Key Takeaways

- Rwanda's business entities are governed under the Companies Act (2009, as amended) and registered through the Rwanda Development Board (RDB), which serves as the central authority for incorporation and investment facilitation.

- The Private Limited Company (Société à Responsabilité Limitée / SARL) is the most commonly registered entity type in Rwanda, favored by small and medium enterprises for its flexible shareholding structure and limited liability protection.

- Rwanda operates a territorial tax system, meaning corporate income tax applies only to income sourced within the country, a factor that directly influences entity selection for foreign investors.

- Foreign businesses requiring a direct operational presence in Rwanda without establishing a separate legal entity typically do so through a Branch Office rather than a subsidiary structure.

Introduction to Entity Types in Rwanda

Rwanda is a landlocked country in East Africa, bordered by Uganda, Tanzania, Burundi, and the Democratic Republic of the Congo. It is an independent republic and a member of both the East African Community and the Commonwealth. Businesses operating there register through the Rwanda Development Board (RDB), which serves as the central authority for company registration and investment facilitation.

The country operates a territorial tax system, meaning only income sourced within Rwanda is generally subject to corporate income tax.

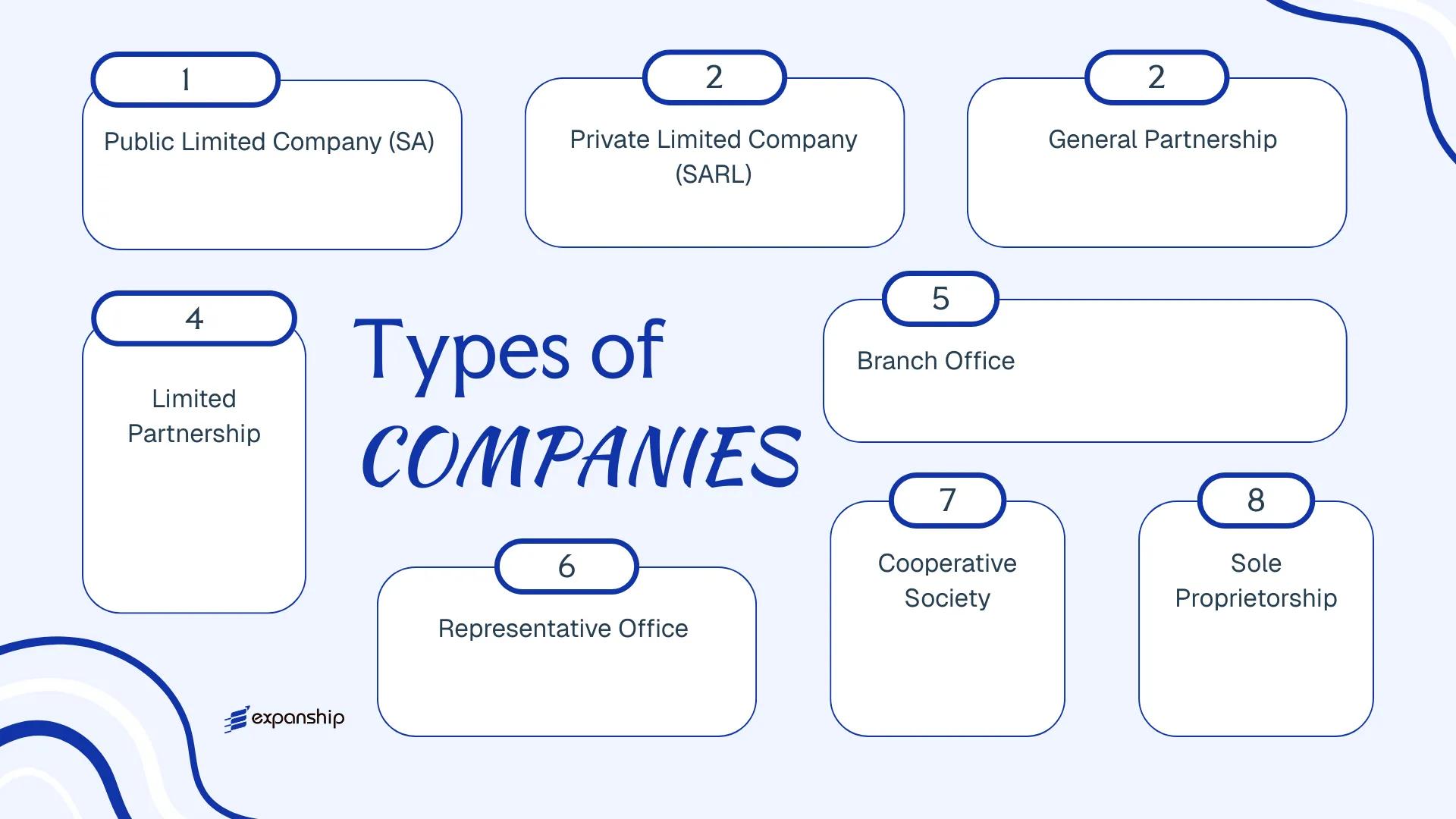

Available types of business entities in Rwanda include the Public Limited Company (Société Anonyme / SA), Private Limited Company (Société à Responsabilité Limitée / SARL), General Partnership (Société en Nom Collectif), Limited Partnership (Société en Commandite Simple), Branch Office, Representative Office, Cooperative Society, and Sole Proprietorship (Entreprise Individuelle). Each structure carries distinct implications for liability, ownership, governance, and tax treatment. This article examines each entity in turn, covering registration requirements, structural features, and the circumstances under which each form is commonly used.

