Key Takeaways

- Romania's most commonly registered entity, the Societate cu Răspundere Limitată (SRL), is governed by Law No. 31/1990 and can be formed by a single member with a low minimum capital threshold.

- The Societate cu Răspundere Limitată Debutant (SRL-D) offers specific fiscal concessions designed for young entrepreneurs within the European Union.

- All business registrations in Romania are processed and maintained by the Oficiul Național al Registrului Comerțului (ONRC), which also handles structural changes across all entity types.

- Foreign companies seeking market entry without full incorporation can establish a branch office or representative office before committing to a locally incorporated subsidiary.

Introduction to Entity Types in Romania

Romania sits in southeastern Europe, bordered by Bulgaria, Serbia, Hungary, Ukraine, and Moldova, with Black Sea coastline to the east. It is an independent nation and a European Union member state, which means company formation and ongoing compliance operate within both domestic law and applicable EU regulatory frameworks. Business registration falls under the authority of the Oficiul Național al Registrului Comerțului (ONRC), the National Trade Register Office, which processes incorporations, maintains the commercial register, and handles structural changes for all registered entities.

Romania applies a standard corporate income tax rate, with a micro-enterprise regime available to qualifying smaller firms — making its tax posture relevant to both local operators and foreign investors structuring regional operations.

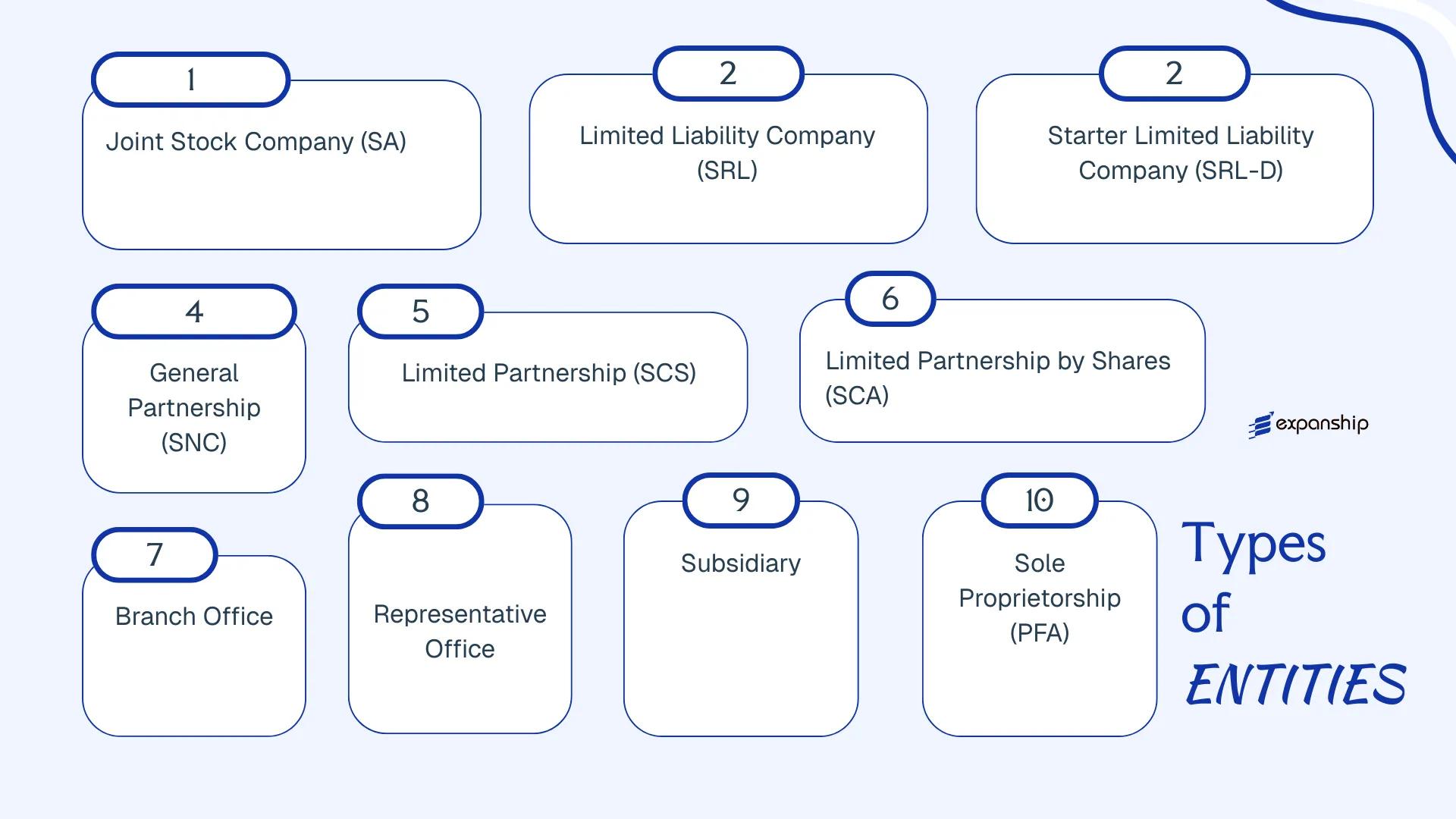

The types of business entities in Romania span several distinct legal forms. These include the Societate pe Acțiuni (SA), Societate cu Răspundere Limitată (SRL), Societate cu Răspundere Limitată Debutant (SRL-D), Societate în Nume Colectiv (SNC), Societate în Comandită Simplă (SCS), Societate în Comandită pe Acțiuni (SCA), Branch Office, Representative Office, Subsidiary, and the individual-based structures PFA, II, and IF. Each form carries distinct liability, governance, and compliance obligations under Romanian company law, primarily governed by Law No. 31/1990 on companies.

