Key Takeaways

- Business entities in Réunion are governed by the French Code de commerce and registered through the Greffe du Tribunal de Commerce, which maintains the Registre du Commerce et des Sociétés (RCS).

- As a French overseas department and EU territory, Réunion applies standard French metropolitan corporate tax rules rather than any preferential or zero-tax regime.

- The SAS and SARL are the most commonly registered structures on the island, with the SAS favoured for investor-backed ventures requiring contractual flexibility and the SARL serving as the default for small and medium-sized firms.

- Foreign operators entering Réunion through a branch structure avoid local share capital requirements but expose the parent entity to full liability for the branch's operations.

Introduction to Entity Types in Réunion

Réunion is a French overseas department (département d'outre-mer) located in the Indian Ocean, approximately 700 kilometres east of Madagascar and 170 kilometres southwest of Mauritius. As an integral part of the French Republic, it operates under French law and falls within the European Union's legal and regulatory framework — a distinction that directly shapes the business entity types in Réunion available to founders and investors.

Company registration is administered through the Greffe du Tribunal de Commerce (Commercial Court Registry), which maintains the Registre du Commerce et des Sociétés (RCS). Businesses operating on the island are subject to French metropolitan corporate tax rules, making this a standard-rate, continental tax jurisdiction rather than a preferential or zero-tax regime.

Legal forms of business in Réunion mirror those codified under the French Code de commerce, and include the SA, SAS, SARL, SNC, SCS, SCA, Branch Office, Representative Office, Entreprise Individuelle, and the Auto-Entrepreneur (Micro-Entrepreneur) status. Each structure carries distinct implications for liability, governance, capital requirements, and taxation. The sections that follow examine each of these company structures in detail.

An Overview of Business Structures in Réunion

Réunion recognises several distinct corporate forms under French commercial law, which applies in full as the island is an overseas department (département d'outre-mer) of France. The primary legislation governing these structures is the French Code de commerce, supplemented by the Code civil for certain partnership arrangements. Each form carries a different liability profile, governance requirement, and tax treatment.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| SA | Corporation | Limited to share capital | Subject to IS (corporate tax) | Permitted | 2 shareholders | Greffe du Tribunal de Commerce | Code de commerce |

| SAS | Simplified corporation | Limited to share capital | Subject to IS | Permitted | 1 shareholder | Greffe du Tribunal de Commerce | Code de commerce |

| SARL | Private limited company | Limited to contributions | Subject to IS or IR | Permitted | 1–100 associates | Greffe du Tribunal de Commerce | Code de commerce |

| SNC | General partnership | Unlimited, joint and several | Subject to IR (partners) | Permitted | 2 associates | Greffe du Tribunal de Commerce | Code de commerce |

| SCS | Limited partnership | Mixed (general/limited) | Subject to IR | Permitted | 2 associates | Greffe du Tribunal de Commerce | Code de commerce |

| SCA | Partnership limited by shares | Mixed (general/limited) | Subject to IS | Permitted | 4 members | Greffe du Tribunal de Commerce | Code de commerce |

| Branch Office | Non-independent unit | Parent company liable | Subject to IS on local profits | Permitted | N/A (parent required) | Greffe du Tribunal de Commerce | Code de commerce |

| Representative Office | Non-trading entity | Parent company liable | Generally non-taxable | Not permitted | N/A (parent required) | Greffe du Tribunal de Commerce | Code de commerce |

| Entreprise Individuelle | Sole proprietorship | Unlimited (default) | Subject to IR | Permitted | 1 individual | CFE / URSSAF | Code de commerce |

| Auto-Entrepreneur | Micro-enterprise regime | Unlimited (default) | Flat-rate IR / micro-BIC | Permitted (capped turnover) | 1 individual | CFE / URSSAF | Code de commerce |

Each of these structures is examined in full in the sections below.

Société Anonyme (SA)

Governed by the French Commercial Code (Code de commerce), the Société Anonyme is the standard public limited company structure available in Réunion under the same legal framework that applies across all French overseas departments. As a French département d'outre-mer, Réunion applies metropolitan French corporate law in full, meaning Société Anonyme SA Réunion formation follows identical procedures and statutory requirements as in mainland France.

