creating a multi-layered reporting structure that foreign-incorporated businesses often underestimate. Under the Canada Business Corporations Act, corporations face obligations that carry real administrative cost and legal exposure.

- Corporations registered under the CBCA must maintain and file a register of individuals with significant control (ISC), disclosing the identity of anyone holding 25% or more of voting shares or shares by fair market value, exposing ownership structures that many foreign principals prefer to keep private.

- The Canadian corporate transparency obligations under the ISC register require updates within 15 days of any change, making dynamic ownership structures operationally burdensome.

- Failure to maintain an accurate ISC register carries penalties under the CBCA, placing direct legal liability on directors, including any resident Canadian director your firm appoints.

- Publicly accessible director information filed with Corporations Canada creates reputational and security considerations for foreign principals unaccustomed to this level of statutory exposure.

Foreign Ownership Restrictions in Key Industries

Canada foreign ownership restrictions in industries such as telecommunications, broadcasting, and financial services are codified across multiple federal statutes, not left to regulatory discretion. This creates hard legal ceilings that foreign investors cannot negotiate around, regardless of capital commitment or business structure.

Under the Telecommunications Act and the Broadcasting Act, non-Canadian entities face equity caps that directly limit control. A foreign corporation cannot hold more than 20% of voting shares in a facilities-based carrier, effectively barring majority ownership in that sector.

The Investment Canada Act imposes a net benefit review on foreign acquisitions above prescribed thresholds, with certain cultural businesses subject to outright ministerial approval. Failing to satisfy the net benefit test can result in a transaction being blocked or unwound.

Restricted sectors include:

- Telecommunications carriers

- Broadcasting and media companies

- Domestic air transport

- Uranium mining

- Financial institutions (banks, insurance)

A foreign investor seeking to acquire a mid-sized Canadian telecom carrier would be legally prohibited from holding majority voting control under Section 16 of the Telecommunications Act, regardless of the acquisition price or proposed operational model.

Overcoming These Incorporation Challenges

Overcoming these incorporation challenges requires structural decisions made before and during the registration process, not adjustments made after problems emerge.

- Appoint a qualifying Canadian resident director at the time of federal incorporation under the Canada Business Corporations Act to satisfy the CBCA's residency thresholds from the outset.

- Select a provincial jurisdiction, such as British Columbia or Alberta, that imposes no resident director requirement, reducing the compliance burden for foreign-owned entities.

- Register for GST/HST with the Canada Revenue Agency once taxable supplies meet or are expected to meet the $30,000 CAD threshold across four consecutive calendar quarters.

- File annual returns and maintain a registered office address to satisfy both federal and applicable provincial corporate registries.

- Review federal foreign ownership restrictions under sector-specific statutes before structuring your shareholding, particularly in broadcasting, telecommunications, and financial services.

Overcoming Canada incorporation challenges does not eliminate the underlying regulatory obligations. The solutions available operate within a tightly administered dual federal-provincial framework, and managing Canadian compliance requirements remains an ongoing obligation rather than a one-time exercise.

Canada's Value as a Business Destination

Canada remains a credible incorporation destination despite the drawbacks examined in this blog. Its stable legal system under the Canada Business Corporations Act, treaty network, and access to North American markets give it a grounded appeal for foreign businesses that can absorb its structural demands.

| Pros | Cons |

|---|---|

| Canada's tax treaty network reduces withholding tax exposure for cross-border structures. | Federal and provincial corporate taxes stack, producing a combined rate that exceeds many competing jurisdictions. |

| The CBCA provides a well-established, predictable statutory framework for corporate governance. | Dual federal and provincial compliance creates parallel reporting obligations that increase administrative overhead. |

| Incorporation grants access to one of the world's largest trading relationships through CUSMA. | At least one director must be a Canadian resident, limiting governance flexibility for fully foreign-owned entities. |

| Canada's banking infrastructure is stable and widely accessible to incorporated entities. | GST/HST registration and remittance obligations vary by province and threshold, adding compliance complexity. |

| Canadian corporations carry reputational weight in international trade relationships. | Restricted foreign ownership applies to sectors including telecommunications, broadcasting, and financial services. |

Meeting ongoing obligations, from CBCA disclosure filings to provincial annual returns, requires consistent attention throughout the life of your corporation.