An Overview of Business Structures in Romania

Romanian company law recognises several distinct entity types, each governed primarily by Law No. 31/1990 on Companies, as subsequently amended and republished. The Civil Code and specific sector regulations supplement this framework in certain cases. Each structure carries different implications for liability, governance, and tax treatment.

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| SA | Joint Stock Company | Limited to shares | Corporate tax | Yes | 2 shareholders | Trade Register | Law 31/1990 |

| SRL | Limited Liability Co. | Limited to capital | Corporate tax | Yes | 1–50 associates | Trade Register | Law 31/1990 |

| SRL-D | Starter LLC | Limited to capital | Corporate tax | Yes | 1–5 associates | Trade Register | Law 31/1990 |

| SNC | General Partnership | Unlimited, joint | Corporate tax | Yes | Min. 2 partners | Trade Register | Law 31/1990 |

| SCS | Simple Ltd. Partnership | Mixed liability | Corporate tax | Yes | Min. 2 partners | Trade Register | Law 31/1990 |

| SCA | Ltd. Partnership/Shares | Mixed liability | Corporate tax | Yes | Min. 2 partners | Trade Register | Law 31/1990 |

| Branch | Extension of parent | Parent liable | Corporate tax | Restricted | N/A | Trade Register | Law 31/1990 |

| Rep. Office | Non-trading presence | Parent liable | Exempt/limited | No | N/A | Trade Register | GEO 44/2008 |

| PFA | Sole trader | Unlimited personal | Income tax | Yes | 1 individual | Trade Register | GEO 44/2008 |

| II | Individual enterprise | Unlimited personal | Income tax | Yes | 1 individual | Trade Register | GEO 44/2008 |

| IF | Family enterprise | Unlimited personal | Income tax | Yes | 2–5 members | Trade Register | GEO 44/2008 |

Each of these structures is examined in full in the sections below.

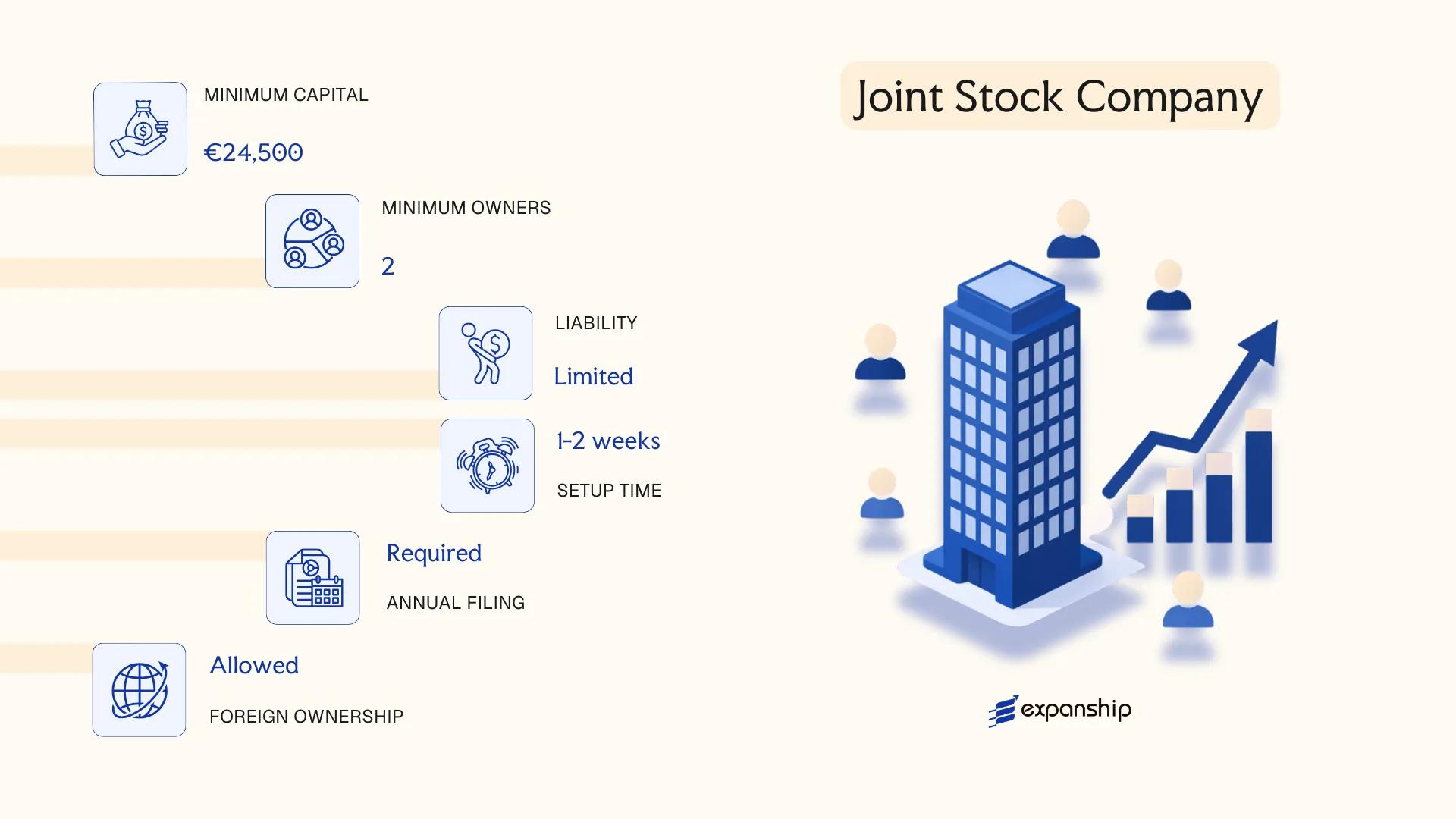

Societate pe Acțiuni (SA) — Joint Stock Company

The Societate pe Acțiuni (SA) is governed by Law No. 31/1990 on companies, as subsequently amended, and represents the most structurally complex corporate form available under Romanian law. It carries separate legal personality, meaning the entity holds rights and obligations independently of its shareholders.