An Overview of Business Structures in Rwanda

Rwanda's company law framework provides several distinct legal forms under which a business may be established and operated. The primary legislation governing these structures is the Law No. 17/2018 of 13/04/2018 governing companies in Rwanda, administered by the Rwanda Development Board (RDB), which serves as the central registration authority. Each legal form carries different implications for liability, ownership, governance, and tax treatment.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (SA) | Corporate | Limited to shares | Taxed | Yes | 2 shareholders | RDB | Law No. 17/2018 |

| Private Limited Company (SARL) | Corporate | Limited to shares | Taxed | Yes | 1 shareholder | RDB | Law No. 17/2018 |

| General Partnership (SNC) | Partnership | Unlimited, joint | Taxed | Yes | 2 partners | RDB | Law No. 17/2018 |

| Limited Partnership (SCS) | Partnership | Mixed | Taxed | Yes | 2 partners | RDB | Law No. 17/2018 |

| Branch Office | Foreign entity | Parent liable | Taxed | Yes | N/A | RDB | Law No. 17/2018 |

| Representative Office | Foreign entity | Parent liable | Generally exempt | Restricted | N/A | RDB | Law No. 17/2018 |

| Cooperative Society | Cooperative | Limited | Conditional exemptions | Yes | 7 members | RDB / RCCL | Law No. 67/2018 |

| Sole Proprietorship | Individual | Unlimited | Taxed | Yes | 1 owner | RDB | Law No. 17/2018 |

Each of these structures is examined in full in the sections below.