The SA carries separate legal personality, meaning the entity itself — not its shareholders — holds assets, enters contracts, and bears liabilities. Shareholder exposure is capped at the value of their subscribed shares.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (SA) | Separate legal personality; limited liability |

| Members | Shareholders (min. 2; min. 7 if publicly listed) | No upper limit on shareholder count |

| Governance | Board of Directors (Conseil d'Administration, min. 3, max. 18) or Supervisory Board + Management Board | Two governance models available under French law |

| Local Presence | Registered office in Réunion required | No mandatory local director under French law |

| Share Capital | Minimum €37,000 (non-listed); minimum €225,000 (listed) | At least 50% must be paid up on incorporation |

| Privacy | Shareholder and director details filed with the Greffe du Tribunal de Commerce | Publicly accessible via the Registre du Commerce et des Sociétés (RCS) |

Focus Points

- Taxation: Subject to French corporate income tax (impôt sur les sociétés) at the standard 25% rate, VAT obligations under French rules, and withholding taxes on dividends, interest, and royalties as prescribed by the French tax authority (*Direction Générale des Finances Publiques*); overseas tax credits may apply given Réunion's DOM status.

- Annual Compliance: Statutory accounts must be filed annually with the Greffe; a statutory auditor (commissaire aux comptes) is mandatory for all SAs regardless of size.

- Treaty Access: Full access to France's extensive network of double tax treaties, as Réunion is treated as French territory for treaty purposes.

- Conversion: An SA can be converted into an SAS or SARL by shareholder resolution, subject to compliance with applicable thresholds under the Code de commerce.

- Restrictions: A public offering of shares requires registration with the Autorité des marchés financiers (AMF); this adds significant regulatory burden for smaller firms.

Sub-Types

SA with Board of Directors (Conseil d'Administration)

This is the more traditional governance structure, where a single board oversees both management and supervision. It is commonly used by established businesses that prefer a unified command structure.

SA with Supervisory Board (Conseil de Surveillance) and Management Board (Directoire)

This two-tier model separates executive management from supervisory oversight, reflecting German-influenced governance principles adopted into French law. Larger enterprises or those with institutional investors typically adopt this structure.

Suitable Uses and Limitations

The SA suits large commercial operations, companies seeking external investment, or businesses preparing for a public listing, with France's treaty network being a tangible structural benefit. The mandatory statutory auditor and higher minimum capital make it a disproportionate structure for smaller or early-stage operations.

Best suited for established businesses with multiple institutional shareholders, companies anticipating a public offering, or large trading and holding entities requiring a formal governance structure.

Company Incorporation in Réunion

Incorporate your SA or other entity type in Réunion with end-to-end support from registration to compliance.

Société par Actions Simplifiée (SAS)

The Société par Actions Simplifiée SAS Réunion is governed by the same French commercial law framework applicable across all French overseas departments, principally the Code de commerce as reformed by the law of 3 January 1994, which introduced the SAS form. As an overseas department (département d'outre-mer), Réunion applies metropolitan French company law directly. The entity holds separate legal personality from its shareholders and offers limited liability, while its statutes (statuts) can be drafted with considerable contractual freedom compared to more rigid corporate forms.

This flexibility makes the SAS a frequently chosen structure for SAS incorporation Réunion island, particularly where investors require tailored governance arrangements that a standard SA cannot accommodate within its statutory framework.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Simplified Joint Stock Company | Governed by French Code de commerce |

| Members | Shareholders (actionnaires); President (Président) as sole mandatory officer | President may be an individual or legal entity |

| Membership | Minimum 1 shareholder; no maximum | Single-shareholder variant is the SASU |

| Capital | No statutory minimum; denominated in EUR | Capital is freely set in the statutes |

| Local Presence | Registered office (siège social) in Réunion required | No mandatory local director requirement under current law |

| Privacy | Shareholder identity filed with the Registre du Commerce et des Sociétés (RCS); beneficial ownership reported to Registre des bénéficiaires effectifs | Limited public disclosure compared to SA |

Focus Points

- Taxation: Subject to impôt sur les sociétés (IS) at standard French corporate rates; VAT applies under French rules; dividends paid to non-resident shareholders may attract withholding tax subject to applicable tax treaties; no separate territorial surcharge specific to Réunion.

- Annual Compliance: Annual accounts must be filed with the RCS; statutory audit (commissaire aux comptes) is mandatory once two of three legal thresholds (balance sheet, turnover, headcount) are exceeded.

- Treaty Access: As a French territory, entities benefit from France's extensive double tax treaty network.

- Conversion: An SAS may be converted into an SA or SARL by shareholder resolution, subject to meeting the target form's requirements.

- Restrictions: Shares in an SAS cannot be offered to the public (appel public à l'épargne is prohibited).

Sub-Types

Société par Actions Simplifiée Unipersonnelle (SASU)

The SASU is a single-shareholder variant of the SAS where one individual or legal entity holds 100% of the shares. Governance requirements remain identical to the standard SAS, but all shareholder decisions are taken unilaterally by the sole shareholder, simplifying internal procedures.