Liability is limited to each shareholder's capital contribution. The SA is the required form for regulated activities such as banking, insurance, and public offerings of securities, making it the standard vehicle for larger commercial operations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock Company (Societate pe Acțiuni) | Separate legal personality; governed by Law No. 31/1990 |

| Members | Shareholders (minimum 2; no statutory maximum) | Shareholders elect a Board of Directors or a Supervisory Board |

| Management | Unitary system (Board of Directors) or Dualist system (Supervisory Board + Directorate) | Dualist system mandatory for certain regulated entities |

| Local Presence | Registered office in Romania required | No statutory requirement for a local resident director, but regulated entities may face additional requirements from the relevant supervisory authority |

| Share Capital | Minimum RON 90,000 (approx. EUR 18,000); must be divided into shares with a minimum nominal value of RON 0.1 | At least 30% of subscribed capital must be paid up at incorporation; remainder within 12 months |

| Privacy | Shareholder register maintained at the company; SA shares can be dematerialised and held via the Central Depository (Depozitarul Central) for listed entities | Beneficial ownership reported to the Trade Register |

Focus Points

- Taxation: Corporate income tax at 19% applies (with a micro-enterprise alternative regime for qualifying entities); VAT registration required once turnover exceeds the statutory threshold; dividend withholding tax at 8% applies to distributions, subject to reduction under applicable EU directives or double tax treaties; no stamp duty on share transfers in standard form.

- Annual Compliance: Annual financial statements must be filed with the Trade Register; statutory audit is mandatory for SA entities regardless of size thresholds that apply to other forms.

- Economic Substance: No specific economic substance legislation applies to domestic SAs, but corporate tax residency rules require effective management to be exercised in Romania.

- Treaty Access: As a Romanian tax resident entity, an SA has full access to Romania's network of double tax treaties and benefits under EU Parent-Subsidiary and Interest-Royalties Directives.

- Conversion: An SA may be converted into another legal form (including SRL) by shareholder resolution, subject to creditor protection procedures under Law No. 31/1990.

Sub-Types

Closed (Nelistată) SA

Shares are not publicly traded and are transferred subject to restrictions set out in the articles of association. This structure is used for private holding arrangements or large family-owned businesses that require the corporate governance framework of an SA without public market exposure.

Listed (Listată) SA

Shares are admitted to trading on a regulated market or multilateral trading facility, primarily the Bucharest Stock Exchange (Bursa de Valori București). Listed SAs are subject to additional obligations under Law No. 24/2017 on issuers of financial instruments and market operations, including continuous disclosure requirements and oversight by the Financial Supervisory Authority (ASF).

An SA suits large-scale commercial operations, regulated businesses, and entities planning public capital raises or institutional investment. The mandatory statutory audit and higher minimum capital make it less practical for small or early-stage ventures.

Best suited for businesses in regulated sectors, enterprises seeking capital market access, or large corporate groups requiring a formal governance structure with distinct supervisory and executive layers.

Company Incorporation in Romania

Expanship assists with the full incorporation process for SA and other Romanian entity types, including Trade Register filings and post-incorporation compliance setup.