Public Limited Company (Société Anonyme / SA) in Rwanda

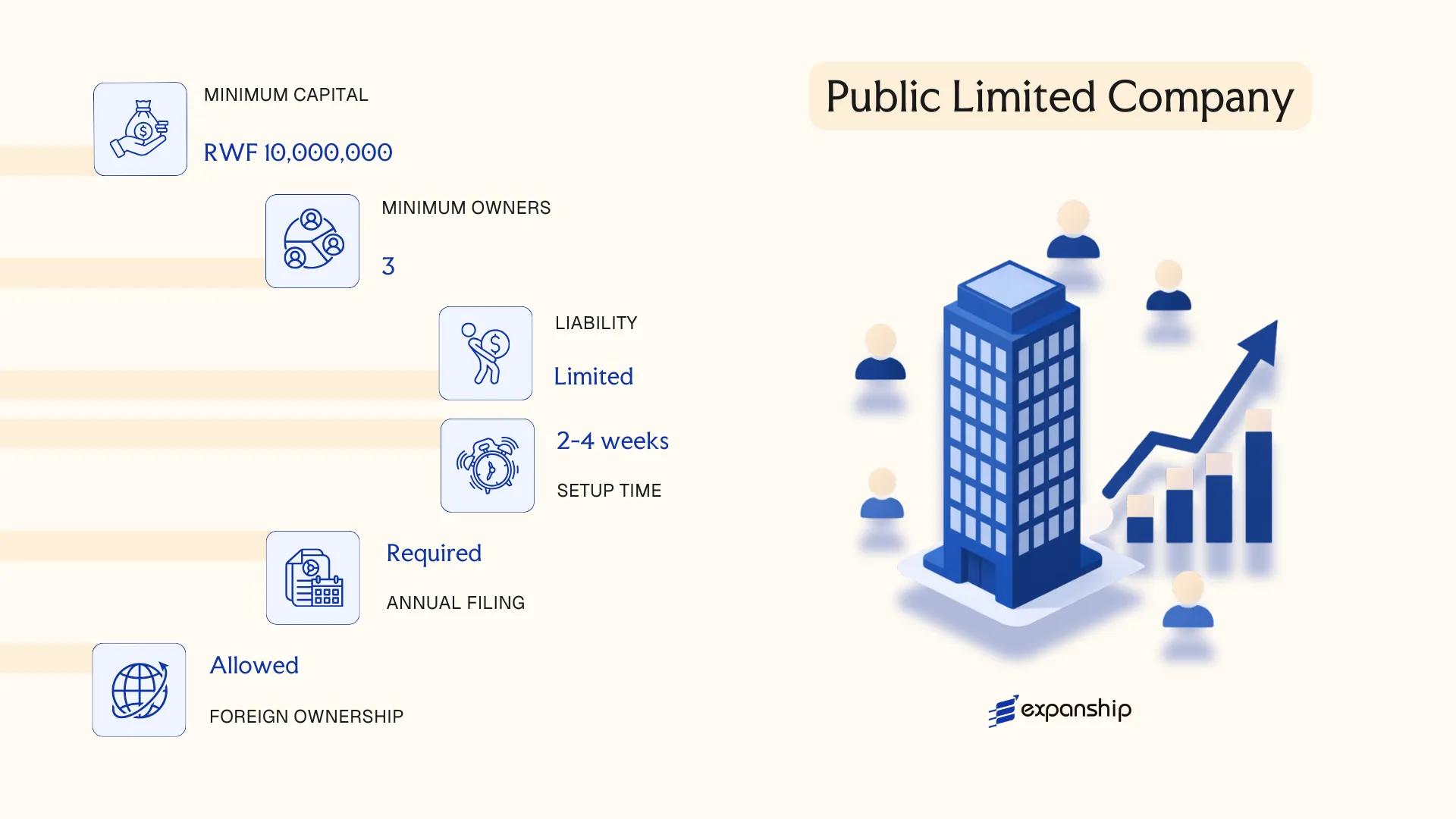

Governed by Law No. 17/2018 of 13/04/2018 on Companies, the public limited company SA Rwanda structure carries a distinct legal personality, fully separate from its shareholders. Liability is confined to each shareholder's capital contribution.

Shares in an SA may be offered to the public, distinguishing it from its private counterpart. The Rwanda Development Board (RDB) oversees registration, while the Capital Market Authority (CMA) regulates any public share offering activity.

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (SA) | Separate legal personality; governed by Law No. 17/2018 |

| Members | Shareholders (min. 2); no statutory maximum | Directors: min. 3 on the board; no maximum |

| Local Presence | Registered office in Rwanda required | No mandatory local director, but a registered address is compulsory |

| Share Capital | Minimum RWF 10,000,000 | Must be fully subscribed; at least 25% paid up at incorporation |

| Shares | Freely transferable; may be listed on Rwanda Stock Exchange (RSE) | Publicly tradeable shares permitted |

| Privacy | Shareholder register is not fully public; filings with RDB are on record | Beneficial ownership disclosure required under AML regulations |

Focus Points

- Taxation: Subject to corporate income tax at 30% (standard rate); VAT at 18% applies to taxable supplies; withholding tax rates vary by payment type (dividends: 15% for non-residents); no stamp duty on share transfers generally.

- Annual Compliance: Audited financial statements required annually; annual general meeting must be held; annual returns filed with RDB.

- Treaty Access: Rwanda has concluded double tax treaties with select jurisdictions, including Mauritius, Belgium, and South Africa; SA entities are eligible to benefit.

- Conversion: An SA may be converted into another company form under Law No. 17/2018 by shareholder resolution and RDB notification.

- Restrictions: Foreign ownership is generally permitted; certain sectors (e.g., media, land) carry ownership restrictions under sector-specific legislation.

Closing

An SA suits large-scale commercial operations, joint ventures with institutional investors, and businesses planning eventual public listing on the RSE. The freely transferable share structure facilitates capital raising, though the minimum capital threshold and mandatory audit requirements create a compliance burden unsuitable for smaller or early-stage operations.

Large enterprises and ventures seeking public investment or stock exchange listing where formal governance and audited accounts are acceptable costs.

Company Incorporation in Rwanda

Register your SA or other business entity in Rwanda with end-to-end support from Expanship.