The simplified joint stock company Réunion is commonly used for holding structures, intra-group IP ownership, and joint ventures requiring bespoke shareholder agreements. Its primary advantage is statutory flexibility in governance; its principal limitation is the prohibition on public share offerings, which restricts capital-raising options.

The SAS is best suited for startups, foreign investors establishing subsidiaries, and multi-party joint ventures that require customised governance beyond what standard corporate forms permit.

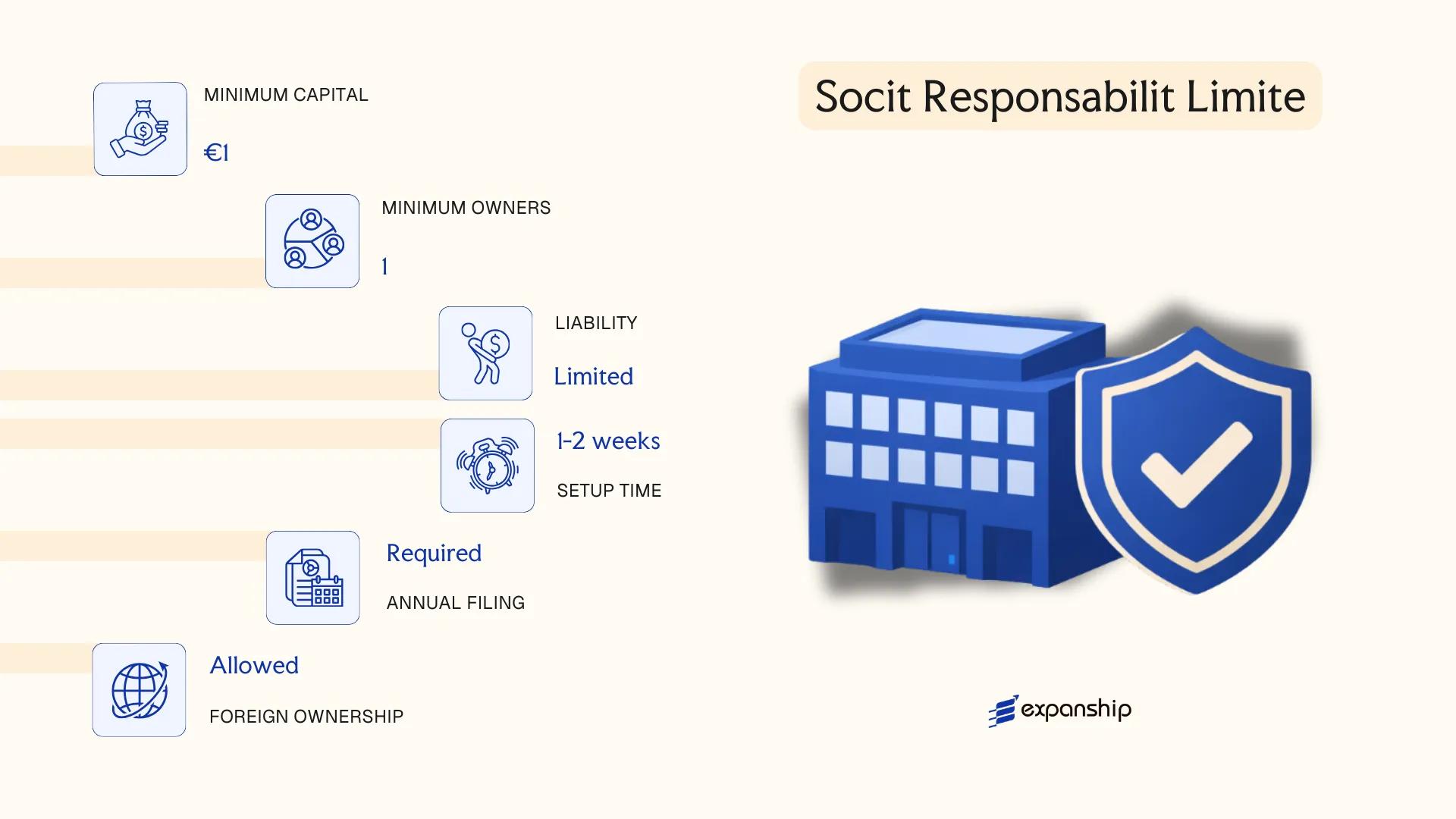

Société à Responsabilité Limitée (SARL)

The Société à Responsabilité Limitée (SARL) in Réunion is governed by French company law, principally the Code de commerce, which applies in full to Réunion as an overseas department (département d'outre-mer) of France. As a distinct legal entity, the SARL carries separate legal personality from its members, meaning the company holds assets, enters contracts, and bears liabilities in its own name.