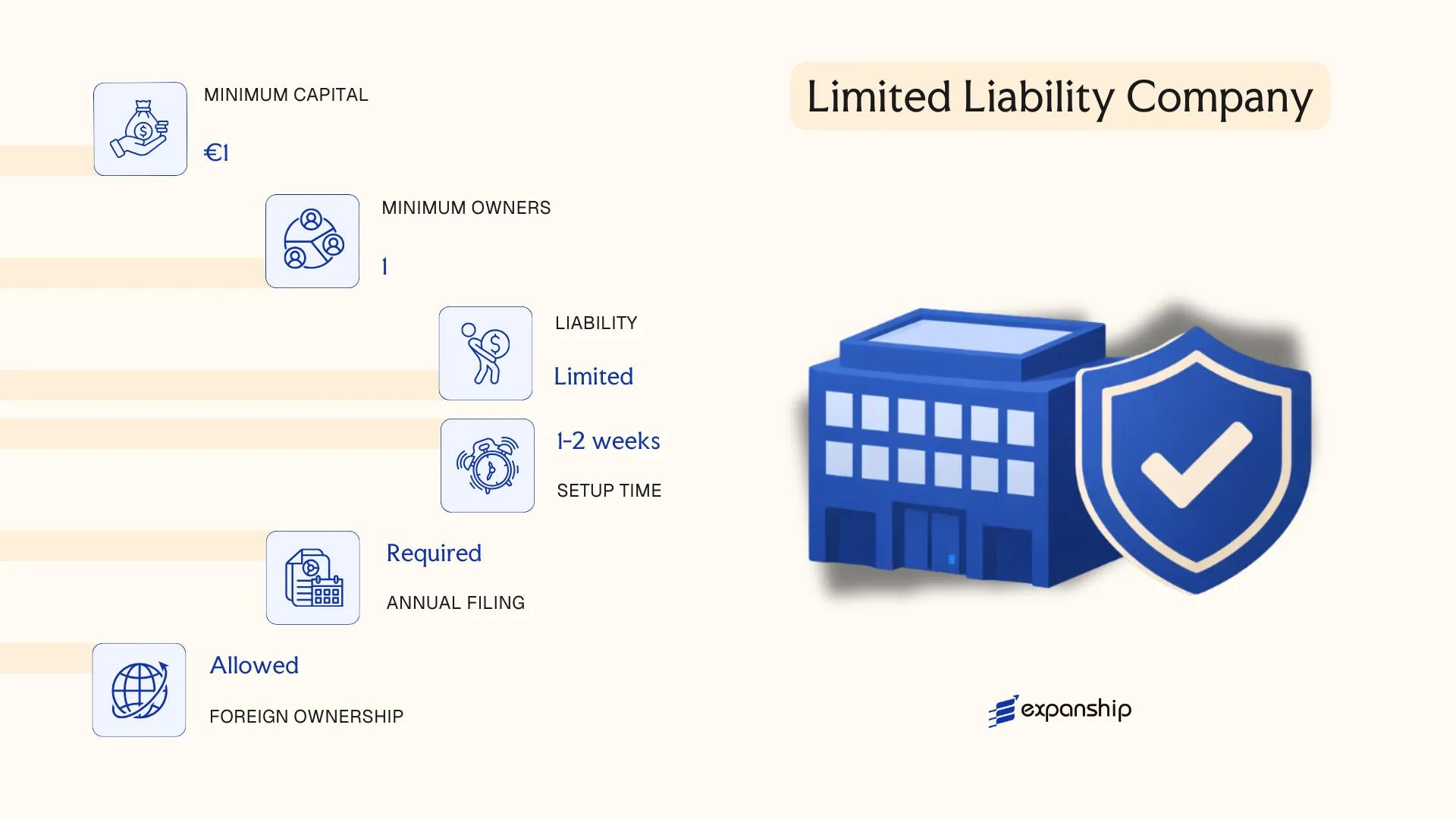

Societate cu Răspundere Limitată (SRL) — Limited Liability Company

The Societate cu Răspundere Limitată SRL Romania is governed primarily by Law No. 31/1990 on Companies, as subsequently amended. It carries separate legal personality, meaning the entity's assets and liabilities are legally distinct from those of its shareholders.

Structurally, the SRL functions as a hybrid: it combines the limited liability protections associated with a joint stock company with the operational simplicity typical of a partnership. Shareholders are liable only to the extent of their capital contributions.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private limited liability company | Closed structure; shares cannot be publicly traded |

| Members | Associates (shareholders) and one or more managers (administratori) | Minimum 1, maximum 50 associates; managers need not be shareholders |

| Local Presence | Registered office address in Romania | Must be maintained at all times; commercial agent not mandated |

| Share Capital | Minimum RON 200; divided into equal social parts of at least RON 10 each | No maximum; contributions may be in cash or in kind |

| Transferability | Share transfers to third parties require associate approval | Articles of association may impose additional restrictions |

| Privacy | Associates and managers disclosed in the Trade Register | Beneficial ownership must be declared under AML legislation |

Focus Points

- Taxation: Subject to 16% corporate income tax; micro-enterprise revenue tax (1% or 3%) may apply if turnover is below RON 500,000; standard VAT rate of 19%; withholding tax applies to dividends paid to non-residents at 8% (subject to EU directives or applicable tax treaties).

- Annual Compliance: Financial statements must be filed with the Ministry of Finance annually; statutory audit is not mandatory below certain size thresholds.

- Economic Substance: No formal substance regime, but tax residency and management-and-control tests apply under Romanian fiscal law.

- Treaty Access: As a tax-resident entity, the SRL can access Romania's network of double taxation treaties.

- Conversion: An SRL may be converted into an SA or other company form through a general meeting resolution, subject to Trade Register procedures.

Closing

The SRL suits trading operations, holding structures, and service businesses where a small number of principals wish to retain close control. Its low capital threshold reduces the initial financial commitment, though the 50-associate ceiling limits its use as a vehicle for broad equity participation.

The SRL is most appropriate for small to mid-sized businesses, foreign investors establishing a locally incorporated subsidiary, and entrepreneurs seeking operational control with limited personal liability exposure.