Private Limited Company (Société à Responsabilité Limitée / SARL) in Rwanda

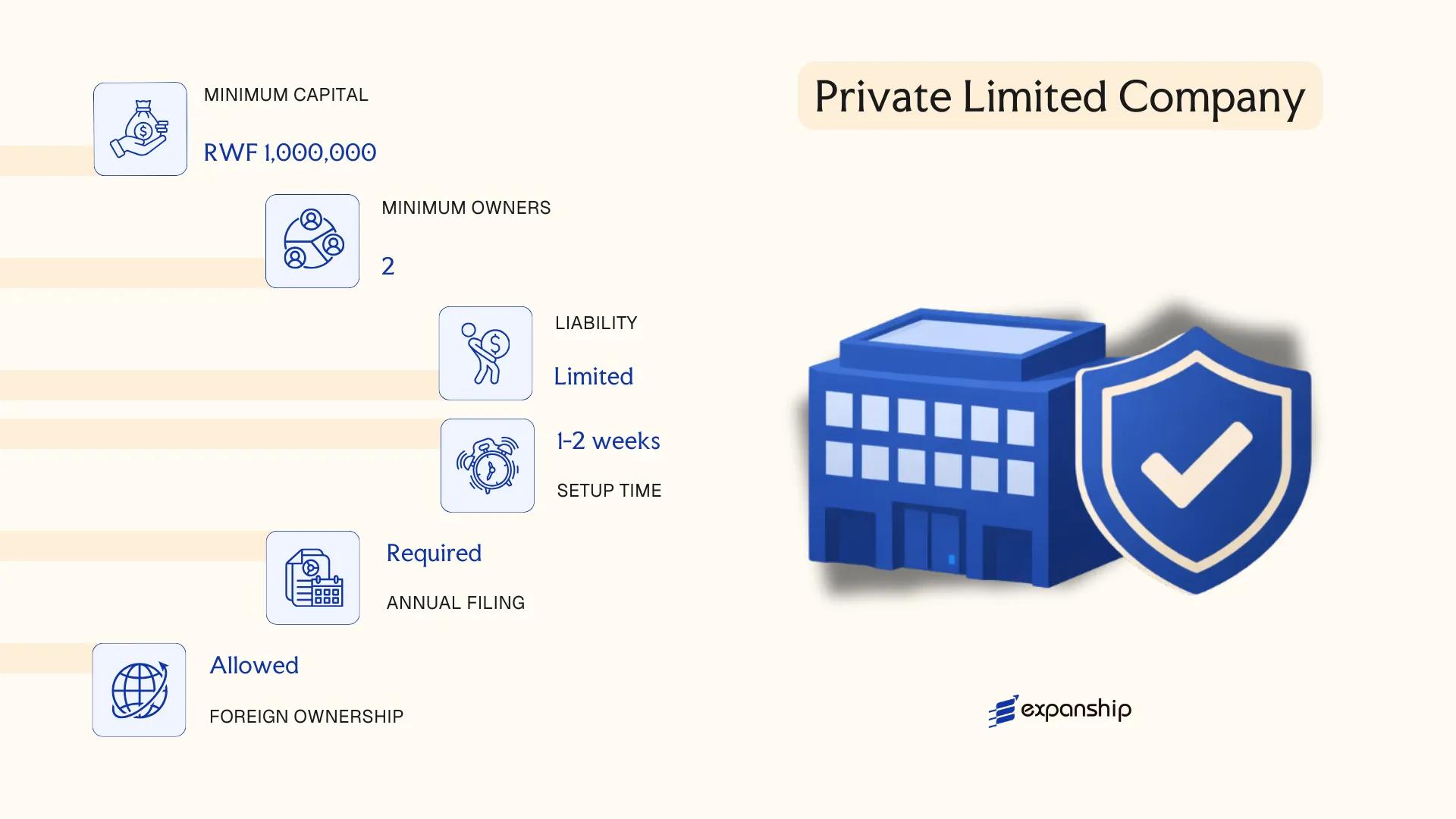

The private limited company SARL Rwanda is governed by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, which Rwanda adopted alongside its own Companies Act (Law No. 17/2018 of 13/04/2018). As a distinct legal entity, the SARL carries separate legal personality from its members, meaning the firm can own assets, enter contracts, and bear liabilities in its own name.

Member liability is capped at the amount each has contributed to the share capital. This hybrid structure — combining elements of partnership flexibility with corporate liability protection — makes it a common choice for small to mid-sized private businesses.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société à Responsabilité Limitée (SARL) | Separate legal personality; limited liability |

| Members | 1–50 shareholders | A single-member SARL (SARL unipersonnelle) is permitted |

| Management | One or more gérants (managers) | Managers need not be shareholders or Rwandan residents |

| Local Presence | Registered office address in Rwanda required | A physical or registered agent address suffices |

| Share Capital | No statutory minimum under current law | Capital denominated in Rwandan Francs (RWF) |

| Privacy | Beneficial ownership disclosure required | Filed with Rwanda Development Board (RDB) |

Focus Points

- Taxation: Corporate income tax applies at 30%; a reduced rate of 15% may apply to qualifying sectors; VAT registration is mandatory once turnover exceeds the prescribed threshold; withholding tax applies to dividends, interest, and service fees paid to non-residents.

- Annual Compliance: Annual returns and financial statements must be filed with RDB; audit requirements depend on company size thresholds.

- Economic Substance: No formal substance regime, but genuine management and control considerations apply for treaty access purposes.

- Treaty Access: Rwanda has a limited but growing double tax treaty network; SARL entities can access applicable treaties subject to beneficial ownership conditions.

- Conversion: A SARL may convert to a Public Limited Company (SA) upon meeting the relevant share capital and shareholder requirements under the Companies Act.

Closing

The SARL suits trading operations, holding structures, and foreign-owned subsidiaries where controlled ownership and liability protection are priorities. Its permissive single-member option adds structural flexibility, though the 50-shareholder ceiling restricts its use for businesses requiring broad equity participation.

Foreign investors and SMEs seeking a privately held operating or holding entity with straightforward governance and capped member liability.