Liability is capped at each member's capital contribution, making this structure suitable for small to medium enterprises seeking a defined liability boundary without the administrative burden of a public company.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited liability company | Hybrid structure blending partnership flexibility with corporate liability protection |

| Members | 1–100 associés (shareholders) | Single-member variant is the EURL |

| Management | One or more gérants (managers) | Gérant may be a member or a third party; at least one must be a natural person |

| Registered Office | Physical address in Réunion required | Virtual offices are permissible under French law |

| Share Capital | No statutory minimum; €1 symbolic minimum in practice | Capital divided into parts sociales, not freely transferable without member approval |

| Privacy | Gérant identity disclosed in public register (RCS) | Beneficial ownership reported to the Registre des bénéficiaires effectifs |

Focus Points

- Taxation: Subject to standard French corporate income tax (IS) at 25%; VAT applies at standard French rates; dividends paid to non-residents may attract withholding tax under French domestic rules, reducible via France's tax treaty network.

- Annual Compliance: Annual accounts must be filed with the greffe du tribunal de commerce; statutory audit is required only above certain thresholds.

- Treaty Access: As a French entity, the SARL accesses France's extensive double tax treaty network, covering over 120 jurisdictions.

- Transfer of Shares: Parts sociales require approval (agrément) from existing members, restricting free transferability.

- Conversion: A SARL can be converted into an SAS or SA by member resolution without dissolving the entity.

Sub-Types

Entreprise Unipersonnelle à Responsabilité Limitée (EURL)

The EURL is a single-member SARL, permitting sole ownership while retaining the SARL's liability framework. It is commonly used by individual entrepreneurs who require a separate legal structure without admitting additional shareholders.

Closing

The SARL suits trading companies, family-owned businesses, and joint ventures where members want controlled ownership transfer and defined liability. Its principal advantage is access to France's treaty network; the key limitation is the restricted transferability of shares, which can complicate investor entry or exit.

The SARL is best suited for small to medium-sized businesses with a stable, known shareholder base seeking liability protection under a well-regulated French legal framework.