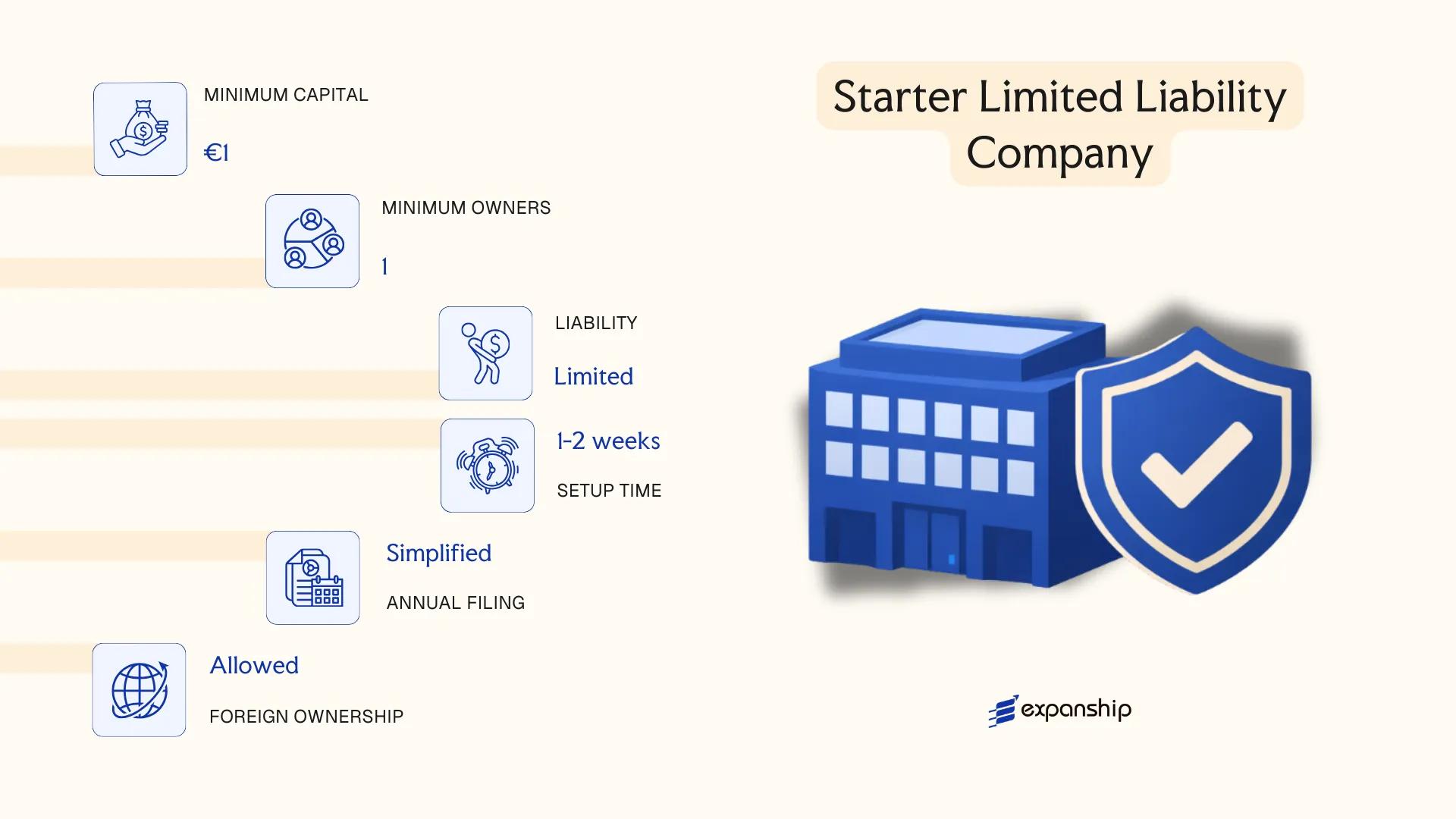

Societate cu Răspundere Limitată Debutant (SRL-D) — Starter Limited Liability Company

The SRL-D starter company Romania introduced through Government Emergency Ordinance no. 6/2011 (subsequently amended) is a time-limited variant of the standard SRL, designed specifically for first-time entrepreneurs. It carries separate legal personality and limits member liability to the value of their subscribed share capital.

Eligibility criteria distinguish this structure from the base SRL. Each founding associate must not have previously held shares in another Romanian commercial company, and the total number of associates cannot exceed five.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited liability company (debutant variant) | Governed by GEO 6/2011 and Law 31/1990 |

| Members | Associates (shareholders); maximum 5 | All associates must be first-time business owners |

| Management | Administrator(s) | Can be an associate or a third party |

| Share Capital | Minimum RON 200 (same as standard SRL) | Must be fully paid at registration |

| Local Presence | Registered office in Romania required | No statutory requirement for a local administrator |

| Duration | Active status limited to 3 years from registration | Must convert to standard SRL after the debutant period |

Focus Points

- Taxation: Subject to standard Romanian corporate income tax (16%), microenterprise revenue tax (1% or 3% depending on conditions), VAT registration thresholds apply at RON 300,000 annual turnover, and standard withholding tax rates apply to dividends.

- Social contributions: The SRL-D may qualify for partial exemption from certain employer social contributions during the debutant period, subject to meeting headcount and activity conditions under GEO 6/2011.

- Annual compliance: Must file annual financial statements with the Trade Register and maintain accounting records in accordance with Romanian OMFP accounting regulations.

- Conversion obligation: Upon expiry of the 3-year debutant period, the entity must convert to a standard SRL or dissolve; continuation as an SRL-D is not permitted.

- Restrictions: Associates cannot simultaneously hold shares in any other Romanian commercial company during the debutant period.

Closing

The SRL-D suits early-stage domestic trading or service businesses where founders have no prior share ownership history in Romanian entities and want a structured entry point with a defined transition to standard operations. The primary limitation is the 3-year ceiling on debutant status, which imposes a mandatory restructuring obligation regardless of business readiness.

First-time founders launching a domestic Romanian business who meet the eligibility criteria under GEO 6/2011 and can plan for conversion to a standard SRL within three years.

Partnerships in Romania (Societate în Nume Colectiv, Societate în Comandită Simplă, Societate în Comandită pe Acțiuni)

Partnerships in Romania — SNC, SCS, and SCA — are governed by Law No. 31/1990 on companies, the same foundational legislation that regulates most Romanian business structures. All three forms carry separate legal personality once registered with the Trade Register (Oficiul Național al Registrului Comerțului, or ONRC), which distinguishes them from informal arrangements under civil law.

Liability treatment varies significantly across these three forms. In a Societate în Nume Colectiv (SNC), all partners bear unlimited joint liability for company obligations. The two comandită variants introduce a split between general partners (asociați comanditați), who hold unlimited liability, and limited partners (asociați comanditari), whose exposure is capped at their capital contribution.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Forms | SNC, SCS, SCA | Three distinct structures under Law 31/1990 |

| Members | SNC: min. 2 general partners, no cap; SCS: min. 1 general + 1 limited partner; SCA: min. 2 general + min. 5 shareholders | SCA shareholders may transfer shares; SNC/SCS interests are non-transferable without partner consent |

| Liability | SNC: unlimited for all; SCS: unlimited for general, capped for limited; SCA: same split as SCS | General partners in all forms face personal asset exposure |

| Registered Office | Physical registered address in Romania required for ONRC registration | No registered agent requirement analogous to common-law jurisdictions |

| Share Capital | SNC/SCS: no statutory minimum; SCA: RON 90,000 minimum | SCA must maintain capital above this threshold throughout its existence |

| Privacy | Partner names appear in the Trade Register and are publicly accessible | No beneficial ownership concealment available |

Focus Points

- Taxation: Partnerships are generally treated as corporate taxpayers subject to 16% corporate income tax; VAT registration thresholds and obligations apply as with other Romanian entities; dividend withholding tax of 8% applies on distributions to non-resident partners absent treaty relief.