Partnerships in Rwanda [General Partnership (Société en Nom Collectif), Limited Partnership (Société en Commandite Simple)]

Partnership structures in Rwanda are governed by Law No. 17/2018 of 13/04/2018 governing companies in Rwanda, administered through the Rwanda Development Board (RDB). Both partnership forms carry distinct liability profiles that make them structurally different from limited companies.

A Société en Nom Collectif (SNC) holds no separate legal personality distinct from its partners, meaning all partners bear joint and unlimited liability for the firm's debts. The Société en Commandite Simple (SCS), by contrast, introduces a two-tier membership structure, separating those with unlimited exposure from those whose liability is capped at their capital contribution.

Key Characteristics

| Requirement | General Partnership (SNC) | Limited Partnership (SCS) |

|---|---|---|

| Legal Form | Unincorporated; no separate legal personality | Hybrid; partial separation between partner classes |

| Members | Partners (minimum 2, no statutory maximum) | Minimum 1 general partner + 1 limited partner |

| Liability | Unlimited, joint and several for all partners | General partners: unlimited; limited partners: capped at contribution |

| Local Presence | Registered office in Rwanda required | Registered office in Rwanda required |

| Capital | No statutory minimum; RWF-denominated contributions | No statutory minimum; contribution-based |

| Privacy | Partner details filed with RDB; publicly accessible | Both partner classes disclosed in registration records |

Focus Points

- Taxation: Partnerships are generally treated as fiscally transparent; income is taxed at the partner level under Rwanda Revenue Authority (RRA) rules, subject to personal or corporate income tax rates depending on partner type; VAT registration applies where turnover thresholds are met.

- Annual Compliance: Annual returns must be filed with RDB; financial records must be maintained in accordance with Rwandan accounting standards.

- Restrictions: Foreign nationals may face additional requirements under investment regulations; certain regulated sectors restrict partnership structures.

- Conversion: Conversion to a limited company is permissible under the Companies Act framework, subject to RDB approval and re-registration.

- Treaty Access: Access to Rwanda's double taxation agreements depends on the partner's tax residency, not the partnership's registration.

Sub-Types

Société en Nom Collectif (General Partnership)

All members carry unlimited personal liability, making this structure uncommon for high-risk commercial activities. It is typically used by small professional firms or family-run businesses where trust among partners is established.

Société en Commandite Simple (Limited Partnership)

The SCS allows passive investors to participate through limited partnership interests without incurring management obligations or unlimited liability. General partners retain full operational control and bear unrestricted exposure to liabilities.

When to Consider a Partnership Structure

Partnership forms suit arrangements where profit-sharing flexibility and pass-through taxation outweigh the drawbacks of personal liability exposure. The key limitation is the unlimited liability borne by at least one class of partner, which deters use in capital-intensive or high-liability sectors.

Partnership structures are best suited for closely held professional practices or joint ventures between established entities where the partners have agreed liability arrangements and seek fiscal transparency over corporate separation.

Foreign Business Structures in Rwanda [Branch Office, Representative Office]