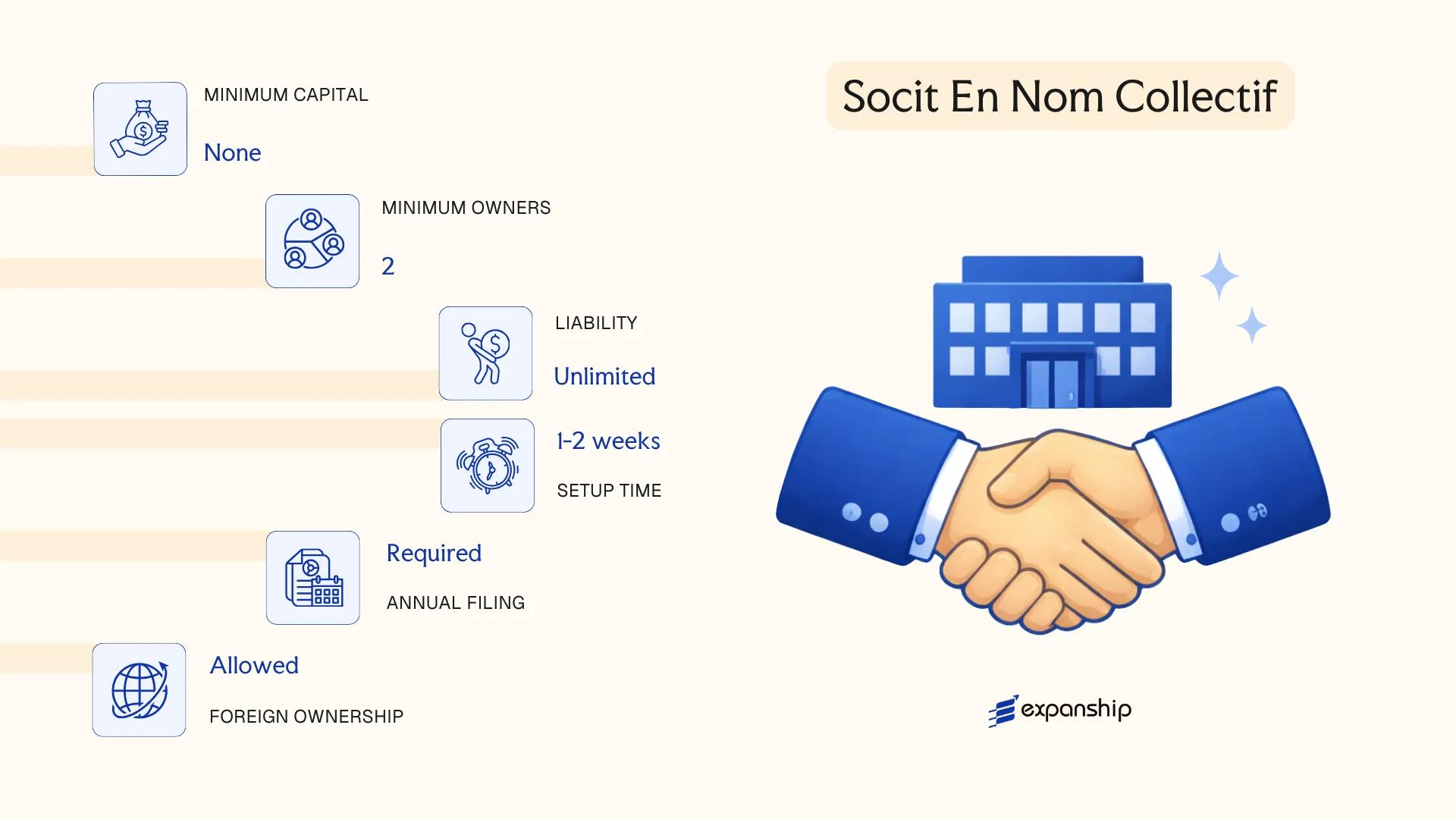

Société en Nom Collectif (SNC)

The Société en Nom Collectif SNC Réunion is governed by the French Commercial Code (Code de commerce), which applies in full to Réunion as an overseas department (département d'outre-mer) of France. The SNC is a general partnership structure in which all partners hold the status of associés en nom and bear unlimited, joint, and several liability for the debts of the firm.

Unlike capital companies such as the SA or SAS, the SNC does possess separate legal personality upon registration with the Greffe du Tribunal de Commerce. That legal separation, however, offers no liability shield to its members.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | General partnership (société de personnes) | Governed by Articles L221-1 to L221-17 of the Code de commerce |

| Members | Minimum 2 partners (associés); no statutory maximum | All partners must have trader status (qualité de commerçant) |

| Liability | Unlimited, joint, and several for all partners | Personal assets of each partner are exposed to business debts |

| Registered Office | Must be maintained in France (including Réunion) | Required for registration with the Greffe du Tribunal de Commerce |

| Share Capital | No statutory minimum | Contributions can be in cash, kind, or industry |

| Privacy | Partner identities disclosed in public registry filings | Beneficial ownership reported to the Registre des bénéficiaires effectifs |

Focus Points

- Taxation: The SNC is fiscally transparent by default — profits are taxed at the partner level under personal income tax (impôt sur le revenu); however, partners may elect for corporate income tax (impôt sur les sociétés) treatment. Standard French VAT rules apply, and no separate withholding tax regime exists at the entity level.

- Annual Compliance: Annual accounts must be filed with the Greffe; the SNC is not required to publish accounts unless it exceeds statutory thresholds under French law.

- Treaty Access: As a French territory, Réunion benefits from France's extensive network of double tax treaties, though transparent entity treatment may affect how treaty relief is accessed at the partner level.

- Restrictions: All partners must hold qualité de commerçant; minors and individuals subject to commercial prohibitions cannot participate.

- Conversion: An SNC can be converted into another corporate form, such as a SARL or SAS, subject to unanimous partner consent and re-registration procedures.

Closing Paragraph

The SNC suits closely-held trading or family businesses where partners prefer flexible profit-sharing and are willing to accept personal liability. The principal advantage is structural flexibility in profit allocation and management; the clear drawback is that every partner's personal estate remains fully exposed to the firm's obligations.

The SNC is best suited for small groups of trusted partners — particularly family businesses or professional firms — who require flexible internal arrangements and can accept unlimited personal liability.

Partnerships and Hybrid Structures [Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA)]

Both the Société en Commandite Simple (SCS) and the Société en Commandite par Actions (SCA) are governed by the French Code de Commerce, which applies directly in Réunion as an overseas department of France. The SCS and SCA partnership structures in Réunion share a defining characteristic: a two-tier membership structure separating general partners, who bear unlimited liability, from limited partners, whose exposure is capped at their capital contribution.

The SCA is the hybrid variant, combining features of a limited partnership with those of a joint-stock company. This structure allows the SCA to issue shares to limited partners, making it more suited to capital-intensive arrangements than the SCS, which does not issue transferable shares.