- Annual Compliance: Entities must file annual financial statements with ONRC and submit corporate tax returns to ANAF (Agenția Națională de Administrare Fiscală).

- Treaty Access: Romanian tax treaties apply, though access depends on the entity's tax residency classification and the treaty partner's treatment of the specific partnership form.

- Restrictions: General partners in SNC and SCS cannot limit their personal liability by contract; this structural feature cannot be modified through the constitutive act.

- Conversion: Romanian law permits conversion between company forms through a shareholder/partner resolution and re-registration with ONRC, subject to applicable capital requirements of the target form.

Sub-Types

Societate în Nume Colectiv (SNC)

All partners hold unlimited, joint, and several liability. This structure is used primarily in professional services or family-operated businesses where partners accept mutual exposure and require no minimum capital.

Societate în Comandită Simplă (SCS)

The SCS separates active management (general partners) from passive investors (limited partners). Limited partners may not engage in management acts without forfeiting their liability protection under Romanian law.

Societate în Comandită pe Acțiuni (SCA)

The SCA mirrors the SCS liability split but issues shares to its limited partners, making it the closest Romanian equivalent to a limited partnership with transferable interests. Its RON 90,000 capital requirement and five-shareholder minimum make it structurally heavier than the SCS.

These partnership forms are most commonly used in family businesses, professional practices, or structures requiring tiered investor involvement. The liability protection available to limited partners in the SCS and SCA offers a clear structural advantage, though unlimited personal exposure for general partners remains a significant drawback across all three forms.

Romanian partnership structures are best suited for closely held family businesses or professional operators who require flexible capital arrangements and are prepared to accept personal liability at the general partner level.

Foreign Business Presence in Romania (Branch Office, Representative Office, Subsidiary)

Establishing a foreign company presence in Romania is governed primarily by Law No. 31/1990 on Companies, alongside Government Ordinance No. 44/2016 for certain procedural aspects of branch registration. The structure you choose determines whether your foreign parent carries direct liability or operates through a legally separate entity.

Registration for all three forms is handled through the Romanian Trade Registry (Registrul Comerțului), under the National Trade Register Office (ONRC).

Key Characteristics

| Requirement | Branch Office | Representative Office | Subsidiary (SRL/SA) |

|---|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent | Separate legal entity |

| Liability | Parent bears full liability | Parent bears full liability | Limited to entity's own capital |

| Permitted Activities | Commercial and operational | Promotional and liaison only | Full commercial scope |

| Registration Body | ONRC | ONRC + Ministry of Economy (sector-dependent) | ONRC |

| Minimum Capital | None prescribed | None prescribed | As per SRL or SA rules |

| Tax Registration | Required; treated as permanent establishment | Generally not a taxable entity | Independent taxpayer |

Focus Points

- Taxation: Branch offices are taxed as permanent establishments at the standard 16% corporate rate; representative offices pay a flat annual tax (fixed-sum tax regime); subsidiaries are subject to full Romanian corporate tax, VAT (19% standard rate), and applicable withholding taxes on dividends remitted to the parent.

- Substance obligations: Branch offices must maintain a local registered address and appoint a designated representative authorised to act on behalf of the parent.

- Annual compliance: All three forms must file annual financial statements with ONRC; branches and subsidiaries additionally file corporate tax returns with ANAF (Agenția Națională de Administrare Fiscală).

- Treaty access: Only subsidiaries, as separate legal entities, can access Romania's network of double taxation treaties in their own right; branches typically rely on the parent's treaty position.

- Restrictions: Representative offices cannot invoice clients, generate revenue, or enter into commercial contracts in their own name.

Sub-Types

Branch Office (Sucursală)

A branch has no independent legal personality and operates as a direct extension of the foreign parent, which remains fully liable for all branch obligations. It suits foreign firms that want operational presence without incorporating a separate entity.

Representative Office (Birou de Reprezentanță)

Restricted to non-commercial activities such as market research, promotion, and liaison, a representative office cannot conduct revenue-generating transactions. It is typically used during a market-entry assessment phase before committing to a fuller structure.

Subsidiary

Incorporated as an SRL or SA under Romanian law, a subsidiary is a legally distinct entity with its own rights and obligations, entirely separate from the foreign parent's balance sheet.

When to Use This Structure

Branch and representative offices suit foreign businesses testing or supporting existing operations, while a subsidiary is the standard choice for sustained commercial activity requiring liability separation. The principal limitation of a branch is the parent's unlimited exposure to Romanian liabilities.

Foreign companies with existing operations seeking a controlled, defined-scope presence in the Romanian market without full independent incorporation.