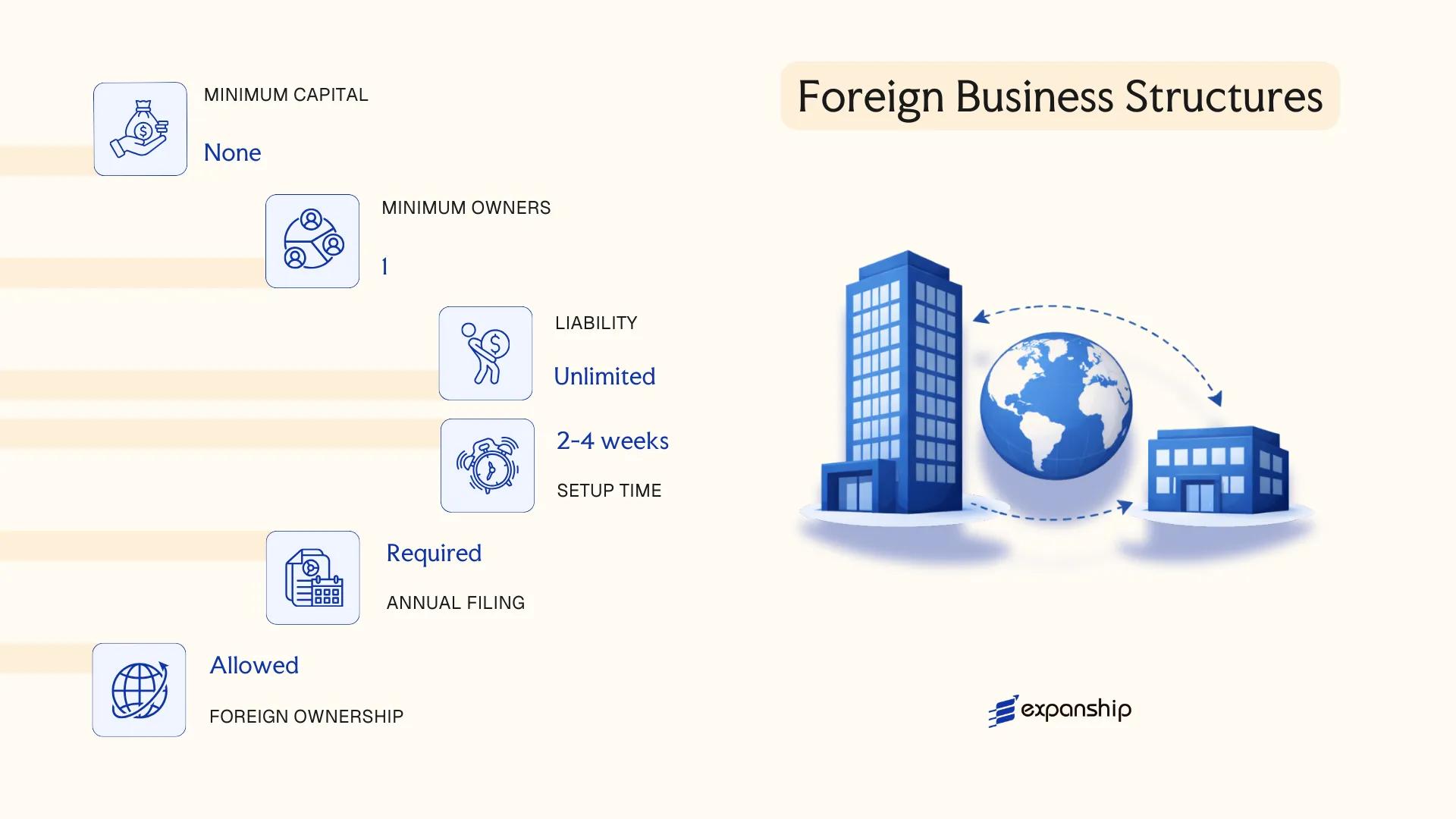

Foreign companies seeking a presence in Rwanda without incorporating a new local entity have two principal options: a branch office or a representative office. Both are governed by the Companies Act No. 17 of 2009 and administered through the Rwanda Development Board (RDB), which manages the One Stop Centre for business registration. A foreign company branch office in Rwanda does not constitute a separate legal entity — the parent company remains fully liable for its obligations.

Registration requires submitting certified copies of the parent company's incorporation documents, constitutional documents, and a resolution authorizing the establishment of the local office. A locally resident authorized agent must be appointed in both cases.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Authorized Representative | Locally resident individual appointed by parent | Locally resident individual appointed by parent |

| Commercial Activity | Permitted — can generate revenue | Not permitted — limited to liaison, market research, promotion |

| Capital Requirement | No statutory minimum | No statutory minimum |

| Local Office | Physical registered address required | Physical registered address required |

| Liability | Parent bears full liability | Parent bears full liability |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at 30%; VAT registration is required if annual turnover exceeds the statutory threshold; withholding tax applies to remittances to the parent at the applicable treaty or domestic rate.

- Economic Substance: A locally resident authorized representative must be maintained; branches conducting substantive operations are expected to maintain adequate local infrastructure.

- Annual Compliance: Annual returns must be filed with RDB; branches must submit audited financial statements of the parent company alongside local accounts where applicable.

- Treaty Access: Rwanda representative office setup and branch structures may access Rwanda's double tax agreements, though entitlement depends on treaty-specific provisions and the nature of income.

- Restrictions: A representative office cannot enter into commercial contracts, invoice clients, or remit profits — any revenue-generating activity requires conversion to a branch or locally incorporated entity.

Sub-Types

Branch Office

A branch office is the trading extension of the parent entity, authorized to conduct the same commercial activities permitted under its parent's constitutive documents. It is the appropriate structure when a foreign firm requires operational capacity — contracting, invoicing, and employing staff locally — without incorporating a separate Rwandan company.

Representative Office

A representative office is limited strictly to non-commercial functions such as market research, promotion of the parent company's services, and liaison activities. It carries no authority to generate revenue or enter into binding commercial agreements on behalf of the parent.

Closing

Both structures suit foreign firms testing market entry before committing to full local incorporation, though the representative office's activity restrictions make it unsuitable for any revenue-generating operation. The primary limitation of both forms is the absence of limited liability — the parent entity carries full legal and financial exposure for all local obligations.

A branch office suits foreign companies that require operational and revenue-generating capacity in Rwanda while maintaining centralized parent control without incorporating a separate local entity.

Cooperative Society in Rwanda

Cooperative society registration Rwanda is governed by Law No. 013/2021 of 16/06/2021 Relating to Co-operatives, which replaced earlier cooperative legislation and brought the framework into closer alignment with contemporary governance standards. A cooperative registered under this law acquires separate legal personality upon registration with the Rwanda Cooperative Agency (RCA).