Key Characteristics

| Requirement | SCS | SCA |

|---|---|---|

| Legal Form | Limited partnership | Hybrid limited partnership with share capital |

| Members | Min. 1 general partner (associé commandité, unlimited liability) + 1 limited partner (associé commanditaire) | Min. 1 general partner + 3 limited shareholders (actionnaires commanditaires) |

| Registered Office | Must be maintained in France/Réunion | Must be maintained in France/Réunion |

| Share Capital | No statutory minimum | No statutory minimum |

| Transferability | Limited partner interests not freely transferable without general partner consent | Limited partner shares freely transferable; general partner interests require consent |

| Privacy | No public disclosure of partner identities beyond statutory filings with the Greffe du Tribunal de Commerce | Same as SCS; beneficial ownership registered with RBE |

Focus Points

- Taxation: Both structures are subject to French corporate tax (IS) at the standard 25% rate if they opt for or are required to apply IS; otherwise, partnership income may be taxed at the partner level under IR. VAT, payroll taxes, and withholding taxes on distributions follow standard French rules applicable in Réunion.

- Annual compliance: Both entities must file annual accounts with the Greffe du Tribunal de Commerce and maintain statutory registers.

- Economic substance: No specific substance regime beyond standard French commercial law requirements for registered office and management.

- Conversion: An SCS may convert to an SCA or other French commercial forms subject to unanimous or qualified partner consent per the Code de Commerce.

- Restrictions: General partners in both structures cannot limit their personal liability; this remains a structural constraint regardless of contractual arrangements.

Sub-Types

Société en Commandite Simple (SCS)

The SCS is the simpler of the two forms, with no share capital requirement and no public market for partner interests. It is typically used for family-held businesses or investment vehicles where the controlling general partner wishes to retain full operational authority.

Société en Commandite par Actions (SCA)

The SCA introduces a supervisory board (conseil de surveillance) to oversee the general partners, a structural feature absent in the SCS. This governance layer makes the SCA more suitable for larger enterprises or structures requiring institutional investor participation.

Closing

Both forms are used primarily as holding or investment structures where a clear separation of management control from economic participation is required. The two-tier liability structure provides general partners with strong governance control, though that same feature — unlimited personal liability for general partners — can deter individuals from accepting the commandité role.

These structures suit experienced investors or family groups seeking a controlled holding arrangement where one party retains management authority and others participate as passive capital contributors.

Foreign Business Structures [Branch Office, Representative Office]

Because Réunion is an integral part of France and an EU outermost region, foreign companies establishing a presence there operate under French commercial law, primarily the Code de Commerce. Neither a branch nor a representative office constitutes a separate legal entity; both remain extensions of the parent company, which retains full legal and financial responsibility for their activities.

Completing a foreign branch office setup in Réunion requires registration with the Greffe du Tribunal de Commerce, after which the branch receives a SIRET number and is listed in the Registre du Commerce et des Sociétés (RCS). A representative office, by contrast, is confined to non-commercial activities such as market research or liaison functions and cannot generate local revenue.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Liability | Parent bears full liability | Parent bears full liability |

| Commercial Activity | Permitted | Not permitted |

| Registration | RCS via Greffe du Tribunal de Commerce; SIRET required | No formal commercial registration; may require local administrative notifications |

| Local Representative | Mandatory appointed representative (permanent representative) | Appointed contact person recommended |

| Registered Address | Physical address in Réunion required | Physical address required |

Focus Points

- Taxation: Branch profits are subject to French corporate income tax (IS) at the standard 25% rate; VAT applies to taxable supplies; withholding tax may apply to profit remittances depending on the parent's home jurisdiction and applicable tax treaties.

- Treaty Access: As part of France, Réunion benefits from France's extensive double tax treaty network, which may reduce withholding obligations for the parent company.

- Annual Compliance: Branches must file annual accounts derived from the parent's financial statements with the Greffe and submit French tax returns; representative offices have lighter obligations but must still respect local employment and administrative rules.

- Restrictions: A representative office cannot invoice clients or sign commercial contracts; any revenue-generating activity automatically triggers branch or subsidiary obligations.

- Conversion: A branch can be converted into a subsidiary (such as a SARL or SAS) without dissolving the parent's French registration, though the process requires a new RCS filing and capital contribution.

Sub-Types

Branch Office (Succursale)

A succursale is a registered, operationally active extension of the foreign parent, capable of hiring staff, entering contracts, and generating taxable revenue in France. It is the standard vehicle for foreign companies wishing to trade directly without incorporating a standalone French entity.