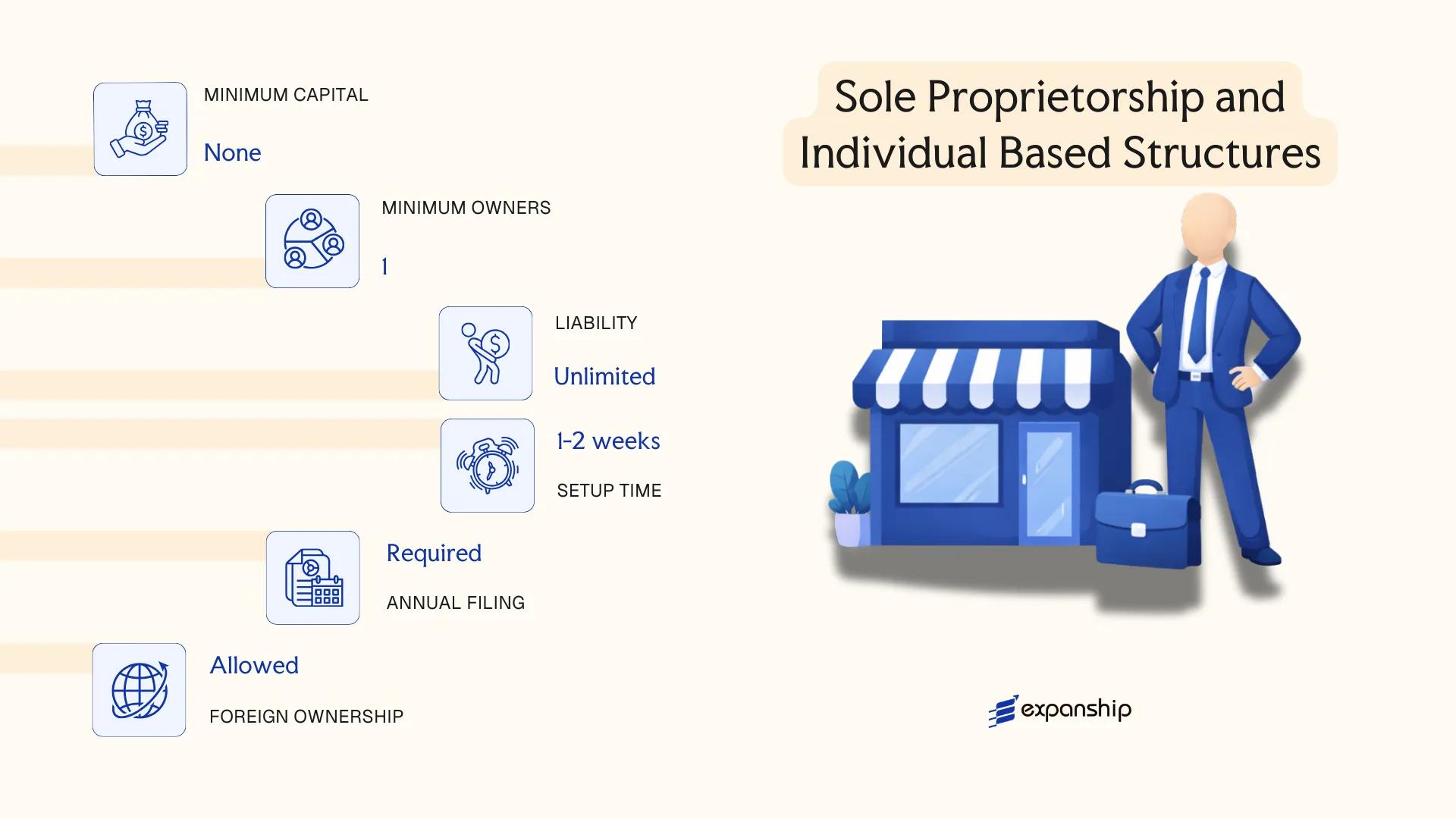

Sole Proprietorship and Individual-Based Structures (PFA, II, IF)

Romanian law recognises three individual-based business forms under Government Emergency Ordinance no. 44/2008: the Persoană Fizică Autorizată (PFA), the Întreprindere Individuală (II), and the Întreprindere Familială (IF). None of these carry separate legal personality — the individual remains personally liable for all obligations incurred.

A PFA sole proprietorship Romania registers directly with the Trade Registry and is linked to a specific CAEN activity code. The PFA cannot be transferred or inherited as a going concern, which distinguishes it structurally from the II, which may employ up to three staff outside the family unit.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated individual enterprise | No separate legal personality; personal liability applies to all three forms |

| Members | PFA: 1 natural person; II: 1 natural person; IF: 2–5 family members | II owner must be 18+; IF members must share a family relationship as defined by the Civil Code |

| Registered Office | Local address required; registered with the Trade Registry | Must correspond to the declared activity location |

| Capital | No minimum capital requirement | No share structure; assets are personal assets of the proprietor |

| Activity Scope | Tied to declared CAEN codes at registration | Changing or adding codes requires a formal amendment at the Trade Registry |

| Privacy | Owner's name and address appear in the public Trade Registry record | No meaningful privacy protection |

Focus Points

- Taxation: PFA income is taxed as personal income under the Fiscal Code; a 10% flat income tax applies, along with CAS (25%) and CASS (10%) social contributions subject to income ceilings; VAT registration is mandatory above the RON 300,000 threshold.

- Annual Compliance: Annual income declarations must be filed with ANAF; accounting obligations are lighter than for corporate entities, with single-entry bookkeeping permitted under certain conditions.

- Activity Restrictions: Each form is bound to the CAEN codes declared at registration; commercial activities of a corporate nature are not permitted under OUG 44/2008.

- Conversion: A PFA or II may be converted into an SRL without dissolving the underlying activity, though the process requires a new incorporation procedure at the Trade Registry.

- Treaty Access: These structures do not qualify as corporate residents for purposes of Romania's double tax treaty network; treaty benefits available to companies do not extend to individual-based forms.

Sub-Types

Persoană Fizică Autorizată (PFA)

The PFA is the simplest form, suited to freelancers and independent professionals. The individual operates under their own name and bears unlimited personal liability, with no employees permitted beyond the proprietor themselves.

Întreprindere Individuală (II)

The II extends the PFA model by allowing the proprietor to hire up to three employees who are not family members, making it appropriate for micro-businesses requiring a small workforce without corporate overhead.