Corporate Compliance Services for Companies in Canada

Manage your ongoing federal and provincial compliance obligations, from annual returns and CBCA disclosure filings to GST/HST remittance requirements.

Conclusion

The disadvantages of incorporating in Canada are real and measurable. Resident director requirements under the Canada Business Corporations Act, layered federal-provincial tax obligations, and dual compliance filing across two regulatory tiers represent genuine structural costs for foreign businesses. These are not theoretical concerns — they affect timelines, operating budgets, and ownership flexibility. For businesses with the right structure and professional support in place, those costs become manageable.

Expanship's Canada Incorporation Support

Expanship's Canada incorporation support services are structured around the specific compliance demands that come with forming a corporation under the CBCA or a provincial equivalent. From satisfying Corporations Canada's documentary requirements to managing ongoing GST/HST remittance schedules and provincial filing obligations, the operational load is real. Expanship's role is to reduce that burden, particularly for foreign-founded businesses working through unfamiliar regulatory frameworks.

Beyond incorporation itself, Expanship offers a practical range of services to support your business through setup and beyond.

- Your company is registered with all required government documents prepared and filed correctly.

- A registered agent and Canadian office address are provided to meet statutory presence requirements.

- Your firm's filings and regulatory correspondence are handled directly with the relevant federal and provincial authorities.

- Post-incorporation compliance obligations are managed on an ongoing basis.

- Banking introduction assistance is available to help your business establish a Canadian financial footprint.

- Tax registration and liaison with the CRA and provincial tax authorities are coordinated on your behalf.

Reach out through Expanship Canada to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The requirement varies by province. British Columbia and Prince Edward Island have eliminated resident director requirements, while Ontario, Alberta, and Manitoba still impose them. Incorporating provincially in a jurisdiction without this rule is one way foreign investors reduce structural friction, though it shifts which corporate registry and compliance framework governs the entity.

Under the CBCA, failure to maintain a current register of individuals with significant control or to file annual returns with Corporations Canada can result in fines and, in serious cases, administrative dissolution of the corporation. Directors can face personal liability for certain omissions, particularly where disclosure of beneficial ownership is involved. The penalties are not theoretical; Corporations Canada actively flags non-compliant entities.

The direct tax cost depends on revenue, but the administrative burden is a fixed overhead regardless of size. Businesses must register with the Canada Revenue Agency once taxable supplies exceed CAD 30,000 in a calendar quarter or over four consecutive quarters, then file returns either monthly, quarterly, or annually depending on turnover. Errors in input tax credit claims frequently trigger audits, which generate professional fees that can far exceed the original remittance amounts.

Canada's combined federal and provincial corporate tax rate typically falls between 23% and 31%, depending on the province, which is broadly comparable to Australia but higher than the UK's 25% headline rate. Small Canadian-controlled private corporations benefit from the small business deduction, reducing federal tax to 9% on the first CAD 500,000 of active business income, but that relief phases out at higher income levels and is unavailable to foreign-controlled corporations. For internationally mobile businesses, the unavailability of that deduction is a material disadvantage.

Missing a provincial annual return deadline can trigger late filing fees and, if the delinquency continues, involuntary dissolution by the provincial registrar. A dissolved corporation loses its legal standing, cannot enter contracts, and may have its name made available for registration by another party. Restoration is possible but involves additional filings, fees, and in some provinces a court order, making prevention significantly less costly than remediation.

Partial mitigation through holding structures is sometimes possible but the core restrictions still apply at the operational level. The Telecommunications Act and the Bank Act impose Canadian ownership thresholds directly on licensed entities, not just on the immediate parent. Regulators such as the CRTC and OSFI examine the ultimate beneficial ownership chain, so a Canadian-incorporated holding company controlled by foreign nationals does not satisfy the residency or ownership conditions required to hold certain licences.

A federally incorporated business that operates in multiple provinces must register as an extra-provincial corporation in each province where it carries on business, triggering separate registration fees, annual filings, and in some cases provincial tax accounts. That means a single operating entity can face compliance obligations to Corporations Canada, the CRA, and up to ten provincial or territorial registries simultaneously. The cumulative filing and professional costs can be substantially higher than what a single-jurisdiction incorporation in a comparable country would require.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.