Representative Office (Bureau de Liaison)

A bureau de liaison performs preparatory or auxiliary functions only, such as promotional activities or gathering market intelligence. Because it produces no taxable income, it carries a lower compliance burden, though its operational scope is strictly limited.

Both structures suit foreign companies testing the French market before committing to full incorporation. The branch offers commercial reach without establishing a new legal entity; its principal drawback is that the parent remains fully exposed to any liabilities incurred locally.

Foreign companies seeking a direct but structurally light presence in the French regulatory environment before committing to a standalone subsidiary.

Sole Proprietorship and Micro-Enterprise [Entreprise Individuelle, Auto-Entrepreneur / Micro-Entrepreneur]

Both the Entreprise Individuelle and the auto-entrepreneur micro-enterprise status in Réunion operate under French metropolitan law, as the island is an overseas department (département d'outre-mer) fully subject to French legislation. The primary governing framework is the loi du 14 février 2022 (known as the loi en faveur de l'activité professionnelle indépendante), which introduced a statutory patrimonial separation between personal and professional assets for sole traders — without creating a distinct legal entity.

The auto-entrepreneur regime, formally the micro-entrepreneur status, is a simplified administrative layer applied on top of the Entreprise Individuelle structure. Registration is handled through the Guichet unique of the Institut National de la Propriété Industrielle (INPI), which replaced the former Centre de Formalités des Entreprises (CFE) network in 2023.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Entreprise Individuelle (sole trader) | No separate legal personality; owner and business are one legal person |

| Proprietor | Single natural person only | Cannot be held by a legal entity |

| Liability | Statutory asset separation since 2022 | Professional assets protected from personal creditors by default; personal assets protected from business creditors |

| Local Presence | Registered business address in Réunion required | Must correspond to actual place of activity or domicile |

| Share Capital | None required | No minimum capital obligation |

| Revenue Thresholds (Micro) | Commercial: €188,700 / Services: €77,700 (2024 thresholds) | Exceeding thresholds triggers exit from micro regime; subject to periodic revision |

Focus Points

- Taxation: Micro-entrepreneurs pay income tax under the régime micro-fiscal (flat-rate abatements on gross revenue) or opt for the versement libératoire; standard income tax (IR) applies to the Entreprise Individuelle; VAT exemption applies below the franchise en base thresholds, with no corporate tax.

- Social Contributions: Cotisations sociales are calculated as a fixed percentage of actual turnover under the micro regime, administered through URSSAF.

- Annual Compliance: No statutory accounts filing or audit obligation; micro-entrepreneurs must maintain a revenue register (livre des recettes) and, for commercial activity, a purchase log.

- Conversion: An Entreprise Individuelle can be converted into a one-person EURL or SASU by transferring the business assets; the micro-entrepreneur regime cannot be directly "converted" but ceases upon threshold breach or voluntary deregistration.

- Restrictions: The micro-entrepreneur regime excludes certain regulated professions and activities subject to TVA immobilière; agricultural activities fall under a separate chambre d'agriculture registration.

Sub-Types

Auto-Entrepreneur / Micro-Entrepreneur

This is not a separate legal form but a simplified fiscal and social regime available to eligible Entreprise Individuelle operators. It offers a reduced administrative burden with forfait social and fiscal calculations based solely on turnover, making it the standard entry point for freelancers and small traders.

Entreprise Individuelle à Responsabilité (Standard EI post-2022)

Following the 2022 reform, all newly registered sole traders automatically benefit from the statutory separation of patrimonies without needing to adopt a separate legal structure. This form suits operators with higher revenue or asset exposure who have outgrown the micro-revenue caps.

Both forms suit low-capital, single-operator activities — commercial trading, freelance services, and artisan trades. The primary advantage is minimal setup cost with no capital requirement; the central limitation is that neither form permits multiple owners or the issuance of shares, restricting external investment entirely.

Best suited for individual entrepreneurs, freelancers, and artisans in Réunion testing a business concept or operating a low-risk, single-person activity below the micro-revenue thresholds.

How to Choose the Right Entity Type in Réunion

Selecting how to choose company structure in Réunion requires more than comparing registration fees — the consequences of a mismatched structure affect tax position, liability exposure, and operational legality.

Why Your Entity Choice Matters

Concrete outcomes follow from the wrong selection:

- Operating through a structure not authorised for local commercial activity can result in administrative dissolution or financial penalties under French commercial law as applied in Réunion.

- Choosing an entity that falls outside the French tax treaty network means your business cannot claim reduced withholding tax rates in counterpart jurisdictions.