Întreprindere Familială (IF)

The IF is established by a family agreement rather than a registration deed and requires between two and five family members as defined under the Civil Code. Management authority rests with a designated family representative, and profit distribution follows the terms of the family agreement.

These structures suit Romanian-resident individuals operating service-based or trade activities at a small scale, with the main advantage being minimal administrative burden relative to a corporate entity. The principal limitation is unlimited personal liability, which exposes the individual's private assets to business creditors with no structural separation.

Individual residents providing freelance, consultancy, or small-scale trade services who do not require liability protection or external investment capacity.

How to Choose the Right Entity Type in Romania

Selecting how to choose a company type in Romania is not a procedural formality — the structure you register determines your tax exposure, liability, reporting obligations, and operational capacity from day one.

Why Your Entity Choice Matters

Registering the wrong structure carries concrete consequences:

- An SRL-D that exceeds the statutory thresholds — 1 million RON in share capital contributions or five years of operation — automatically loses its preferential status, creating unexpected compliance costs if the business has not planned for the transition.

- Choosing a representative office when you intend to conclude contracts locally places you in breach of Romanian law, since representative offices are prohibited from conducting direct commercial activity.

- Selecting a partnership form where partners bear unlimited personal liability, when the business carries financial or legal risk, exposes individual assets with no statutory cap.

- Forming an SA when your firm is a single-owner consultancy subjects you to mandatory audit thresholds and a minimum share capital of 90,000 RON, adding costs disproportionate to the business scale.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors each point toward different structures under Law No. 31/1990 on Companies.

- Ownership Structure: A sole founder with no plans for external investors fits an SRL; multi-party arrangements requiring share transferability suit an SA.

- Tax Objectives: Your eligibility for the micro-enterprise income tax regime (currently 1% or 3%) depends on the entity type and revenue thresholds set by the Fiscal Code.

- Liability Exposure: The degree of personal liability you can accept directly narrows or expands which structures are viable.

- Substance Capacity: If you cannot maintain a genuine operational presence — staff, office, decision-making — certain structures carry higher regulatory scrutiny from ANAF.

- Exit Strategy: Not all Romanian entities permit redomiciliation or conversion; verifying these options before formation avoids structural lock-in.

Compliance Services for Companies in Romania

Ongoing compliance support for Romanian entities, including annual filings, statutory reporting, and regulatory obligations.

Conclusion

Romania's company law, governed primarily by Law No. 31/1990, provides a defined set of structures suited to different operational scales and ownership profiles. For those incorporating a business in Romania, the SRL remains the most registered entity type, favoured for its low capital threshold and single-member eligibility. The SA suits larger ventures requiring share capital structures or public listings. Young entrepreneurs within the EU may find the SRL-D a practical entry point, given its specific fiscal concessions. Partnerships carry unlimited liability and tend to serve closely held, professional arrangements. Branch offices and representative offices serve foreign firms testing the market before committing to a local subsidiary.

Ongoing reforms by the National Trade Register Office have progressively digitised registration procedures, and Romania's expanding tax treaty network continues to broaden its appeal for cross-border structures. Professional guidance remains relevant when aligning the chosen entity with your specific ownership, tax, and operational requirements.

How Expanship Can Assist You

Expanship's Romania company formation services cover the full registration process, from choosing between an SRL, SA, or SRL-D to filing with the Oficiul Național al Registrului Comerțului (ONRC). Every structure discussed in this guide carries distinct incorporation steps and ongoing compliance obligations — Expanship prepares your documentation and manages each stage accordingly.

Our corporate services Romania incorporation support includes:

- Preparation and legalization of constitutional documents

- Registered address and local agent provision

- Filing with the ONRC and coordination with relevant authorities

- Post-incorporation compliance management, including annual reporting obligations

- Business banking introduction assistance

Reach out to Expanship Romania to discuss the right structure for your business.

Romania Company Formation

Register your Romanian entity with full ONRC filing support and post-incorporation compliance management.

Frequently Asked Questions (FAQ)

The Societate cu Răspundere Limitată (SRL) is the most frequently incorporated structure, governed by Law No. 31/1990 on companies. Its low minimum share capital requirement and capped personal liability make it practical for small and medium-sized businesses.

A branch has no separate legal personality and leaves the parent company exposed to liabilities arising from Romanian operations, whereas an SRL is a distinct legal entity. Tax treatment also differs: an SRL is subject to corporate income tax domestically, while a branch is taxed on profits attributable to its Romanian activities under the permanent establishment rules of the Fiscal Code.

Among registered structures, the SRL with a sole associate offers relative discretion, though beneficial ownership information must be submitted to the Trade Register under Anti-Money Laundering directives transposed into Romanian law. Nominee arrangements are legally permissible but subject to disclosure obligations under the same framework.

No. Partnerships, including the Societate în Nume Colectiv and Societate în Comandită Simplă, require a minimum of two associates by definition under Law No. 31/1990. An SRL, SRL-D, and sole proprietorship structures such as the PFA can each be established by one individual.

Foreign individuals and legal entities may establish an SRL, SA, branch, or representative office without restrictions on nationality. The Trade Register handles registration regardless of the applicant's country of residence, and no local partner is required for most commercial structures.

Romanian law allows transformation of one company type into another, most commonly from an SRL to an SA as the business scales. The process requires a general assembly decision, updated articles of association, and re-registration with the Oficiul Național al Registrului Comerțului (ONRC).

Not all. The Societate în Nume Colectiv, SRL, SA, and IF each carry distinct legal personality. A representative office and a sole proprietorship (PFA) do not, meaning liabilities flow directly to the founding individual or parent entity rather than sitting within a separate legal structure.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.