Members hold limited liability, restricted to their subscribed share contributions. This structure sits between a purely commercial entity and a social enterprise, since it combines economic activity with member-benefit objectives rather than profit maximization for external shareholders.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Cooperative Society | Separate legal personality upon RCA registration |

| Members | Referred to as Members; minimum 7 individuals | No statutory maximum; legal persons may also join |

| Governing Body | Board of Directors elected by General Assembly | Supervisory Committee required for oversight |

| Local Presence | Registered office in Rwanda required | RCA registration is mandatory before operations begin |

| Capital | Rwandan Franc (RWF); no fixed statutory minimum share capital | Each member must subscribe to at least one share |

| Privacy | Member register maintained internally | Not fully public, but regulatory filings made to RCA |

Focus Points

- Taxation: Cooperative societies are subject to corporate income tax at the standard 30% rate; VAT registration applies where turnover thresholds are met; dividend distributions to members may attract withholding tax under domestic rules.

- Annual Compliance: Cooperatives must hold an Annual General Meeting, submit audited financial statements to the RCA, and renew their operating certificate periodically.

- Economic Activity Restriction: A cooperative must operate primarily for the mutual benefit of its members; activities outside the stated cooperative purpose may raise compliance issues with the RCA.

- Conversion: Conversion from a cooperative to a commercial company structure is not straightforwardly provided for under the 2021 law and would require legal restructuring.

- Treaty Access: Cooperatives are resident entities and may access Rwanda's double taxation agreements, subject to meeting beneficial ownership and residency conditions.

Sub-Types

Savings and Credit Cooperative (SACCO)

SACCOs are cooperatives focused specifically on financial services — accepting member deposits and extending credit — and are regulated by the National Bank of Rwanda (BNR) in addition to the RCA, creating a dual regulatory oversight requirement distinct from general cooperatives.

Agricultural Cooperative

This sub-type organises farmers or agro-processors around shared production, processing, or marketing activities, and may qualify for sector-specific government support programs administered through the Ministry of Agriculture and Animal Resources.

Closing

A cooperative society suits member-owned enterprises in agriculture, savings, trade, and services where profit is shared among active participants rather than passive investors. The principal advantage is the democratic governance model, where voting rights are not proportional to capital contribution. The main limitation is restricted access to external equity financing, since ownership cannot be transferred freely to outside investors.

Groups of individuals — particularly in agriculture, financial services, or community trade — who intend to operate collectively for shared economic benefit rather than attracting third-party investment.

Sole Proprietorship (Entreprise Individuelle) in Rwanda

A sole proprietorship Rwanda — known as an Entreprise Individuelle — is the simplest form of business registration available to individual traders and entrepreneurs. Governed by the Rwandan Commercial Code and administered through the Rwanda Development Board (RDB), this structure carries no separate legal personality from its owner.

Because the proprietor and the business are legally one and the same, personal assets remain directly exposed to any business debts or liabilities incurred.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Entreprise Individuelle) | No separate legal personality from the owner |

| Member Reference | Proprietor | Single individual only; no co-ownership permitted |

| Membership | 1 proprietor (min and max) | Cannot be held by a legal entity |

| Local Presence | Registered business address in Rwanda | Physical or virtual address acceptable at registration |

| Capital | No statutory minimum capital required | Owner funds the business directly |

| Privacy | Owner's name publicly associated with the business | Limited privacy; no nominee arrangement applicable |

Focus Points

- Taxation: Subject to personal income tax on business profits; VAT registration required once annual turnover exceeds the RDB threshold; no separate corporate tax applies.

- Annual Compliance: Annual renewal of the business registration certificate with the RDB is required to maintain active status.

- Conversion: Can be converted into a more formal structure such as a SARL, though this requires a new registration process rather than a simple reclassification.

- Treaty Access: As a pass-through structure with no separate legal personality, access to double taxation treaty benefits is limited and assessed at the individual level.

- Restrictions: Foreign nationals face ownership restrictions; eligibility to register as a sole trader is generally reserved for Rwandan citizens or residents holding valid work authorisation.

Closing

The Entreprise Individuelle suits small-scale traders, freelancers, and micro-enterprises operating domestically with low liability exposure. Its primary advantage is administrative simplicity, but the absence of limited liability makes it unsuitable for any business carrying significant financial or contractual risk.

This structure is best suited for Rwandan citizens or resident individuals running low-risk, single-operator businesses with modest turnover.

How to Choose the Right Entity Type in Rwanda

Selecting the correct structure at the outset determines your tax position, liability exposure, and compliance obligations for the life of your business. Understanding how to choose a business structure in Rwanda requires moving beyond general preference and examining the concrete legal and operational consequences of each option.