- Forming a capital company when a single-person consultancy is all that is required generates mandatory audit thresholds and annual statutory costs that serve no operational purpose.

- Selecting a structure incompatible with your intended governance model locks shareholders into obligations — such as annual general meetings and statutory accounts — that may be disproportionate to the business activity.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors each correspond to distinct structures under the French Code de commerce, which applies in Réunion as a French overseas department.

- Ownership and Management: Single-owner operations and multi-party ventures have different governance requirements, pushing toward an Entreprise Individuelle or a multi-associate SARL respectively.

- Tax Objectives: Your eligibility for specific French tax regimes, including the micro-entreprise flat-rate system, depends directly on the entity form selected.

- Substance Capacity: If maintaining a physical presence is not feasible, your structure must reflect that limitation to avoid compliance failures.

- Exit Strategy: Not all French entities permit straightforward conversion or redomiciliation, so anticipated structural changes should factor into the initial choice.

- Privacy Requirements: Director and shareholder details are filed with the Registre du Commerce et des Sociétés and are publicly accessible; structures offering any degree of confidentiality are limited.

The full text of the Code de commerce is available on Légifrance, the official French legal database.

Compliance Services for Companies in Réunion

Maintain statutory obligations and avoid penalties with structured compliance support tailored to French overseas department requirements.

Conclusion

Incorporating a business in Réunion means operating within French commercial law as applied in an overseas department, where the same Code de commerce provisions that govern metropolitan France set the rules for entity formation, liability, and governance. Each structure serves a distinct profile: the SA suits large enterprises requiring listed capital or formal board governance; the SAS offers the most contractual flexibility for investor-backed ventures; the SARL remains the default choice for small and medium-sized firms; and the SNC places full personal liability on its associates, making it uncommon outside professional circles.

Among these, the SAS and SARL account for the majority of registrations with the Greffe du Tribunal de Commerce. Doing business in Réunion island also draws foreign operators toward branch structures, which avoid local share capital requirements but carry full parent liability.

As a French overseas department, Réunion's regulatory framework tracks closely with EU developments, meaning any shift in French or European corporate legislation applies directly. Expanship assists clients at each stage of this process.

How Expanship Can Assist You

Expanship's company formation services in Réunion cover the full registration process, from selecting the right legal structure — SA, SAS, SARL, or SNC — through to filing with the Centre de Formalités des Entreprises (CFE) and the Greffe du Tribunal de Commerce. Each entity type carries distinct obligations, and our team ensures your documentation meets the requirements set by local authorities before submission.

Across our corporate services in Réunion, we support clients at every stage of the setup process:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- Filing and liaison with the Greffe du Tribunal de Commerce

- Post-incorporation compliance management, including annual reporting

- Banking introduction assistance for newly registered entities

- Ongoing statutory maintenance and corporate secretarial support

Reach out to our team directly through Expanship Réunion to discuss your entity setup requirements.

Frequently Asked Questions (FAQ)

The SARL (Société à Responsabilité Limitée) is the most frequently formed structure. Its capped liability, flexible governance under the French Code de commerce, and suitability for small to mid-sized operations make it the default choice for resident and non-resident founders alike.

Both structures offer limited liability, but the SAS allows greater freedom in drafting shareholder agreements and does not cap the number of shareholders. The SARL imposes a ceiling of 100 associates and applies more rigid statutory rules around profit distribution and management.

The SAS provides relatively stronger privacy, as shareholder information is not required on publicly accessible documents in the same way as some other forms. Nominee arrangements are legally permitted under French law, though beneficial ownership must still be declared to the Registre des bénéficiaires effectifs.

No. The SA requires a minimum of two shareholders, and the SNC and partnership structures (SCS, SCA) each require at least two partners by definition. The SARL, SAS, and sole proprietorship forms can each be established by one person.

Foreign nationals can form an SA, SAS, or SARL without restrictions on nationality, as French law does not impose residency requirements on shareholders. Directors of certain forms may need a valid right to work or reside if they intend to manage the business actively from within the territory.

French commercial law permits the transformation of one legal form into another, for example converting a SARL into an SAS, provided the required formalities under the Code de commerce are completed. The process involves a shareholder resolution, updated articles of association, and re-registration with the Registre du Commerce et des Sociétés (RCS).

The SA, SAS, SARL, SNC, SCS, and SCA all possess distinct legal personality upon registration with the RCS. The Entreprise Individuelle and micro-enterprise (auto-entrepreneur) regime do not create a separate legal entity; the individual and the business remain legally unified, which carries direct implications for personal liability.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.