Why Your Entity Choice Matters

The Rwanda Companies Act (Law No. 17/2018) governs most registered entities, and operating outside the boundaries of your registered structure carries real consequences:

- Registering a foreign branch while conducting independent local trade can result in that entity being treated as an unregistered company, exposing it to deregistration or financial penalties.

- Selecting a structure that lacks access to Rwanda's tax treaty network means you cannot claim reduced withholding tax rates on dividends, interest, or royalties paid to counterpart jurisdictions.

- Forming a company when your objective is asset holding or succession planning locks you into annual general meeting requirements and shareholder obligations that do not apply to trust arrangements.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors such as banking or insurance, and passive asset holding each require a distinct structure under Rwandan law.

- Ownership Configuration: A sole shareholder may prefer a single-member SARL, while multi-party ventures requiring formal governance will need an SA with a board structure.

- Tax Objectives: Your eligibility for specific regimes under the Rwanda Income Tax Law depends on entity type and residency status.

- Substance Capacity: If you cannot maintain a physical presence or resident staff, certain entity types will expose you to compliance failures under local substance expectations.

- Exit Strategy: Not all Rwandan entities permit redomiciliation or conversion; confirm these options before incorporating.

Compliance Services for Companies in Rwanda

Ongoing compliance support for Rwandan entities, including annual returns, statutory filings, and regulatory reporting.

Conclusion

Selecting the right structure is a foundational decision in any Rwanda company incorporation summary, and the options under the Companies Act (2009, as amended) cover a wide spectrum of operational and ownership needs. The Private Limited Company remains the most registered entity type, favored by small and medium enterprises for its flexible shareholding and capped liability. Public Limited Companies suit firms pursuing capital markets access; General Partnerships fit closely held professional ventures where partners accept joint liability. Branches serve foreign firms requiring a direct operational presence without a separate legal entity. Cooperative Societies address member-owned enterprises in agriculture and community services.

Registration is administered through the Rwanda Development Board, which has progressively reduced incorporation timelines. Your choice of structure will carry direct implications for governance obligations, tax registration, and post-incorporation compliance across the entity's lifecycle.

How Expanship Can Assist You

Expanship Rwanda company formation services cover the full spectrum of entity types discussed in this guide — from a Private Limited Company (SARL) registered under the Rwanda Development Board (RDB) to a Branch Office operating under a foreign parent. Each structure carries distinct filing requirements, and working with an experienced team reduces the risk of procedural delays at registration.

Expanship can support your business at every stage of the process in Rwanda:

- Preparation and legalization of incorporation documents

- Registered agent and registered office provision

- Government filing and liaison with the Rwanda Development Board

- Post-incorporation compliance management, including annual returns

- Corporate bank account introduction assistance

Ready to move forward? Contact Expanship Rwanda to discuss the right structure for your business.

Frequently Asked Questions (FAQ)

The Private Limited Company (SARL) is the most frequently incorporated entity, registered through the RDB's online portal. Its combination of limited liability, a single-shareholder minimum, and no mandatory public share offering makes it the default choice for small and medium-sized businesses.

A Branch Office is not a separate legal entity; it remains an extension of its foreign parent and carries the parent's full liability exposure. A SARL is an independent legal entity subject to Rwandan corporate income tax on locally sourced profits, while a Branch is taxed on income attributable to its Rwandan operations. Compliance obligations for a SARL are generally broader, including statutory audits above certain thresholds.

Among registered structures, the SARL offers relatively limited public disclosure compared to a Public Limited Company (SA), whose shareholder register and financial statements face broader disclosure requirements. Nominee arrangements are legally permissible but must still satisfy beneficial ownership registration requirements under Rwanda's anti-money laundering framework.

A sole proprietorship and a SARL can both be formed by one individual. General Partnerships and Limited Partnerships require at least two partners by their legal definition under the Companies Act. An SA requires a minimum of one shareholder but carries additional governance requirements, including a board structure.

Foreign individuals and foreign-owned companies may incorporate a SARL, SA, or establish a Branch Office or Representative Office without a mandatory local partner requirement. Certain regulated sectors may impose additional conditions, but the general incorporation framework under the Companies Act does not restrict foreign ownership by nationality.

Conversion between entity types is permitted under Rwandan company law. A SARL may be converted to an SA, for example, through a formal resolution process filed with the RDB. The converted entity retains its legal continuity, including existing contracts and liabilities.

Not all do. A Sole Proprietorship has no legal separation between the owner and the business, meaning personal assets remain exposed to business liabilities. SARLs, SAs, and Cooperative Societies each hold distinct legal personality under Rwandan law, while a Branch Office derives its legal standing from its parent company.

A Sole Proprietorship imposes the lightest administrative burden, with no statutory audit requirement and minimal annual filing obligations. By contrast, an SA faces the most extensive ongoing requirements, including mandatory external audits, board meeting records, and public financial disclosures where applicable.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.